Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,297 million (3.50 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar but strengthened against the Sterling Pound and the Euro to exchange at KES 137.49, KES 170.86 and KES 148.51 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | 11.40% | 0.45% |

| Sterling Pound | 14.88% | -0.40% |

| Euro | 12.80% | -0.57% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate increasing from 9.19% to 9.25%, as tax remittances more than offset government payments. Remittance inflows totalled $320.32 million in April 2023, a 10.27% decrease from $356.98 million in March 2023 and a 9.78% decline from $355.04 million in April 2022. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 9.19% | 9.25% |

| Interbank volume (billion) | 30.53 | 29.00 |

| Commercial banks’ excess reserves (billion) | 18.20 | 36.40 |

Fixed Income

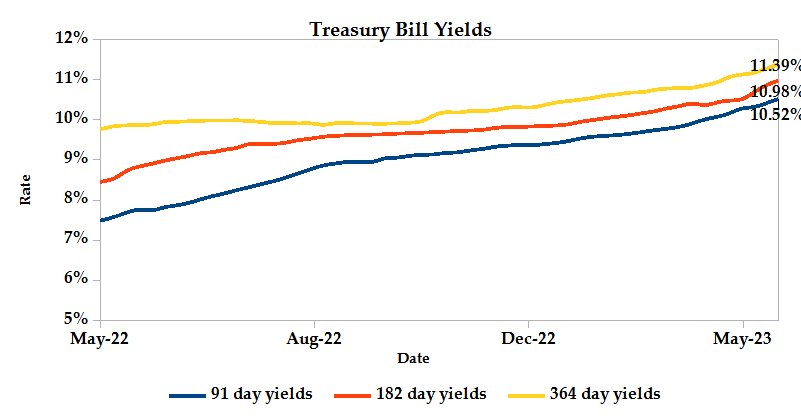

T-Bills

T-Bills were over-subscribed during the week, with the overall subscription rate recorded as 150.09%, down from 188.91% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 602.33% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 42.16% and 77.12% respectively. The acceptance rate decreased by 0.03% to close the week at 99.85%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 31.18% from KES 14.75 billion in the previous week to KES 19.35 billion. Total bond deals increased by 14.43% from 395 in the previous week to 452.

In the primary bond market, CBK reopened the 3-year fixed bond; FXD1/2023/003, through a tap sale which sought to raise KES 10 billion. The issue was over-subscribed receiving bids worth KES 10.60 billion, representing a performance of 106.03%. KES 10.60 billion worth of bids were accepted at a weighted average rate of 14.23%.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average 0.83% compared to the previous week, 1.69% month to date and increased 2.08% year to date. The yields on the 10-Year Eurobonds for Angola declined while that of Ghana increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 2.46% | -5.20% | -2.18% |

| 2018 10-Year Issue | 2.11% | -1.49% | -0.68% |

| 2018 30-Year Issue | 1.09% | -0.74% | -0.37% |

| 2019 7-Year Issue | 3.34% | -1.21% | -0.81% |

| 2019 12-Year Issue | 1.64% | -0.77% | -0.44% |

| 2021 13-Year Issue | 1.82% | -0.74% | -0.47% |

Equities

NASI and NSE 25 settled 5.28% and 2.67% higher while NSE 20 settled 0.30% lower compared to the previous week bringing the year-to-date performance to -22.63%, -12.39% and -18.05% respectively. Market capitalization gained 5.29% from the previous week to close at KES 1.53 trillion recording a year-to-date decline of 22.70%. The performance was driven by gains recorded by large-cap stocks such as Safaricom, KCB and EABL of 13.21%, 8.25% and 4.81% respectively. These were however weighed down by losses recorded by Equity and Stanbic of 5.88% and 1.79% respectively.

The Banking sector had shares worth KES 614M transacted which accounted for 37.44% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 263.3M transacted which represented 16.03% and Safaricom, with shares worth KES 734.9M transacted represented 44.75% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Eveready | 50.00% | 28.57% |

| Longhorn | -13.33% | 14.04% |

| Safaricom | -37.63% | 13.21% |

| Uchumi | -9.52% | 11.76% |

| HF Group | 33.02% | 11.44% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| B.O.C | -1.06% | -22.44% |

| Flame Tree | 11.82% | -10.22% |

| WPP Scangroup | -10.45% | -9.82% |

| Olympia | -8.45% | -9.67% |

| Unga | -40.63% | -9.52% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.04 | 1.70 | 63.02% |

| Derivatives Contracts | 23.00 | 20.00 | -13.04% |

| I-REIT Turnover (million) | 0.29 | 0.41 | 38.37% |

| I-REIT deals | 25 | 50 | 100.00% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 9.62% | 1.65% |

| Dow Jones Industrial Average (DJI) | 0.88% | 0.38% |

| FTSE 100 (FTSE) | 2.68% | 0.03% |

| STOXX Europe 600 | 7.99% | 0.73% |

| Shanghai Composite (SSEC) | 5.36% | 0.34% |

| MSCI Emerging Markets Index | 1.52% | 0.44% |

| MSCI World Index | 9.30% | 1.19% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 0.27% | 0.79% |

| JSE All Share | 6.77% | 0.03% |

| NSE All Share (NGSE) | 1.15% | -0.05% |

| DSEI (Tanzania) | -3.83% | 2.12% |

| ALSIUG (Uganda) | -14.30% | -1.12% |

US indices edged higher as significant benchmark averages capped a solid week. S&P 500, Dow Jones and Nasdaq Composite all had gains for the week. Market analysts are still keeping an eye on the US debt ceiling talks and are optimistic that it will be raised. Positive corporate news from well-known companies also uplifted sentiment, with NVIDIA advancing after joining ServiceNow to develop artificial intelligence for businesses. After experiencing huge fluctuations in previous weeks, regional banks appeared to be stabilizing, with the KBW Regional Bank index rising 8.5%.

European indices in the past week recorded a marginal increase as they hope to benefit from the global optimism that the US debt default will be avoided. According to the most recent Growth from Knowledge(GfK) survey, consumer confidence in the UK has increased for four months running and is now at its best level since February 2022. Additionally, for a large number of prominent European corporations, the first quarter was relatively good. So far, over half of the STOXX 600 businesses have announced first-quarter results, with two-thirds exceeding expectations.

Asia Pacific indices finished the week on a positive note, thanks to gains in energy and finance firms. Tiangi Lithium, Ganfeng Lithium and Sungrow Power topped the pack with significant gains. Financial firms advanced as Chinese banks began to decrease deposit rates in order to protect their interest margins. The tech sector advanced as well, driven by gains from Zhongji Innolight and TRS Information.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 2.25% and 1.91% higher at $71.67 and $75.59 respectively. Gold futures prices settled 1.79% lower at $1979.90.

Week’s Highlights

- The National Treasury released its quarterly economic and budget analysis for Q3 of the 2022-2023 fiscal year. Current account deficits in March 2023 stood at USD 5,640.9 million, compared to USD 5,537.7 million in March 2022. In March 2023, foreign exchange reserves were at USD 6,961.8 million (3.90 months of import cover), falling short of CBK’s statutory obligation to provide import coverage of at least 4.0 months. However, in March 2022, the foreign reserves stood at USD 8,432.2 million (5.0 months of import cover), well above CBK’s requirement. Revenue collection totalled KES 1,686 billion between July 2022 and March 2023, falling short of the targeted amount of KES 1,773.4 billion by KES 87.4 billion. Total expenditure stood at KES 2,209.2 billion. For the period under review, net foreign and domestic finances were KES 80.1 billion and KES 287.8 billion respectively. Gross domestic debt increased to KES 4,539.6 billion in March 2023 from KES 4,192.4 billion in March 2022 while total external debt stock stood at KES 4,851.1 billion by the end of March 2023.

- Moody’s Investors Service has downgraded Kenya’s long-term foreign-currency and local currency issuer ratings to a B3 rating indicative of financial instability concerns or inadequate cash reserves relative to business needs, debt and other financial obligations. The downgrade stems from the Kenyan government’s elevated liquidity risks, partly as a result of deteriorating domestic debt uptake, particularly long-term bonds. This has resulted in budget deficits and delays in the clearance of government department arrears. The agency has also placed the ratings under review for downgrade as it monitors the country’s ability to channel domestic debt towards a majority of the net financing needs while reserving external financing for pressing external debt repayment obligations. While the country continues to rely on the IMF and other international institutions for funding, its ability to sustain market access for commercial external debt is critical for debt servicing.

- The Central Bank of Kenya (CBK) has published the bank supervision annual report for the fiscal year 2021-2022. CBK, in the report has given a detailed account on the economic and financial developments for the period. The balance of payments deficit in comparison to GDP is estimated to have increased marginally to 5.3% from 5.1% in the previous year. Government revenue in the year stood at KES 2,177.9 billion which translates to 17.2% of GDP in comparison to KES 1,815.1 billion in 2021. Tax revenue accounted for 85.4% of the revenue. Government spending and net lending increased by 7.5% to KES 2,955.0 billion accounting for 23.4% of GDP, and falling short of the projected target.

- The Retirement Benefits Authority has granted Britam regulatory approval to administer Tier II contributions from businesses that choose not to participate in the National Social Security Fund (NSSF). Britam becomes the fourth pension provider after Enwealth, CPF and ICEA Lion Life Assurance to receive this approval. The financial services provider guarantees to support qualified employers and companies with the opt-out process and to protect employees’ retirement savings.

- Central Bank of Kenya (CBK) data indicates a decline in customer deposits in the microfinance industry. Customer deposits in the microfinance business declined 7.8% to KES 46.5 billion in 2022 from KES 50.4 billion in 2021, according to CBK. The observed decrease in deposits is attributable to the shift of funds to alternative attractive investments with the general rise of interest rates. In a rising interest rate environment, government securities such as Treasury bills and bonds provided investors with higher risk-adjusted returns, which served to buffer investors against shocks such as excessive inflation.

- In the United Kingdom(UK), GDP grew by 0.1% in Q1 of 2023 despite the unexpected 0.3% decline in March 2023. The observed growth was consistent with market forecasts for the period. Construction and manufacturing showed solid growth expanding 0.7% and 0.5% respectively in the quarter. The services and production sector experienced a slower growth of 0.1% as services dropped by 0.5% in March due to declines in wholesale and retail trade as well as motor repairs. Household consumption showed no growth in the quarter. The Bank of England also reported that the UK is no longer expected to enter a recession this year.

- Euro Area inflation stood at 7% in April 2023 up from 6.9% in March, and well above the European Central Bank’s target of 2%. Service and energy costs rose by 5.2% and 2.4%, respectively. However, inflation in food, alcohol and tobacco as well as non-energy industrial products eased. Rising service and energy prices more than offset the slowing of food price growth. Core inflation, which excludes volatile food and fuel prices, fell to 7.3% from 7.5%, while an even narrower gauge, which excludes alcohol and tobacco, fell to 5.6% from 5.7%. Interest rate hikes are still expected as policymakers work to keep inflation under control and meet their target.

- Eurozone’s quarterly economic growth was confirmed at 0.1% in Q1 of 2023, following an inert previous quarter. Multiple factors have had a substantial impact on the bloc’s economy, including a large increase in consumer prices caused by increasing energy and food costs. Furthermore, the European Central Bank’s strong tightening of monetary policy, the fastest in over two decades, has added to the economic burden, as has a decline in business and consumer confidence. Germany, the Eurozone’s largest economy, recorded no growth in the first quarter, while the Netherlands contracted. However, the economies of France, Italy, and Spain expanded during the same time period.

Get future reports

Please provide your details below to get future reports: