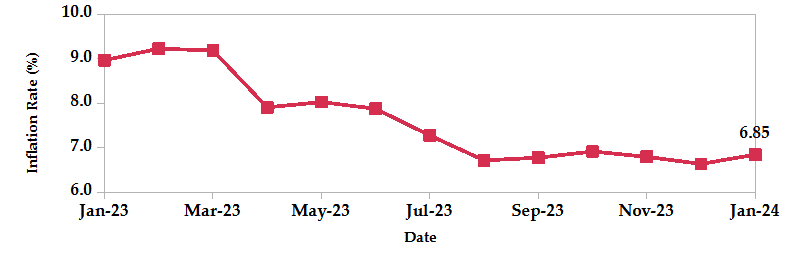

Inflation rose to 6.9% in January 2024, up from a 1.5-year low of 6.6% in December 2023. This upsurge was driven by higher food, gas and electricity prices. The food and non-alcoholic beverages index went up 0.4%, attributed to elevated food prices. The housing, water, electricity, gas and other fuels index edged up 1.6%, mainly due to heightened electricity costs, despite a decrease in kerosene prices. Furthermore, the transport index dropped 0.9% as a result of a decrease in petrol and diesel prices.

The Court of Appeal rejected the state’s application to stay the decision made by the High Court on the Finance Act ruling, implying that the 1.5% housing levy, payable by both employees and employers, remains suspended until the appeal’s final outcome. This ruling offers relief for households and businesses potentially affected by the levy, which faced legal challenges due to lack of a comprehensive legal framework. The levy was part of the June 2023 finance law that also doubled the value-added tax on fuel.

The government revised upwards NSSF deductions. Tier I deductions will rise from Kshs 360 to Kshs 420, due to a revised lower limit of Kshs 7,000 for employee contributions and a matching Kshs 420 from employers. Tier II will see a more substantial increase, from Kshs 720 to Kshs 1,740, thanks to a revised upper limit equal to the national average wage. However, a sigh of relief: Tier II calculations will still use the 2013/14 national average wage, preventing an even steeper hike. Overall, total employee contributions will increase from Kshs 2,160 to Kshs 3,180, a significant change for both employees and employers.

The IMF Board approved $684.7 million disbursement to Kenya, providing immediate financial support and recognizing progress under its economic reform program. This disbursement includes $624.5 million under the Extended Fund Facility and Extended Credit Facility (EFF/ECF) arrangements, with an increased access of $310.6 million. It also includes $60.2 million under the Resilience and Sustainability Facility (RSF). This brings total disbursements under the EFF/ECF to $2.6 billion. However, the IMF-backed revenue measures, aiming to generate an additional Kshs 806 billion over three years, face potential legal challenges in the form of court battles surrounding the proposed tax policies.

Kenya received a $210 million boost from the Trade and Development Bank in the form of syndicated loans, providing temporary relief ahead of a significant Eurobond repayment in June. It still expects additional financial support from the Pan-African lender in the near future.

The Federal Reserve kept its key interest rate unchanged within the range of 5.25%–5.5% in January 2024 for the fourth time in a row. While the Fed Chair hinted at potential rate cuts later in 2024, he emphasized that inflation remains their primary concern. Although inflation has shown slight improvement compared to last year, it still sits significantly above the Fed’s 2% target. Acknowledging this progress and a shift in risk balance towards employment, the Fed removed language suggesting future hikes from its statement. However, Chair Powell cautioned that this pause doesn’t preclude future adjustments if needed to achieve their goals of stable prices and maximum employment.

The European Central Bank (ECB) kept interest rates unchanged at record-high levels during its first meeting in 2024 and promised to keep them at sufficiently restrictive levels until inflation is back to its 2% target. For the third time in a row, the primary refinancing operations rate remained stable at 4.5%, while the deposit facility rate continued to hover around 4%. President Lagarde emphasized that any rate cuts talks were premature. Despite ending rapid hikes in September, the ECB remains vigilant due to lingering inflation and geopolitical uncertainties, like the Red Sea blockade’s potential impact on energy supplies.

The People’s Bank of China (PBoC) kept its lending rates steady at the January fixings in an effort to support economic recovery. This cautious approach saw both the one-year loan prime rate (LPR) for corporate and household loans maintain at a record low of 3.45% for the fifth consecutive month and mortgage rates remain at 4.2% for the seventh month in a row. This strategy coincided with Q4 GDP growth increasing 5.2% year-on-year, exceeding the government target. For the full year, the economy expanded by 5.2%, a significant improvement from 3.0% recorded in 2022.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves increased by 6.61% to settle at USD 7.02 billion (3.80 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

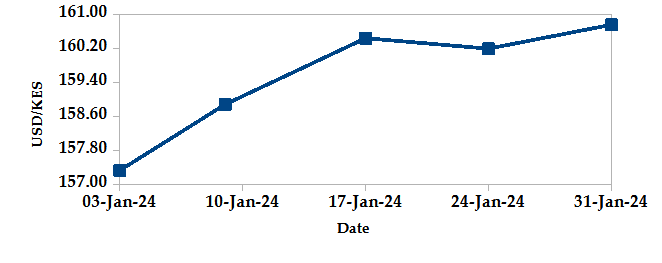

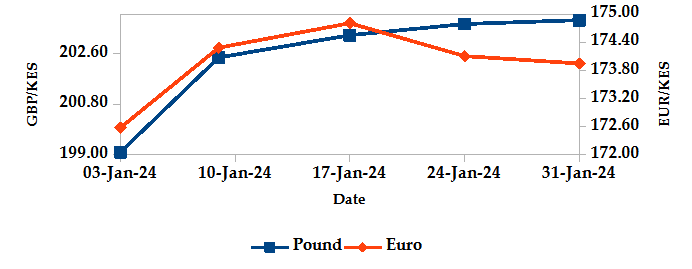

The Kenyan Shilling depreciated against the USD, the Sterling Pound and the Euro by 2.74%, 2.00% and 0.10%, exchanging at Kshs 160.75, Kshs 203.79 and Kshs 173.95 respectively at the end of the month, from Kshs 156.46, Kshs 199.80 and Kshs 173.78 in the previous month. The depreciation against the Dollar is attributed to rising demand from importers, which has caused a shortage in the market.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation increased to 6.85% in January from 6.64% in December. This was primarily driven by higher food, gas and electricity prices.

INFLATION EVOLUTION

Liquidity

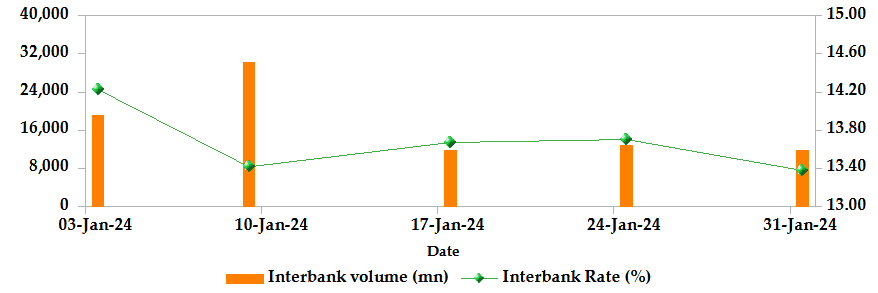

During the month, liquidity increased as a result of government payments which more than offset tax remittances. The inter-bank rate decreased from 14.44% to 13.38%. The volume of inter-bank transactions increased from Kshs 7.75 billion to Kshs 11.87 billion. Commercial banks excess reserves increased from Kshs 10.10 billion to Kshs 22.70 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

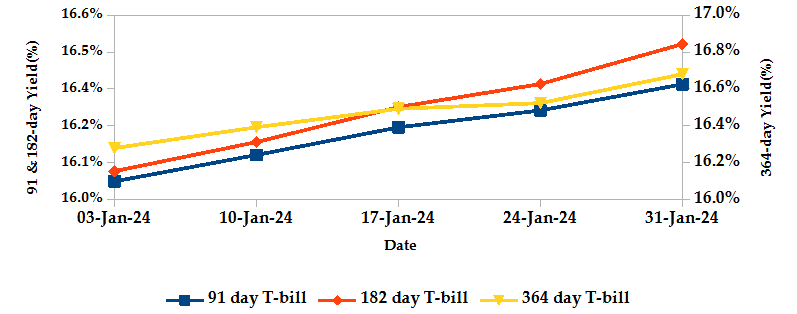

T-Bills

T-bills recorded an overall subscription rate of 146.50% during the month of January, compared to 89.94% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 668.16%, 55.75% and 28.59% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 2.45%, 3.25% and 3.60% to 16.37%, 16.51% and 16.68% respectively as investors aggressively bid to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

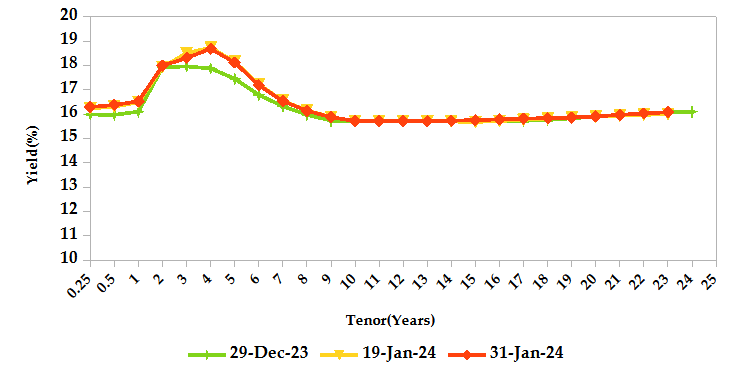

T-Bonds

During the month, T-Bonds registered a total turnover of Kshs 47.33 billion from 1,736 bond deals. This represents a monthly decrease of 9.22% and 4.46% respectively. The yields on government securities in the secondary market increased during the month of January.

In the primary bond market, CBK re-opened FXD1/2024/03 and FXD1/2023/05 through a tap sale, which sought to raise Kshs 15.0 billion. Bids were accepted at weighted average rates of 18.39% and 18.77% respectively. Additionally, the Central Bank issued a new 8.5-year infrastructure bond, IFB1/2024/8.5, seeking Kshs 70 billion. The bond coupon rate will be market-determined.

In the international market, yields on Kenya’s Eurobonds increased by an average of 47.20 basis points.

YIELD CURVE

EQUITIES

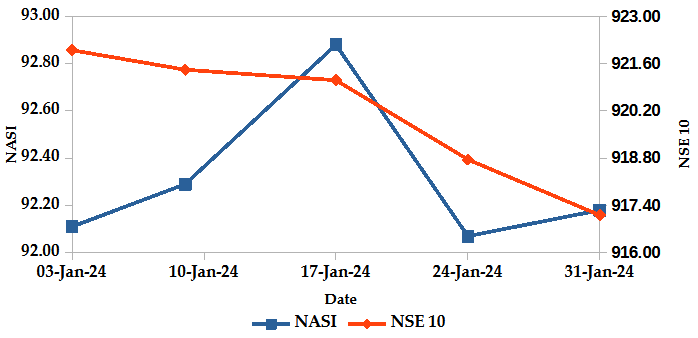

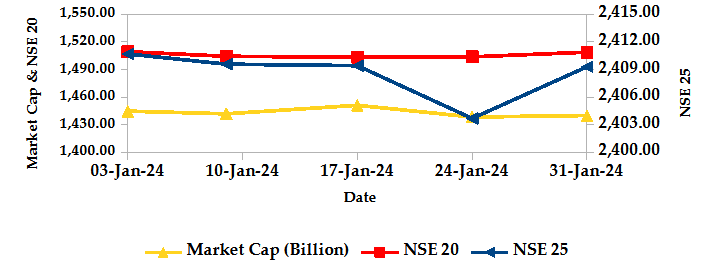

During the month, market capitalization gained 0.08% to settle at Kshs 1.44 trillion. Total shares traded decreased by 39.30% to 121.39 million shares and equity turnover went down 30.71% to close at Kshs 2.09 billion. On a monthly basis, NASI, NSE 20, NSE 25 and NSE 10 settled 0.08%, 0.51%, 1.22% and 1.06% higher. The performance was as a result of gains recorded by large cap stocks such as Equity, Co-operative and ABSA of 12.93%, 6.14% and 2.18% respectively. This was however mitigated by the losses recorded by other large cap stocks such as KCB, EABL and NCBA of 8.22%, 7.02% and 3.47% respectively.

NASI and NSE 10

Market Capitalization, NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

The derivatives market, over the month, recorded a turnover of Kshs 4.46 million with 92 contracts, which was an increase from Kshs 3.23 million with 33 contracts recorded in the previous month.

I-REIT market, over the month, recorded a turnover of Kshs 0.52 million with 73 deals which was an increase from Kshs 0.36 million with 34 deals recorded in the previous month.

The EFT market, over the month, recorded a turnover of Kshs 1.49 million with 3 contracts from no transactions in the previous month.

GLOBAL AND REGIONAL MARKETS

Global Markets

Weekly Change

Monthly Change

S&P 500

1.66%

2.24%

STOXX Europe 600

1.39%

1.15%

Shanghai Composite (SSEC)

-6.27%

-5.86%

MSCI Emerging Market Index

-4.68%

-4.77%

MSCI World

1.14%

1.14%

Regional Markets

Weekly Change

Monthly Change

FTSE ASEA Pan African Index

1.62%

0.81%

JSE All Share

-3.49%

-1.88%

NSE All Share (NGSE)

35.28%

33.11%

DSEI (Tanzania)

-1.53%

-2.28%

ALSIUG (Uganda)

-1.74%

-1.60%

Global markets were volatile during the month. In the US, the S&P 500 gained 1.66% and the Dow Jones index gained 1.22%, as investors cheered strong earnings from tech giants, particularly Meta’s impressive performance, outweighing concerns about a robust jobs report and its impact on Fed policy. In Europe, the STOXX Europe 600 edged 1.39% higher, while the UK’s FTSE 100 indices edged 1.33% lower, as investors assessed positive earnings reports and losses in technology stocks. In Asia Pacific, the Shanghai Composite (SSEC) index lost 6.27%, fueled by concerns about China’s economic slowdown and rising interest rates. Official data showed that Chinese manufacturing activity contracted for the fourth straight month in January.

On a regional front, markets recorded a mixed performance. The FTSE ASEA Pan African index, representing the overall African markets gained 1.62% from December. South Africa’s JSE All Share Index, Uganda’s All Share Index and Tanzania’s DSEI lost 3.49%, 1.74% and 1.53% respectively, while Nigeria’s All Share Index increased by 35.28%.

On the global commodities markets, oil future indices edged higher, fueled by the IMF’s upgraded global growth forecast, particularly in the US and China due to easing inflation. Crude Oil WTI futures and ICE Brent Crude Oil settled 5.86% and 6.06% higher to close at $75.85 and $81.71 respectively.

Get future reports

Please provide your details below to get future reports: