Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,860 million (3.84 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar and the Sterling Pound but strengthened against the Euro to exchange at KES 126.43, KES 152.12 and KES 133.97 respectively. The observed depreciation against the Dollar is attributed to increased demand from importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 2.44% | 0.64% |

| Sterling Pound | 2.28% | 0.66% |

| Euro | 1.76% | -0.28% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate rising from 6.23% to 6.56%, as tax remittances more than offset government payments. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.23% | 6.56% |

| Interbank volume (billion) | 22.05 | 24.06 |

| Commercial banks’ excess reserves (billion) | 16.10 | 15.40 |

Fixed Income

T-Bills

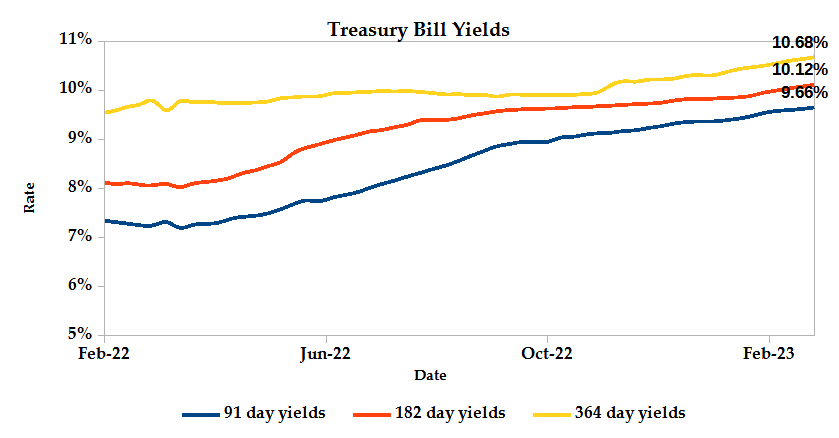

T-Bills were under-subscribed during the week, with the overall subscription rate recorded at 80.98%, down from an oversubscription rate of 191.31% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 284.05% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 44.05% and 36.68% respectively. The acceptance rate decreased by 0.43% to close the week at 96.97%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover declined by 4.92% from KES 12.95 billion in the previous week to KES 12.31 billion. Total bond deals declined by 1.74% from 517 in the previous week to 508.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average 0.16% compared to the previous week, 0.49% month to date and declined 0.05% year to date. The yields on the 10-Year Eurobonds for Ghana and Angola also increased . Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | -1.03% | 0.64% | 0.17% |

| 2018 10-Year Issue | 0.23% | 0.53% | 0.19% |

| 2018 30-Year Issue | 0.10% | 0.36% | 0.16% |

| 2019 7-Year Issue | -0.05% | 0.42% | 0.07% |

| 2019 12-Year Issue | 0.06% | 0.52% | 0.21% |

| 2021 13-Year Issue | 0.39% | 0.46% | 0.17% |

Equities

NASI, NSE 20 and NSE 25 settled 1.21%, 1.51% and 1.25% lower compared to the previous week bringing the year to date performance to -0.68%, -1.21% and 0.38% respectively. Market capitalization lost 1.21% from the previous week to close at KES 1.97 trillion recording a year to date decline of 0.68%. The performance was driven by losses recorded by large-cap stocks such as EABL, Safaricom, Equity, KCB and Co-operative of 2.50%, 1.27%, 1.08%, 0.65% and 0.40% respectively. These were however mitigated by the gain recorded by Standard Chartered of 1.09%.

The Banking sector had shares worth KES 317M transacted which accounted for 39.07% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 33.8M transacted which represented 4.17% and Safaricom, with shares worth KES 354.5M transacted represented 43.66% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| BOC | 8.83% | 10.00% |

| EA Portland | -3.53% | 8.97% |

| Kapchorua Tea | 18.36% | 8.73% |

| Olympia | -4.39% | 8.02% |

| Home Afrika | -5.88% | 6.67% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| NBV | -14.97% | -11.61% |

| Sameer | 1.42% | -10.42% |

| TP Serena | -3.85% | -9.42% |

| Flame Tree | -1.82% | -9.24% |

| Kakuzi | -0.65% | -7.83% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.56 | 0.90 | 60.34% |

| Derivatives Contracts | 12 | 11 | -8.33% |

| I-REIT Turnover (million) | 0.39 | 0.36 | 6.00% |

| I-REIT deals | 56 | 63 | 12.50% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 3.82% | -1.99% |

| Dow Jones Industrial Average (DJI) | -0.96% | -2.38% |

| FTSE 100 (FTSE) | 4.30% | -1.53% |

| STOXX Europe 600 | 5.42% | -1.42% |

| Shanghai Composite (SSEC) | 4.83% | 1.34% |

| MSCI Emerging Markets Index | 0.97% | -3.88% |

| MSCI World Index | 4.08% | -3.00% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 0.00% | -0.70% |

| JSE All Share | 3.69% | -3.20% |

| NSE All Share (NGSE) | 6.50% | 2.13% |

| DSEI(Tanzania) | 2.33% | -0.34% |

| ALSIUG (Uganda) | -0.26% | -0.10% |

US stock indices declined this week, with the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite falling by 0.93%, 0.91%, and 1.6%, respectively. Meanwhile, the core Personal Consumption Expenditure (PCE) deflator, the Federal Reserve’s preferred inflation metric, rose by 4.7% YoY in January, exceeding economic forecasts of 4.3%. The strong consumer data also increased expectations of a potential interest rate hike by the Federal Reserve.

European stock markets drifted lower this week following weak manufacturing activity in Germany and France. The DAX index in Germany, CAC 40 in France, and FTSE 100 in the UK all declined. While France’s services sector saw growth in February, the manufacturing sector contracted. Germany also experienced a similar trend in its manufacturing sector.

Asian stocks closed the week higher, despite fears of a US interest rate hike. Nvidia’s stronger-than-expected revenue forecast boosted regional technology stocks, especially chipmakers. The Taiwan Weighted index was the best performer in Asia, up 1.3% on heavyweight chipmaking stocks gains, and Nvidia shares jumped over 8%. The gains spilled over to many Asian chipmaker suppliers, including Taiwan Semiconductor Manufacturing Co (TW:2330), which surged more than 2%.

On the global commodities markets, Crude Oil WTI closed the week 0.66% higher at $76.47 and ICE Brent Crude closed the week the same at $86.16. Gold futures prices settled 1.77% lower at $1,817.10.

Week’s Highlights

- Starting next month, investing in T-Bills and T-Bonds in Kenya will be automated, as announced by Dr. Patrick Njoroge, Governor of the Central Bank of Kenya. This new development means that individuals can invest in government securities directly from their phones, eliminating the need to physically present the CDS forms at CBK. This move towards automation is expected to increase accessibility, enabling more investors to participate in T-Bills and T-Bonds investment opportunities.

- Kenya’s National Security Council has approved the government’s acquisition of a 60% stake in Telkom Kenya from UK-based private equity fund, Helios Partners, for USD 1 due to national security concerns. The government also reimbursed Helios Partners USD 51 million in shareholder loans and the private equity fund forewent KES 29.8 billion in proceeds from the sale of a 70% stake in Orange in 2016.

- JP Morgan, the world’s sixth-largest bank, has opened a regional office in Nairobi, Kenya, as part of its global expansion strategy. The office will serve as a hub for JP Morgan’s operations in East Africa and will target large multinationals not well-served by local investment banking firms due to a lack of expertise in handling large transactions.

- The Kenya National Treasury plans to review the list of products enjoying tax waivers as taxpayers paid KES 316 billion on behalf of the financial, transport, manufacturing, and communication sectors in 2021. This review may lead to previously tax-exempt products being taxed, affecting a wide range of traders. The Treasury aims to rationalize and harmonize tax expenses to ensure the best value for money, as the 2022 tax expenditure report shows that sectors such as manufacturing, financial services, and information and communication enjoyed the highest tax exemptions in recent years.

- According to the Central Bank of Kenya, non-performing loans in Kenya decreased by KES 18.8 billion in December, bringing the total to KES 487 billion. The decline is attributed to property auctions and debt repayment through restructuring plans. This marks a reversal from the upward trend that started after the August 9th General Election and brings the total below the half-a-trillion-shilling mark. The last time such a significant monthly drop was recorded was in June 2007.

- The Kenya Revenue Authority (KRA) directed The Kenya National Trading Corporation (KNTC) to apply for duty exemption code to import 580,000 metric tonnes of essential goods duty-free including rice, cooking oil, sugar, wheat, and beans to reduce the high cost of living. The Cabinet approved KNTC’s importation of these goods and wheat donated by Ukraine duty-free for one year, after which further importation will be dutiable at the applicable EAC-CET rates unless otherwise approved by the National Treasury.

- Resilient US economy is driving semiconductor stocks’ appeal despite Federal Reserve’s monetary policy concerns. The Philadelphia SE Semiconductor index has gained 16%, outperforming the S&P 500 and Nasdaq Composite. Last year, semiconductor stocks were among the worst hit in the market decline, but in 2023, they have rebounded, supported by a strong economy. Investors are optimistic that economic strength will help semiconductor stocks outperform, given their role as vital components in numerous products.

- China’s economy is expected to rebound in 2023, but the external environment remains challenging, according to the People’s Bank of China’s quarterly policy report. The central bank plans to support domestic demand expansion while avoiding excessive stimulus, and keep prices of energy and food stable. The report also highlights the need for time to transition the property sector and balance local government fiscal revenue and expenditure. No substantial changes have been made to the report, with markets anticipating economic targets and policies for 2023 during the annual parliamentary meeting starting on March 5.

Get future reports

Please provide your details below to get future reports: