Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 8,028 million (4.77 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover, and the EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar the Euro and the Sterling Pound to exchange at Ksh 117.66, Ksh 123.92 and 143.92 respectively. The observed overall depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 3.99% | 0.28% |

| Euro | -3.26% | 1.22% |

| Sterling Pound | -5.53% | 1.22% |

Liquidity

Liquidity in the money markets tightened, partly reflecting government payments which offset tax remittances. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 5.12% | 5.24% |

| Interbank volume (billion) | 10.55 | 17.10 |

| Commercial banks’ excess reserves (billion) | 45.20 | 36.80 |

Fixed Income

T-Bills

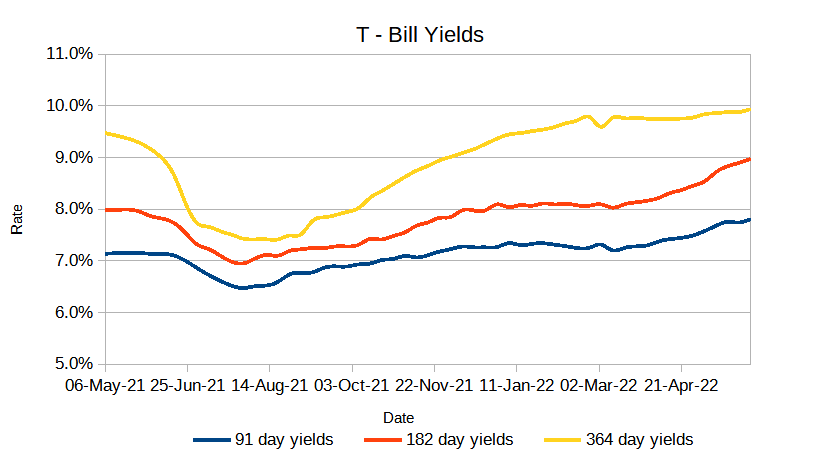

T-Bills remained under-subscribed during the week with an increase in the overall subscription rate from 80.80% recorded in the previous week to 88.30%. The 91-day T-Bill got the highest subscription rate at 201.4% while the 364-day T-Bill and 182-day T-Bill had a subscription rate of 82.9% and 48.5% respectively. The under-subscription is attributed to reduced investor sentiments in the face of high currency and inflation risks. The acceptance rate decreased by 1.69% to close the week at 95.69%.

T-Bonds

The bonds market had a lower demand for the week’s bond offers. Bonds turnover decreased by 27.08% from 17.78B in the previous week to 12.97B. Total bond deals decreased by 16.30%.

In the primary market, the Central Bank released results for the tap sale of the two fixed coupon treasury bonds; FXD1/2022/03 and FXD1/2022/15. The 3-year and 15 year bond received bids worth Ksh. 3.62B and Ksh. 15.96B respectively translating to an undersubscription rate of 78.4% against the targeted Ksh. 25B.

Eurobonds

In the international market, the yields on the 10-year Eurobonds for Angola and Ghana rose. Yields on Kenya’s Eurobonds generally increased by 11.67 basis points compared to the previous week, 3.13% and 7.40% month to date and year to date respectively. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 10.73% | 4.30% | -0.02% |

| 2018 10-Year Issue | 7.82% | 3.35% | 0.28% |

| 2018 30-Year Issue | 4.70% | 1.91% | 0.03% |

| 2019 7-Year Issue | 9.38% | 4.37% | 0.04% |

| 2019 12-Year Issue | 6.33% | 2.61% | 0.18% |

| 2021 12-Year Issue | 5.45% | 2.22% | 0.19% |

Equities

NASI, NSE 20 and NSE 25 decreased by 3.78%, 3.29% and 3.79% compared to last week bringing the year to date performance to -29.86%, -17.81% and -26.32% respectively. The market capitalization decreased by 3.79% from the week to close at 1.826 trillion recording a year to date decline of 29.85%. The performance was driven by loses recorded by large-cap stocks. Top loses were recorded in EABL, ABSA, Safaricom and KCB which declined by 7.43%, 5.56%, 4.94% and 3.17% respectively.

The Banking sector had shares worth Kshs 495M transacted which accounted for 18.69% of the week’s traded value, Manufacturing & Allied sector had shares worth 156M transacted which represented 5.88% and Safaricom, with shares worth Kshs 1.96B transacted represented 74.05% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Sameer Africa | 40.00% | 21.65% |

| EA Portland Cement | 34.15% | 13.54% |

| Flame Tree Group | 6.40% | 9.92% |

| Britam | -19.05% | 9.68% |

| Fahari I-REIT | -5.92% | 9.03% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| Nation Media | -15.19% | -16.25% |

| Scangroup | -26.34% | -11.95% |

| Limuru Tea | 00.00% | -9.86% |

| Olympia Capital | 16.32% | -9.05% |

| Stanbic | 5.17% | -8.73% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 5.75 | 1.67 | -70.96% |

| Derivatives Contracts | 72 | 38 | -47.22% |

| I-REIT Turnover | 0.75 | 0.37 | -50.77% |

| I-REIT Deals | 38 | 18 | -52.63% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -18.45% | 6.45% |

| Dow Jones Industrial Average (DJI) | -13.90% | 5.39% |

| FTSE 100 (FTSE) | -3.95% | 2.74% |

| STOXX Europe 600 | -15.73% | 24.0% |

| Shanghai Composite (SSEC) | -7.78% | 0.99% |

| MSCI Emerging Markets | -18.02% | 0.65% |

| MSCI World Index | -19.19% | 5.38% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -16.38% | -2.74% |

| JSE All Share | -10.49% | 1.54% |

| NSE All Share (NGSE) | 20.17% | -0.14% |

| DSEI (Tanzania) | -5.12% | -2.15% |

| ALSIUG (Uganda) | -18.78 | -4.22% |

U.S stocks closed the week high, as gains in the Basic Materials, Technology and Industrials sectors led shares higher. The stocks rebounded during the week as financial markets have been roiled over worries that rapid rate hikes by the Federal Reserve to rein in 40-year-high inflation could cause a recession. However, investors are gauging the long-term market dynamics after S&P 500 fell by 20% signaling a bear market.

European stocks closed the week higher after receiving a positive handover from the U.S following the completion of the two day testimony by the Federal Reserve on the economy in the congress. However, fears persist that aggressive monetary policy tightening by central banks around the world, aimed at curbing a recent surge in inflation, may instead spark a recession.

Asia Pacific stocks closed the week lower, as investors assessed the monetary policy outlook after U.S. Federal Reserve acknowledged the risk of a recession. Japan and South Korea reported a decrease while Australia, China and Hong Kong were mostly up. However, the Bank of Japan held on to its strategy of pinning 10-year yields near zero at its policy meeting on Friday.

On the global commodities markets, Crude Oil WTI closed the week lower by 3.10% and the ICE Brent Crude decreased by 0.37%. Gold futures prices decreased by 0.75% to settle at $1,828.10.

Week’s Highlights

- The president signed the Supplementary Appropriation Bill of 2022 into a law. The law avails Sh. 88.8B for government expenditure on public services. The fuel stabilization fund got allocated an additional Sh. 49.2B while drought mitigation interventions such as the provision of relief food; the national fertilizer subsidy programme; settlement of ongoing road construction bills were allocated Sh26.7B; social protection and safety net measures was assigned Sh1.5B.

- The Senate approved the proposal to raise the debt ceiling to Ksh. 10 trillion giving Treasury the leeway to borrow Sh. 846B to meet the budget deficit for the 2022/23 financial year.

- According to the Kenya Bankers Association-House Price Index (KBA-HPI), house prices on average went down by 1.82% in the first quarter of 2021, overturning the marginal recovery of 0.22% recorded in the fourth quarter of 2020. This is attributed to a general price correction trend as well as slow economic growth and weakened households’ purchasing power.

- The Kenya Mortgage Refinancing Company (KMRC) is set to issue its KSh10.4 billion medium term notes (MTN) in mid-2023. This delay will help the company align proceeds from the bond’s program to its mortgage pipeline.

- The International Monetary Fund (IMF) Executive Board is set to delay its approval to disburse a KSh28.7 billion loan to Kenya. This implies that there will be a marginal deficit in financing the budget to June 30th.

- According to the Tea Board of Kenya, the Russia – Ukraine war cut the tea exports to Russia down to KSh598 million in March as volumes dropped 74% to 686,072 from 2.6 million kilos during the same period last year, highlighting the negative impact that the conflict has had on Kenya’s global trade.

- The Central Bank of Russia (CBR) cut its key interest rate from 14% to 11%, citing a slowing in inflation and the recovery of the ruble. On the other hand, soaring food prices pushed UK consumer price inflation to a 40-year high of 9.1% last month, the highest rate since 1982 while South African inflation surged above the central bank’s target range for the first time in more than five years to close at 6.5% in May compared to 5.9% recorded in April.

Get future reports

Please provide your details below to get future reports: