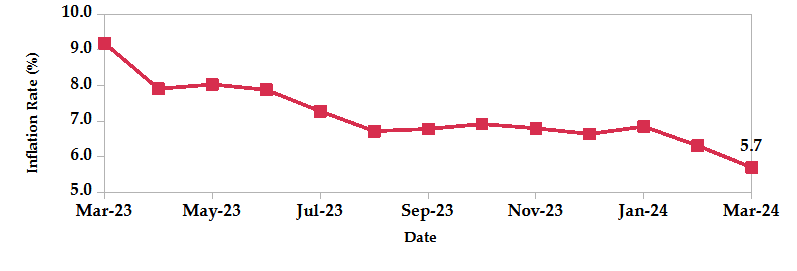

Inflation declined for the second month in a row to a two-year low of 5.7% in March 2024, down from 6.3% in February and below market expectations of 6.0%. This was primarily driven by lower fuel prices. The food and non-alcoholic beverages index edged 0.5% higher, attributed to an increase in food prices. Despite the decrease in kerosene and electricity prices, the housing, water, electricity, gas and other fuels index increased by 0.2%, mainly due to the increase in gas/LPG prices. Furthermore, the transport index decreased by 0.6%, attributed to a drop in petrol and diesel prices.

The president signed the Affordable Housing Bill 2023 into law. This law provides a 15% tax benefit for employees while establishing the Affordable Housing Levy (AHL) of 1.5% collected by employers. The levy, collected by KRA effective 19th March 2024, will be matched by employers. The contributions go towards the government’s goal of increasing housing affordability. While the Act itself doesn’t change existing taxes, a planned reduction in turnover tax for the informal sector from 3% to 1.5% is expected in a separate bill.

The government issued a directive outlining several cost-cutting measures. State corporations must resubmit their annual budgets, which are capped at 70% of the previous year’s allocation. New projects require National Treasury approval and commercial corporations must allocate 80% of profits for dividends. Regulatory bodies must remit most surplus funds to the Consolidated Fund. Additionally, the directive prohibits spending surplus revenue, memberships and unnecessary board expenses. Subsistence allowances and car reimbursements are restricted to approved travel only.

The Central Bank of Kenya (CBK) issued licenses to 19 new Digital Credit Providers (DCPs), bringing the total to 51, in an effort to address concerns about high-cost credit and broaden access to potentially more competitive loan options. This expansion follows the licensing of 32 DCPs in March 2023 and reflects the growing interest in this sector, as evidenced by the 480 applications received since March 2022. CBK has also collaborated with relevant regulators, like the Office of the Data Protection Commissioner, to ensure a responsible licensing process.

The Federal Reserve held interest rates range at a record high of 5.25%–5.5% in March, making the fifth consecutive meeting with no rate adjustments aligning with the market expectations. However, policymakers still plan to cut interest rates three times this year, similar to their December forecast. The Fed revised upwards its GDP growth projections for 2024, 2025 and 2026 to 2.1%, 2.0% and 2.0% respectively. PCE inflation forecasts remained unchanged for 2024 at 2.4% but were slightly raised for 2025 to 2.2%. The core inflation rate is also expected to be higher in 2024 at 2.6%, with no changes predicted for 2025. Moreover, the Fed projects a lower unemployment rate of 4% in 2024, compared to their earlier December forecast of 4.1%. Projections for 2025 remained unchanged at 4.1%.

The Caixin China General Manufacturing PMI rose to 51.1 in March 2024, a 13-month high exceeding market expectations of 51. This marks the fifth consecutive month of expansion, driven by a surge in domestic and foreign new orders, with foreign sales experiencing their strongest growth in a year. Production has increased at its fastest pace since May 2023. However, firms remain cautious about hiring, leading to continued job decline. Inflationary pressures eased for the first time since July 2023, with manufacturers lowering selling prices to stimulate demand. Notably, sentiment in the manufacturing sector is at its highest level since April 2023, buoyed by optimism surrounding the rising activity and an improved global economic outlook.

Eurozone inflation fell to 2.6% year-on-year in February 2024, marking the lowest rate in three months. However, it remains above the European Central Bank’s target of 2%. Energy prices saw a significant decline of 3.7% compared to a 6.1% decrease in January. The pace of price increases was also moderated for food by 3.9% and for non-energy industrial goods by 1.6%. Service sector inflation remained unchanged at 4.0%. The core inflation rate, excluding volatile food and energy prices, held steady at 3.1%, its lowest level since March 2022. Additionally, consumer prices rose by 0.6% on a monthly basis in February.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves increased by 1.81% to settle at USD 7.09 billion (3.80 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

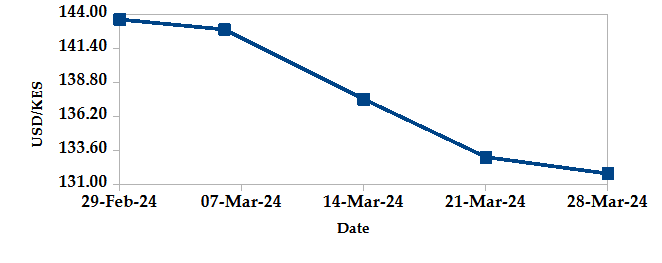

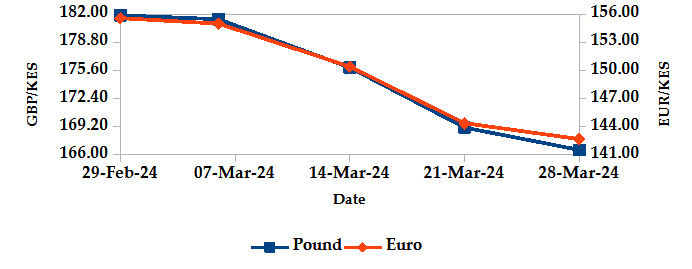

The Kenyan Shilling appreciated against the USD, the Sterling Pound and the Euro by 8.21%, 8.43% and 8.30%, exchanging at Kshs 131.80, Kshs 166.55 and Kshs 142.67 respectively at the end of the month, from Kshs 143.59, Kshs 181.88 and Kshs 155.59 in the previous month. The observed appreciation against the Dollar is attributed to the increased foreign inflows.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation decreased to 5.70% in March from 6.31% in February. This was primarily driven by reduced fuel prices.

INFLATION EVOLUTION

Liquidity

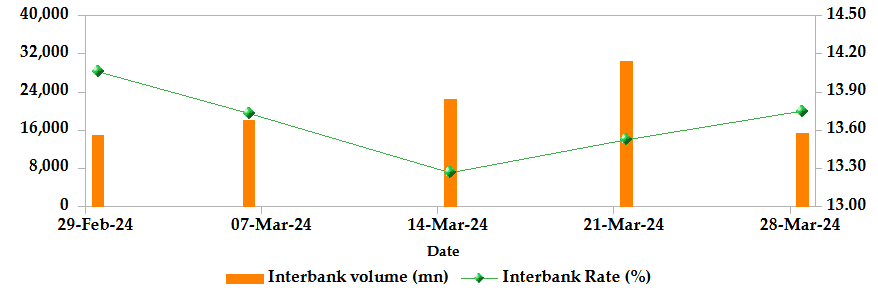

During the month, liquidity increased as a result of government payments which more than offset tax remittances. The average inter-bank rate decreased from 13.65% to 13.48%. The volume of inter-bank transactions increased from Kshs 25.00 billion to Kshs 26.64 billion. Commercial banks excess reserves decreased from Kshs 27.40 billion to Kshs 18.30 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

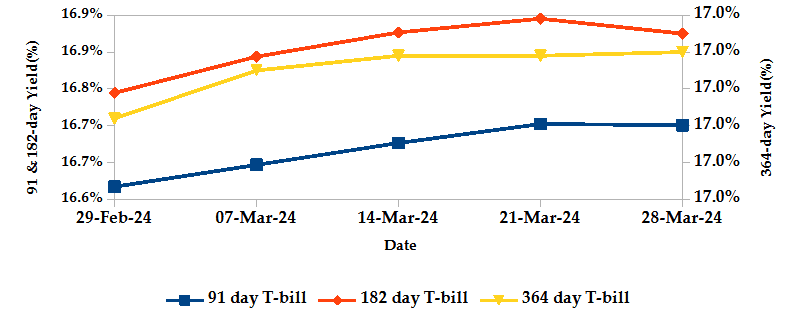

T-bills recorded an overall subscription rate of 109.13% during the month of March, compared to 161.08% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 323.15%, 51.14% and 81.52% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 0.64%, 0.61% and 0.11% to 16.73%, 16.89% and 16.99% respectively.

T-BILLS

T-Bonds

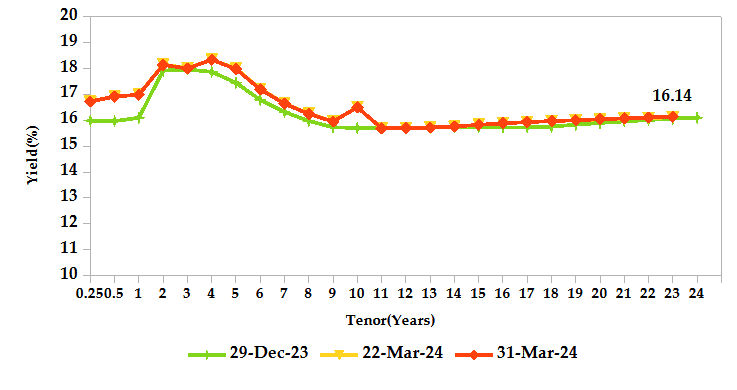

During the month, T-Bonds registered a total turnover of Kshs 125.47 billion from 3,084 bond deals. This represents a monthly decrease of 53.70% and 3.75% respectively. The yields on government securities in the secondary market increased during the month of March.

In the primary bond market, CBK re-opened FXD1/2023/005 and FXD1/2024/010 through a tap sale, seeking to raise Kshs 25.0 billion from the two treasury bonds. Furthermore, CBK re-opened FXD1/2023/002 which seeks to raise Kshs 40 Billion. The period of sale for the FXD1/2024/005 and FXD1/2024/010 runs from 27/03/2024 to 04/04/2024 while FXD1/2023/002 runs from 28/03/2024 to 17/04/2024 and their coupon rates are 16.84%, 16.00% and 16.97% respectively.

In the international market, yields on Kenya’s Eurobonds decreased by an average of 62 basis points.

YIELD CURVE

EQUITIES

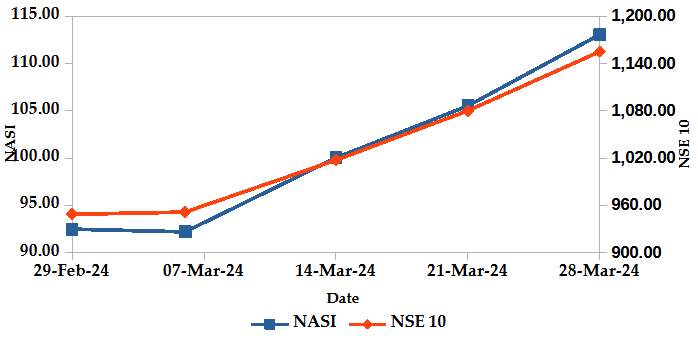

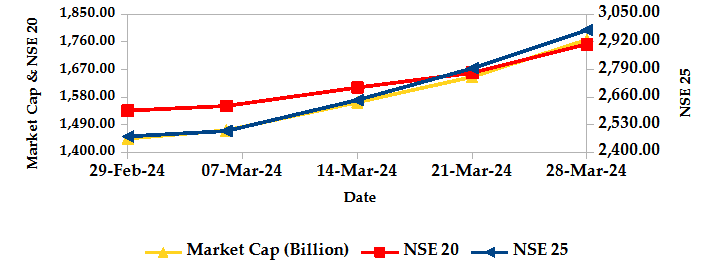

During the month, market capitalization gained 22.28% to settle at Kshs 1.77 trillion. Total shares traded increased by 132.61% to 642.04 million shares and equity turnover also increased by 143.98% to close at Kshs 11.22 billion. On a monthly basis, NASI, NSE 20, NSE 25 and NSE 10 settled 22.27%, 14.10%, 20.22% and 21.78% higher. The performance was as a result of gains recorded by large cap stocks such as KCB, Safaricom, EABL and Standard Chartered of 45.17%, 33.96%, 23.11% and 21.51% respectively.

NASI and NSE 10

Market Capitalization, NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

The derivatives market, over the month, recorded a turnover of Kshs 29.16 million with 86 contracts, which was an increase from Kshs 10.41 million with 107 contracts recorded in the previous month.

I-REIT market, over the month, recorded a turnover of Kshs 550 million with 1 deal which was an increase from Kshs 1.06 million with 97 deals recorded in the previous month.

The ETF market, over the month, recorded a turnover of Kshs 0.55 million with 2 contracts which was an increase from Kshs 3.61 million with 4 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

Global Markets

Weekly Change

Monthly Change

S&P 500

3.10%

10.79%

STOXX Europe 600

3.65%

7.14%

Shanghai Composite (SSEC)

0.87%

2.67%

MSCI Emerging Market Index

2.18%

1.81%

MSCI World

3.01%

8.47%

Regional Markets

Weekly Change

Monthly Change

FTSE ASEA Pan African Index

0.03%

-3.72%

JSE All Share

3.01%

-1.43%

NSE All Share (NGSE)

4.58%

37.60%

DSEI (Tanzania)

1.09%

1.48%

ALSIUG (Uganda)

16.67%

23.04%

Global markets registered gains during the month. In the US, the S&P 500 gained 3.10% and the Dow Jones index gained 2.08%, as investors assessed the recent Fed remarks hinting at a slower pace of future interest rate cuts. In Europe, the STOXX Europe 600 edged 3.65% higher, and the UK’s FTSE 100 indices closed higher by 4.23%, buoyed the dovish signals from central banks, particularly the Bank of England. In Asia Pacific, the Shanghai Composite (SSEC) index gained 0.87%, as investors digested the comments from Chinese legislator Zhao Leji suggesting a more open economy to foreign investors and reports of a state-owned investor buying into major companies, signalling government support for the market.

On a regional front, markets recorded a higher performance. The FTSE ASEA Pan African index, representing the overall African markets gained 0.03% from February. South Africa’s JSE All Share Index and Nigeria’s All Share Index gained 3.01% and 4.58% respectively. Furthermore, Uganda’s All Share index and Tanzania’s DSEI increased by 16.67% and 1.09% respectively.

On the global commodities markets, oil future indices edged higher, as investors awaited the upcoming OPEC+ meeting. The group is expected to assess market conditions and member compliance with production quotas but likely maintain current output levels. This aligns with comments by Russia’s Deputy Prime Minister, who emphasized production cuts over exports for the second quarter to meet OPEC+ targets. Crude Oil WTI futures and ICE Brent Crude Oil settled 6.27% and 4.04% higher to close at $83.17 and $87.00 respectively.

Get future reports

Please provide your details below to get future reports: