MONTH’S HIGHLIGHTS

- Monetary Policy Committee (MPC), retained the key policy rate at 7%, stating that the current accommodative monetary policy stance remains appropriate. Inflation is expected to remain within the target range in the near term due to muted demand pressures and policy interventions. Increased risk of inflation pressure remains due to global uncertainties. The global scene remains uncertain due to the Russia-Ukraine conflict that began at the end of February 2022 and a spike in COVID-19 cases, especially in China.

- Inflation in Kenya edged up to 5.6% in March 2022 from 5.1% in February attributable to a rise in the price of food, housing, water, electricity, gas, fuel and transport. The war in Ukraine pushed up food prices. This breaks an easing trend that has been there for the past five months.

- Kenya Pipeline Company(KPC) confirmed that it has sufficient fuel stocks following fuel shortages. Oil marketers are said to be hoarding fuel products following the failure of the government to compensate them for the rising costs of importing oil products.

- The profitability of Kenyan banks may be disrupted by the Russia-Ukraine conflict through second-order risks. According to Fitch Ratings, lenders in Kenya are not exempt from the effects of the Ukraine conflict and other global risks. The upcoming elections could also disrupt the post-pandemic recovery of banks in Kenya. While interest rate hikes to counter inflationary pressures could boost bank margins, high loan repayment default could erode these gains. Large Kenyan banks have massive deposits with less reliance on market funding and will thus override funding and liquidity risks.

- The global economic outlook remains uncertain due to the ongoing Russia-Ukraine conflict that started at the end of February, significant uncertainty about the policy responses in the advanced economies, and a spike in Covid-19 cases especially in China.

- Financial market volatility has increased amid adjustments in monetary policy in advanced economies.

- Leading indicators point to a strong performance of the Kenyan economy in the first quarter of 2022, supported by robust activity in construction, information and communication, wholesale and retail trade, transport and storage, and manufacturing sectors. The economy is expected to remain resilient supported by recovery in agriculture and continued strong performance of the services sector despite the downside risks to global growth in 2022.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 3.57% to stand at USD 7.84 billion(4.66 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

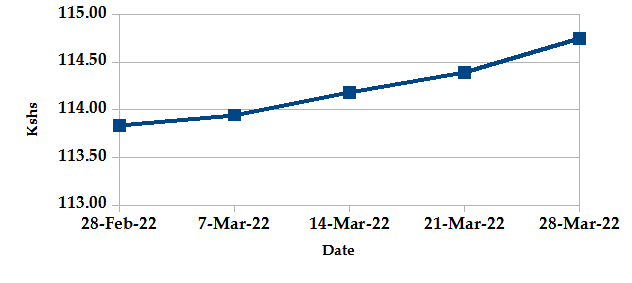

The Kenyan Shilling depreciated against the USD by 0.98%, exchanging at Kshs 114.95 at the end of the month up from Kshs 113.84 in the previous month. The depreciation is due to increased dollar demand from the oil and energy sectors. The pressure on the shilling is largely due to rising global crude oil prices and supply constraints as geopolitical pressures continue to develop in the Ukraine crisis.

USD Vs KSHS

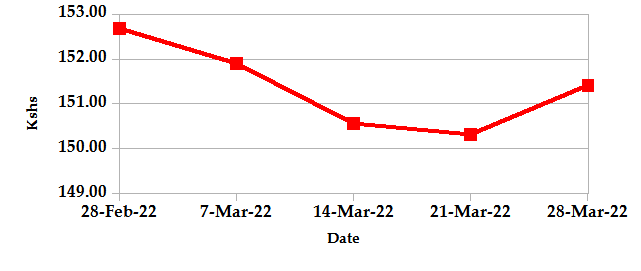

STERLING POUND Vs KSHS

Inflation

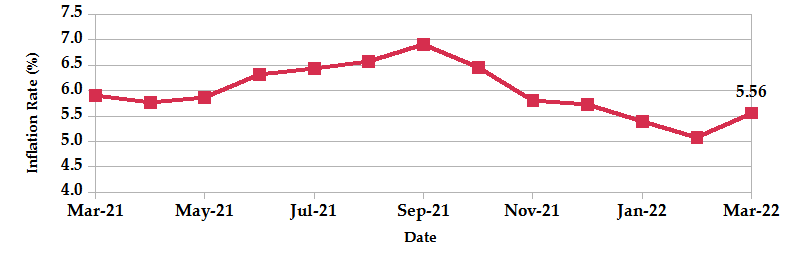

The overall year-on-year inflation increased to 5.56% in the month of March up from a revised figure of 5.08% in February. The increase is attributable to a rise in the price of food, housing, water, electricity, gas, fuel and transport. The war in Ukraine pushed up food prices, including wheat. This breaks an easing trend that has been there for the past five months.

INFLATION EVOLUTION

Liquidity

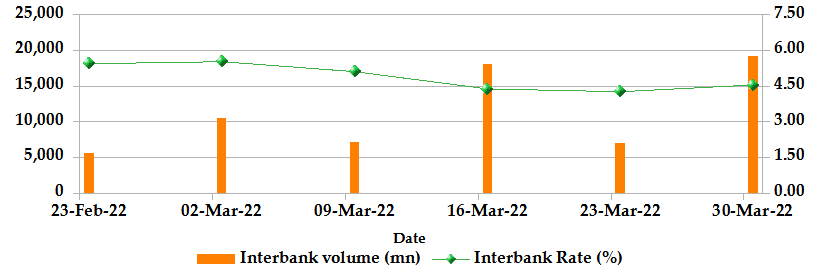

During the month, liquidity eased as a result of government payments which offset tax remittances. The inter-bank rate decreased to 4.62% down from 5.50%. The volume of inter-bank transactions increased from Kshs 5.04 billion to Kshs 14.36 billion. Commercial banks’ excess reserves decreased by 12.9% to Kshs 14.80 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

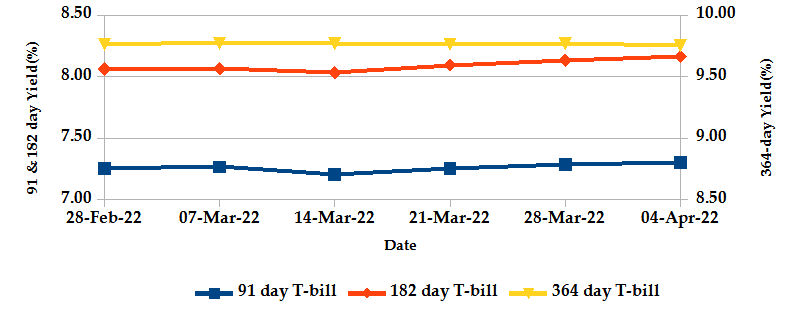

T-Bills

The T-bills recorded an overall subscription rate of 69.3% at the end of the month of March, compared to the 93.6% recorded in the previous month. The undersubscription is partly attributable to tightened liquidity in the market with the average interbank rate coming in at 4.62% compared to 4.29% in the previous week. The performance of the 91-day, 182-day and 364-day papers stands at 53.7%, 60.4% and 84.4% respectively. On a monthly basis, the yields on the 91-day and 182-day papers increased by 0.66% and 1.27% respectively to 7.30% and 8.16%. On the other hand, the yield on the 364-day paper marginally declined by 0.12% to 9.75%.

T-BILLS

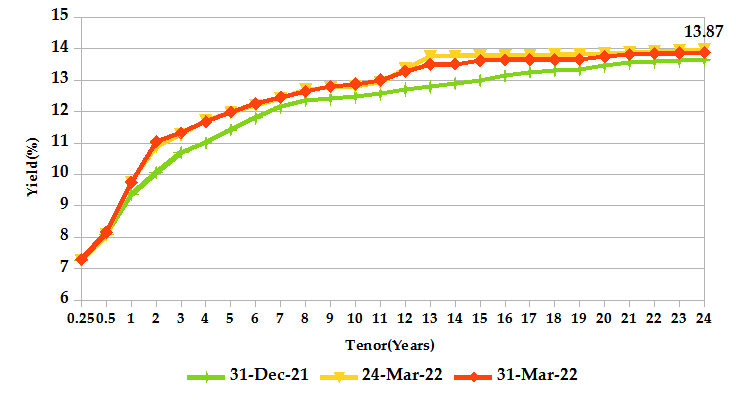

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 11.70 billion from 462 bond deals. This represents a weekly decrease of 23.1 and 25.8% respectively. The yields on government securities in the secondary market were on an upward trajectory during the month of March.

In the international market, yields on Kenya’s Eurobonds declined by an average of 44.8 basis points.

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 80 contracts having a turnover of Kshs 12.1 million which was a decrease from 107 contracts having a turnover of Kshs 14.7 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.6 million with 209 deals which was a decrease from Kshs 1.7 million with 193 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 91.9 million with 2 deals which was an increase from last month which recorded no ETF activity.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 0.23% | 3.58% |

| STOXX Europe 600 | 0.62% | 0.61% |

| Shanghai Composite (SSEC) | -0.10% | -6.06% |

| MSCI Emerging Market Index | 0.43% | -2.52% |

| MSCI World Index | 0.38% | 2.52% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -1.03% | -5.38% |

| JSE All Share | 0.40% | -1.60% |

| NSE All Share (NGSE) | -0.42% | -0.91% |

| DSEI (Tanzania) | 0.55% | -0.92% |

| ALSIUG (Uganda) | -0.58% | -1.55% |

- During the month, major global markets were mixed as investors continued to monitor developments in the Russia-Ukraine crisis and the Covid-19 outbreak in China. In the USA, the S&P 500 and Dow Jones indices gained by 3.58% and 2.36% respectively from the previous month after the release of the jobs report showing an increase of 490 thousand jobs and the unemployment rate falling to 3.7% suggesting the Federal Reserve can continue to combat inflation without hurting the economy too severely. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 appreciated by 0.61% and 0.77% respectively.

- On a regional front, most markets declined. The FTSE ASEA Pan African index, representing the overall African markets, declined by 5.38% from the month of February. South Africa’s JSE All Share declined by 1.60%, Nigeria’s All Share Index declined by 0.91%, Tanzania’s DSEI declined by 0.92% and Uganda’s All Share Index declined by 1.55%. South Africa’s rand declined against the strengthening dollar and the reimpositions of lockdowns in China following another wave of COVID-19 infections. Investors are also observing the situation in Ukraine. South Africa’s finance minister announced a cut in fuel prices to help ease pressure on consumers hit with sharply rising energy costs.

- On the global commodities markets, oil prices rose as fears of supply disruptions in the wake of Russia’s invasion of Ukraine continue to roil the market even with consuming nations set to release emergency reserves and rising Covid-19 cases likely to hit Chinese demand. Discussions of fresh sanctions by European politicians after evidence of atrocities against civilians in Ukraine added to investor concerns. The Crude Oil WTI futures surged by 4.76% from the previous month of February. The ICE Brent Crude Oil increased in value by 6.85%.

YIELD CURVE

EQUITIES

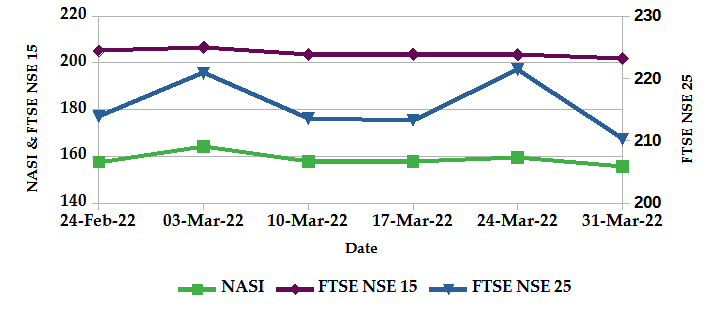

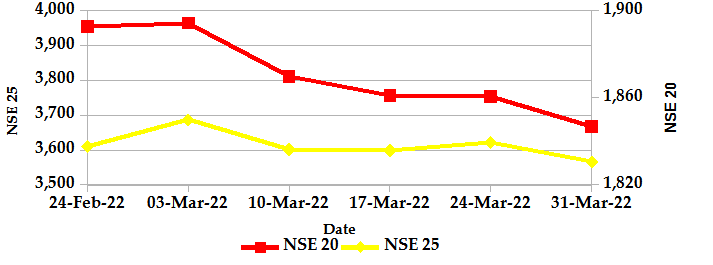

During the month of March, the market capitalization declined by 2.82% to Kshs 2.43 trillion. Total shares traded and equity turnover plunged by 42.5% and 37.3% respectively to 41 million shares and Kshs 1.5 billion. NASI, NSE 20 and NSE 25 declined by 2.8%, 2.1% and 1.5% on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 declined by 2.9%, 0.8% and 1.9% respectively. The decline in NASI is a result of the depreciation of large-cap stocks such as Kengen Company, EABL and Safaricom.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

Get future reports

Please provide your details below to get future reports: