Month’s Highlights

- The Central Bank of Kenya (CBK) has scheduled the next Monetary Policy Committee (MPC) meeting for Thursday, November 26th, 2020. A key focus will be the weakening Kenya Shilling against the US Dollar and dwindling forex reserves.

- Kenya’s current external debt is largely skewed towards concessional terms although commercial loans in the portfolio, including Eurobonds, have impacted the cost and risk profile. Growth in domestic interest payment has doubled since 2015, with interest on Treasury bonds accounting for a higher percentage out of the total domestic interest payment during the financial year.

- The Capital Markets Authority (CMA) has proposed a waiver of listing fees for small businesses to protect them from incurring extra costs. Small businesses pay between Sh75,000 and Sh150,000 to list on the NSE. The Treasury has lined up Sh10 billion to guarantee commercial loans for small and medium enterprises (SMEs) in a bid to cushion them from the economic fallout arising from the COVID-19 pandemic.

- The African Development Fund (ADF) Board of Directors will disburse a loan of KSh 5.5 Billion ($ 50.7 Million) to Tanzania, to assist the state in responding to the COVID-19 pandemic. Tanzania is keen to support its economy by shielding businesses and households from the adverse effects of the COVID-19 pandemic.

- Zambia may enter debt default unless it pays an overdue $1 billion on the 2024 Eurobond. They missed a $42.5 million payment that was due last week in spite of the debt service suspension initiative (DSSI) window facilitated by the G20. However, Eurobond creditors were worried that should they provide the debt relief, Zambia would pay other debt services rather than towards COVID-19-related expenditures.

- Centum Investment plans to issue a Kshs 4.0 Bn housing bond with the possibility of taking up Kshs 6.0 Bn should investors’ risk appetite exceed the targeted sum. The bond is currently undergoing necessary approvals and will be issued in the next few weeks. It will be issued as a zero-coupon bond but will later be introduced in the NSE for trading.

- The Kenyan subsidiary of KCB Group was authorised to take over part of the liabilities and assets of the collapsed Imperial Bank, including Sh3.17 billion worth of deposits. In a Kenya Gazette notice dated September 8, 2020, the Competition Authority of Kenya said it approved the transfer of the assets and liabilities.

- South Sudan plans to have a new currency by replacing the South Sudanese Pound (SSP). The demonetization process will discourage hoarding, improve the economic situation, and end a crippling financial crisis. South Sudan has since independence been in a civil war with itself as well as with the northern neighbours, leading to the collapse of its economy. It ran out of foreign exchange reserves and could not stop the SSP’s depreciation.

- Crude prices dropped globally due to oversupply fears. US oil refineries in Gulf Coast states began to pick up again following a halt in production due to Hurricane Delta. Libya restarted oil production at the country’s largest field. The news of Libya resuming production also added to fears of oversupply, which have been growing ever since a number of countries began reporting second waves of Covid-19.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 5.87% to stand at USD 8.12 billion(4.93 months of import cover).However, this meets the CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

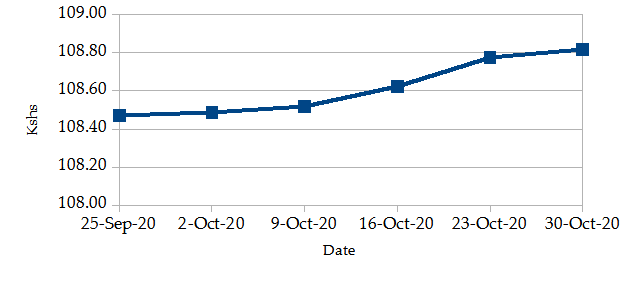

The Kenyan Shilling depreciated against the USD by 0.32% exchanging at Kshs 108.82 at the end of the month up from Kshs 108.47 in the previous month. The depreciation is due to increased dollar demand and reduced foreign exchange inflows. There was also increased demand from energy and merchandise importers which exceeded supply from remittance, horticulture exports and tourism.

USD Vs KSHS

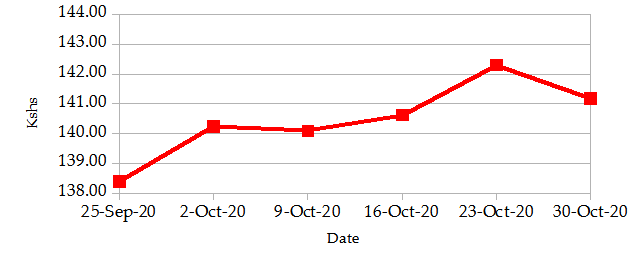

STERLING POUND Vs KSHS

Inflation

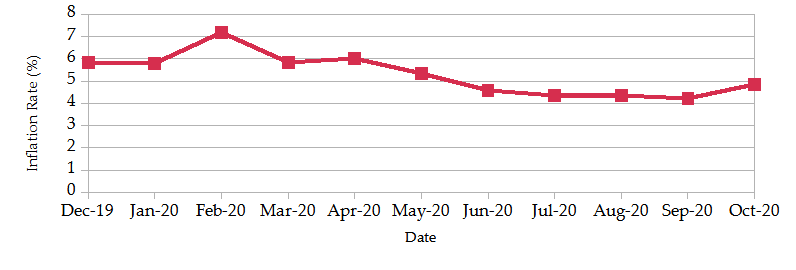

The overall year-on-year inflation increased to 4.84% in the month of October up from a revised figure of 4.20% in September. The increase is attributable to increased transport, electricity and food prices. The month-to-month food and non-alcoholic drinks’ index rose by 1.14% in October 2020 while year-on-year food inflation increased by 5.76%. This was contributed by an increase in prices of carrots, mutton and wheat flour-white among other food items. The price of kerosene rose by 0.7%

INFLATION EVOLUTION

Liquidity

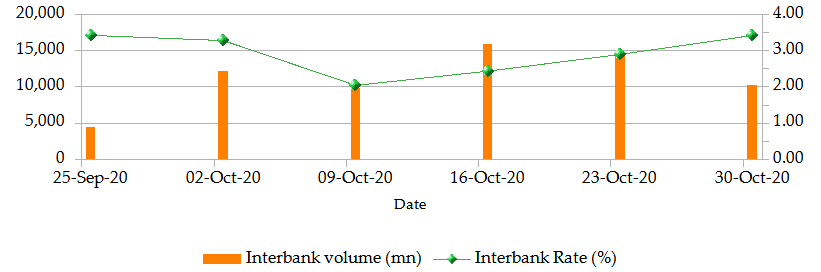

During the month, liquidity eased during the month of October as a result of government payments which partly offset tax receipts. The inter-bank rate was relatively stable at 3.42%. The volume of inter-bank transactions increased from Kshs 4.48 billion to Kshs 10.16 billion. Commercial banks’ excess reserves decreased to Kshs 9.5 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

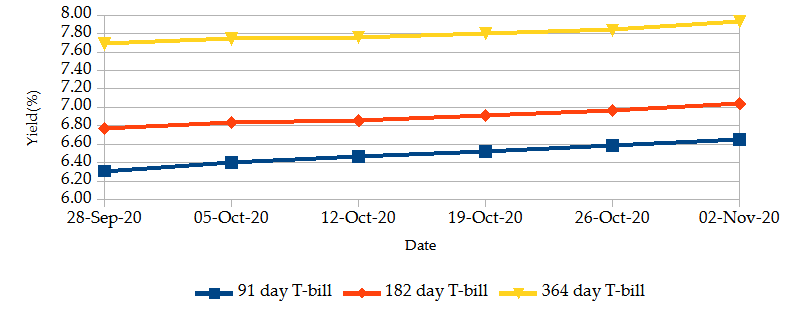

The T-bills recorded an overall subscription rate of 81.62% at the end of month of October, compared to 54.40% recorded in the previous month. The increase in subscriptions is due to an increase in market liquidity from an increase in commercial banks’ excess reserves and a decrease in the average interbank rate. The performance of the 91-day, 182-day and 364-day papers stand at 127.05%, 44.82% and 100.25% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 5.45%, 3.91% and 3.16% respectively to 6.65%, 7.04% and 7.93%.

T-BILLS

T-Bonds

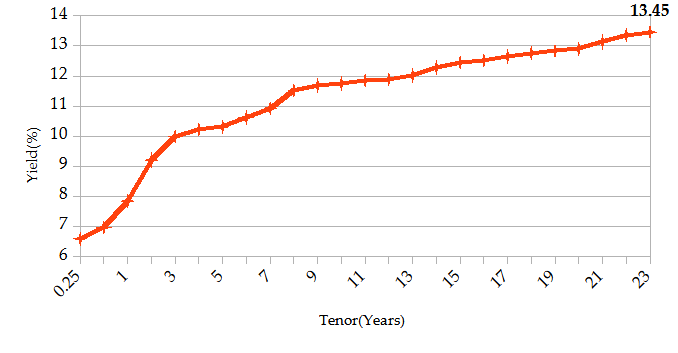

Over the month of October, the T-Bonds registered a total turnover of Kshs 69.91 billion from 1,566 bond deals. This represents a monthly decrease of 17.36% and 14.11% respectively. The yields on government securities in the secondary market remained relatively stable during the month of October.

In the international market, yields on Kenya’s Eurobonds declined by an average of 26.4 basis points.

YIELD CURVE

EQUITIES

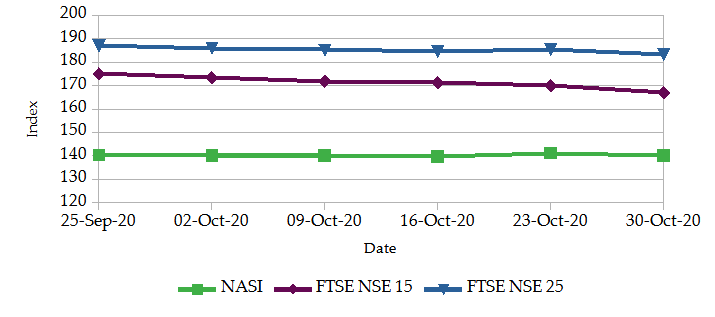

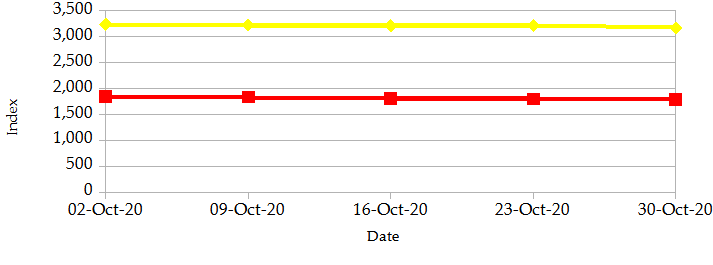

During the month of October, NASI, NSE 20 and NSE 25 decreased by 0.2%, 3.5% and 2.2% respectively on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 decreased by 0.8%, 0.9% and 1.4%. The drop in NASI is a result of the depreciation of large-cap stocks such as Sameer Africa Plc, Centum Investment, KCB Group and HF Group. At the close of the month, market capitalization decreased by 0.23% to Kshs 2.15trillion. Also, total shares traded and equity turnover decreased by 12.4% and 0.8% respectively to 17 million shares and Kshs 0.50 billion.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25TS

ALTERNATIVE INVESTMENTS

- Standard Investment Bank (SIB) announced that it would be offering investors alternative investment options outside the NSE. The multi-asset strategy fund dubbed Mansa-X will offer regional investors access to a wide variety of global investment products such as gold, oil, gas and foreign currencies.

- The uptick in e-commerce and online shopping is evident in markets around the continent. Jumia, Africa’s largest e-commerce, recorded a year-on-year increase in demand of almost four times in Q1 2020 compared to Q1 2019.

- SportPesa will be under a new Betting Control and Licensing Board (BCLB) license. Milestone Games Limited acquired the rights to use the SportPesa brand name in Kenya thus marking the return of the betting giant. SportPesa exited the Kenyan market in September 2019 following the revocation of its license by BCLB for failure to meet tax compliance policies.

- Visa Inc. has announced it has finalized the acquisition of YellowPepper, a fin-tech company that operates in Latin America and the Caribbean. YellowPepper’s technology will enable Visa to become a single point of access for initiating any transaction type and enabling the secure movement of money.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -5.64% | -0.06% |

| STOXX Europe 600 | -5.56% | -3.70% |

| Shanghai Composite (SSEC) | -1.63% | 0.16% |

| MSCI Emerging Market Index | -2.90% | 4.32% |

| MSCI World Index | -5.66% | -0.32% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -0.97% | 2.23% |

| JSE All Share | -9.62% | -6.47% |

| NSE All Share (NGSE) | 6.39% | 16.00% |

| DSEI (Tanzania) | -0.15% | -0.88% |

| ALSIUG (Uganda) | -1.33% | -2.63% |

- During the month, major global markets had mixed returns as the Covid-19 pandemic had a resurgence in some regions. In the USA, the S&P 500 and Dow Jones indices declined by 0.06% and 1.70% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and UK’s FTSE 100 declined by 3.70% and 4.54% respectively.

- On a regional front, most markets had mixed returns. The FTSE ASEA Pan African index, representing the overall African markets, increased by 2.23% from the month of September. South Africa’s JSE All Share dropped by 6.47%, Uganda’s All Share Index declined by 2.63% and Tanzania’s DSEI decreased by 0.88%. However, the Nigeria’s All-share index rose by 16.00%.

- On the global commodities markets, the crude prices continued to drop due to oversupply fears. US oil refineries in Gulf Coast states began to pick up again following a halt in production due to Hurricane Delta and Libya restarted oil production at the country’s largest field. The Crude Oil WTI futures plunged by 11.08% from the previous month of September. Also, the ICE Brent Crude Oil decreased in value by 10.70%.

- During the month, major global economies had mixed returns global rating agency Moody’s cut UK’s debt rating after Britain failed to reach a comprehensive post-Brexit trade deal with the European Union by the deadline it set itself.. China reported a GDP growth of 4.9% in the months of July to September compared to a similar period last year. China’s recovery has been driven by rebound in consumer spending as more people come out of their homes to spend money in the physical shops.

Get future reports

Please provide your details below to get future reports: