Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,566 million (3.67 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Sterling Pound and the Euro to exchange at KES 128.89, KES 153.10 and KES 136.09 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 4.43% | 1.05% |

| Sterling Pound | 2.94% | 0.35% |

| Euro | 3.36% | 0.52% |

Liquidity

Liquidity in the money markets increased with the average interbank rate declining from 6.88% to 6.59%, as government payments offset tax remittances. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.88% | 6.59% |

| Interbank volume (billion) | 11.61 | 31.17 |

| Commercial banks’ excess reserves (billion) | 14.70 | 14.90 |

Fixed Income

T-Bills

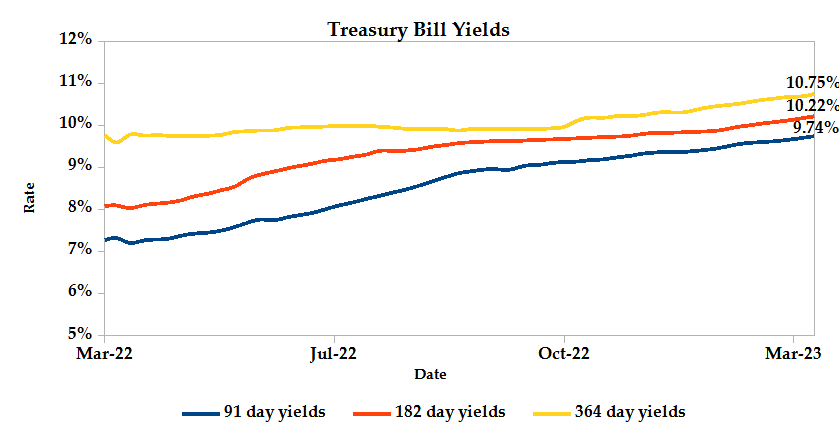

T-Bills remained over-subscribed during the week, with the overall subscription rate recorded as 148.47%, up from 136.25% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 501.03% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 79.11% and 76.81% respectively. The acceptance rate increased by 24.19% to close the week at 90.34%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover declined by 11.22% from KES 9.46 billion in the previous week to KES 8.40 billion. Total bond deals decreased by 39.15% from 659 in the previous week to 401.

In the primary, CBK released auction results of the newly issued 17-year amortized infrastructure bond; IFB1/2023/017, which sought to raise KES 50.0 billion. The issue was oversubscribed receiving bids worth KES 59.77 billion, representing a performance of 119.54%. KES 50.88 billion worth of bids were accepted at a weighted average rate of 14.40%.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average 0.01% compared to the previous week, 0.78% month to date and 0.24% year to date. The yields on the 10-Year Eurobonds for Ghana and Angola declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | -1.09% | 0.58% | -0.60% |

| 2018 10-Year Issue | 0.73% | 1.03% | 0.20% |

| 2018 30-Year Issue | 0.44% | 0.70% | 0.19% |

| 2019 7-Year Issue | 0.15% | 0.61% | -0.25% |

| 2019 12-Year Issue | 0.55% | 1.01% | 0.35% |

| 2021 13-Year Issue | 0.66% | 0.73% | 0.14% |

Equities

NASI, NSE 20 and NSE 25 settled 6.56%, 1.57% and 4.34% lower compared to the previous week bringing the year to date performance to -7.42%, -4.00% and -4.49% respectively. Market capitalization lost 6.58% from the previous week to close at KES 1.84 trillion recording a year to date decline of 7.45%. The performance was driven by losses recorded by large-cap stocks such as Safaricom, Equity, EABL, KCB and Co-operative of 12.15%, 4.76%, 3.14%, 2.35% and 1.96% respectively. These were however mitigated by the gains recorded by Standard Chartered and ABSA of 2.61% and 1.21% respectively.

The Banking sector had shares worth KES 345M transacted which accounted for 22.78% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 33M transacted which represented 2.19% and Safaricom, with shares worth KES 1.1B transacted represented 73.34% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Flame Tree | 12.73 % | 13.76% |

| Sasini | 11.36% | 13.64% |

| Express | 7.56% | 13.18% |

| Stanbic | 6.62% | 8.75% |

| HF Group | 11.11% | 6.38% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Total | -19.71% | -13.54% |

| Safaricom | -14.35% | -12.15% |

| Standard Group | -13.88% | -10.89% |

| E.A Portland | -7.35% | -10.00% |

| Liberty | -10.52% | -9.80% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.94 | 1.26 | 33.87% |

| Derivatives Contracts | 17 | 23 | 35.29% |

| I-REIT Turnover (million) | 0.55 | 0.42 | -24.28% |

| I-REIT deals | 44 | 52 | 18.18% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 0.98% | -4.55% |

| Dow Jones Industrial Average (DJI) | -3.70% | -4.43% |

| FTSE 100 (FTSE) | 2.57% | -2.50% |

| STOXX Europe 600 | 4.56% | -2.21% |

| Shanghai Composite (SSEC) | 3.64% | -2.95% |

| MSCI Emerging Markets Index | -0.76% | -3.31% |

| MSCI World Index | 2.17% | -3.65% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -1.57% | -1.25% |

| JSE All Share | 3.41% | -2.25% |

| NSE All Share (NGSE) | 8.14% | 0.48% |

| DSEI(Tanzania) | 0.14% | -1.50% |

| ALSIUG (Uganda) | -3.68% | -2.97% |

US stocks experienced a significant decline this week, with Treasury yields continuing to drop due to concerns over contagion in the financial sector and stronger-than-expected employment data for February. All major stock indices ended the week lower, with Nasdaq taking the hardest hit. The Dow also recorded its largest weekly loss since June, with fears of contagion spreading across the banking sector following the closure of Silicon Valley Bank (SVB) Financial to protect deposits, amid reports of unsuccessful funding efforts.

European stock markets also closed the week lower, as tension rose ahead of the highly anticipated US jobs report, weakness in the banking sector and concerns over the health of Credit Suisse overshadowed better-than-expected UK growth data. Investors also reacted to the weak Chinese inflation data, which indicated a sluggish economic recovery in China; a significant export market for European companies.

Asian stocks faced a downward trend this week, mainly due to weaker-than-expected Chinese inflation data that indicated a slow economic recovery in the country. The Shanghai Shenzhen CSI 300 and Shanghai Composite indexes declined by 0.3% each after consumer inflation grew much less than anticipated in February, while producer inflation worsened. The data indicates that a Chinese economic rebound is expected to take longer than expected this year, which could negatively impact markets with exposure to China. Weak Chinese import demand also contributed to the decline in sentiment. Fear of a more hawkish Federal Reserve further exacerbated the situation.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 3.77% and 3.55% lower at $76.68 and $82.78 respectively. Gold futures prices settled 0.68% higher at $1,867.20.

Week’s Highlights

- The Kenya Revenue Authority (KRA) plans to compute taxes on each item imported, requiring individual traders to pay import duties, VAT, excise duty, Import Declaration Levy (IDL), and Railway Development Levy (RDL). The new measure will affect small traders importing in a pool, raise costs for consolidated cargo, and increase taxes for traders selling items in open-air markets. At present, consolidated cargo attracts a duty of KES 200 per kilogramme for air cargo or KES 2.2 million for a 40-foot container brought in through the sea.

- The Government of Kenya has selected KCB, NCBA, ABSA Bank Kenya, Stanbic Bank, Co-op Bank, and Africa Export-Import Bank to issue letters of credit worth up to KES 614.89 billion for fuel imports from the United Arab Emirates over nine months. This move is intended to ease the foreign exchange crisis, with imports set to begin next month and continue for 180 days.

- The Kenya National Trading Corporation (KNTC) has secured a KES 24 billion letter of credit from KCB Group to support the duty-free importation of 100,000 tonnes of household goods. The initiative aims to lower the cost of living by stocking 120,000 retail shops with cheap imported foods, with the government setting the retail prices of goods such as cooking oil, sugar, rice, and beans. The move seeks to stabilize the cost of basic commodities, which has seen high inflation rates and exorbitant prices of goods such as sugar and maize flour in the market.

- The Kenya Revenue Authority (KRA) plans to crack down on tax fraud and increase revenue by penalizing large companies that transact with unlisted suppliers in the electronic tax invoice registry. The registry, e-TIMS, which relays real-time sales data to KRA, will include all suppliers and not just those registered for VAT. By ignoring expenses paid to unlisted suppliers, KRA intends to reduce firms’ costs and inflate profits, which would lead to higher tax obligations. This initiative is expected to bring small and medium-sized businesses into the tax net.

- The International Monetary Fund (IMF) has temporarily increased the limits on members’ annual and cumulative access to Fund resources in the General Resources Account (GRA) to better support members facing increased financing pressures and vulnerabilities due to a challenging economic environment. The annual limit in the GRA is now 200% of quota and the cumulative limit is 600% of quota for 12 months. The IMF will also review Poverty Reduction and Growth Trust access limits once sufficient additional resources have been pledged to fill the subsidy resource gap.

- The Central Bank of Nigeria has released operational guidelines for open banking, a financial concept that allows third-party financial service providers to access banking data using Application Programming Interfaces (APIs) with the customer’s explicit consent. This allows customers to share their banking data with other financial service providers, enabling access to a broader range of products and services.

- South Africa’s GDP declined by 1.3% in Q4 2022 due to severe power shortages, resulting in scheduled blackouts that caused a loss of over USD 50 million in output per day. Eskom, the primary energy supplier, is struggling to fulfill energy demands, leading to significant disruptions across the country. The energy crisis, coupled with floods, is expected to reduce economic growth to as low as 0.3% in 2023, down from 2.5% in the previous year, as predicted by the central bank.

- China’s exports for January-February 2023 showed improvement from the previous month, but still declined by 6.8% YoY to USD 506.3 billion, marking the fourth consecutive period of decline due to weak foreign demand. The Chinese government remains concerned about a global slowdown. Notably, sales of refined products and steel products increased, while sales of unwrought aluminium and rare earths decreased. Major trade partners such as the United States, the EU, and Japan experienced significant export declines, while exports to The Association of Southeast Asian Nations (ASEAN) and Russia increased.

Get future reports

Please provide your details below to get future reports: