The Monetary Policy Committee (MPC) of the Central Bank of Kenya increased its benchmark rate by 50 basis points to 13.0% at its meeting on February 6, 2024, following a significant 200 basis point hike in December. This brings borrowing costs to their highest level since October 2012. The decision is a response to the challenge of rising inflation, which has persisted above the government’s 5.0% target range. All components of inflation, including fuel, food and non-food non-fuel, increased in January 2024. The MPC also highlighted ongoing pressure on the exchange rate as a contributing factor.

Inflation declined to 6.3% in February 2024, the lowest since March 2022, from 6.9% in January and below market expectations of 6.9%. This was primarily driven by lower fuel and electricity prices. The food and non-alcoholic beverages index went up by 0.3%, attributed to increased food prices. The housing, water, electricity, gas and other fuels index decreased by 0.8%, mainly due to electricity costs and kerosene prices. Furthermore, the transport index increased by 0.9% despite a decrease in petrol and diesel prices.

Kenya has officially been placed on the Financial Action Task Force (FATF) “grey list,” indicating increased monitoring to ensure compliance with international Anti-Money Laundering, Countering the Financing of Terrorism and Proliferation of Weapons of Mass Destruction (AML/CFT/CPF) obligations. This follows an assessment by the Eastern and Southern Africa Anti-Money Laundering Group (ESAAMLG) in 2022, which identified deficiencies in Kenya’s AML/CFT/CPF framework. Being on the grey list raises concerns about Kenya’s financial system and could potentially discourage international financial transactions with the country.

Kenya announced a tender offer in February 2024 to proactively manage its external debt by repurchasing a portion of its $2 billion, 6.88% Eurobond, maturing in June 2024. Citigroup and Standard Bank acted as dealer managers, while Citibank London served as a tender agent. This proactive approach aimed to manage Kenya’s external debt by smoothing the maturity profile and potentially reducing interest costs. The offer exceeded expectations, receiving strong investor interest, with tenders reaching over $1.48 billion, surpassing the initial target of $1.4 billion. Responding to the high demand, the government slightly increased the maximum acceptance amount to $1.44 billion. This successful buyback reduces its outstanding debt and strengthens its fiscal position.

The European Union Parliament has approved the Kenya-EU Economic Partnership Agreement (EPA), signed in December 2023. The agreement, which passed with 366 votes in favour, 86 against and 56 abstentions, grants duty-free and quota-free access to the massive €14 trillion EU market for Kenyan exports like flowers, tea, coffee, fish, vegetables, fruits and nuts. The EU is already Kenya’s largest export destination and second-largest trading partner, with bilateral trade exceeding €3.3 billion in 2022, a significant 27% increase compared to 2018. This agreement is expected to further boost trade and economic opportunities for both Kenya and the EU.

The Caixin China General Manufacturing PMI rose to 50.9 in February 2024, exceeding forecasts and marking the strongest growth since August 2023. New orders, particularly foreign sales, accelerated significantly. Despite cost-cutting measures keeping employment subdued, firms increased buying activity at the highest rate in 11 months. Notably, inflationary pressures remained muted, with input price growth at a seven-month low. Firms slightly reduced their selling prices to attract new business. Furthermore, business sentiment reached its strongest point since April 2023, fueled by optimism about global economic conditions and investments in new products and equipment.

Euro Area Inflation declined to 2.6% year-on-year in February 2024, down from 2.8% in January and marking the lowest rate in three months. This was mainly driven by a decrease in energy prices, which contracted by 3.7% compared to 6.1% in January. The pace of price increases also moderated across other categories, including services, food and tobacco, and non-energy industrial goods. However, core inflation, excluding volatile food and energy prices, still remained above forecasts at 3.1%, although it reached its lowest level since March 2022. Additionally, consumer prices rose slightly on a monthly basis, increasing by 0.6% in February from a 0.4% drop in January.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves decreased by 2.41% to settle at USD 6.96 billion (3.70 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

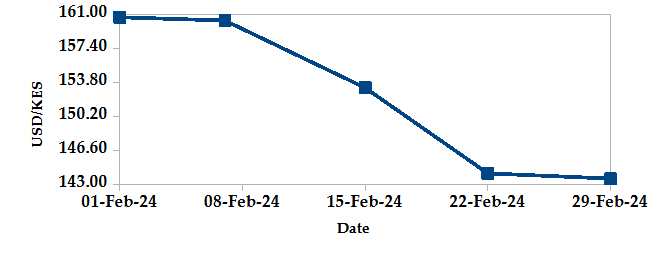

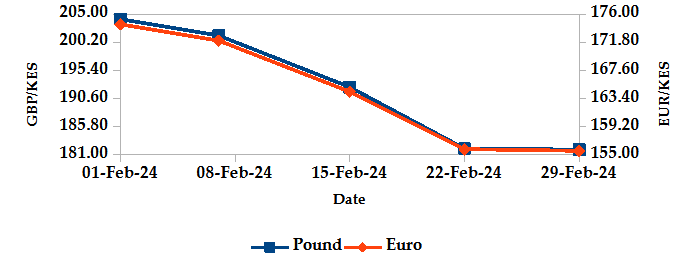

The Kenyan Shilling appreciated against the USD, the Sterling Pound and the Euro by 10.68%, 10.75% and 10.55%, exchanging at Kshs 143.59, Kshs 181.88 and Kshs 155.59 respectively at the end of the month, from Kshs 160.75, Kshs 203.79 and Kshs 173.95 in the previous month. The appreciation against the Dollar is attributed to strong investor participation in the 2014 Eurobond buyback tender which was oversubscribed, showing a boost in investor confidence, improved diaspora remittances and tourism inflows.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

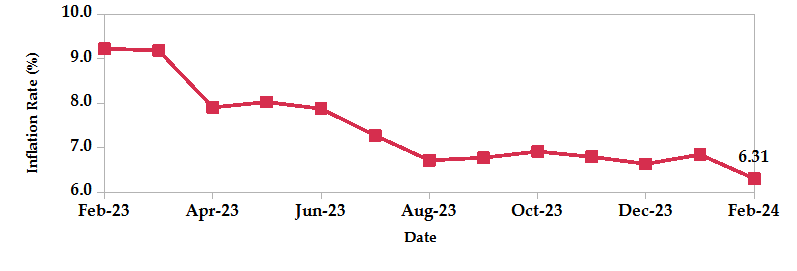

The overall year on year inflation decreased to 6.31% in February from 6.85% in January. This was primarily driven by lower fuel and electricity prices.

INFLATION EVOLUTION

Liquidity

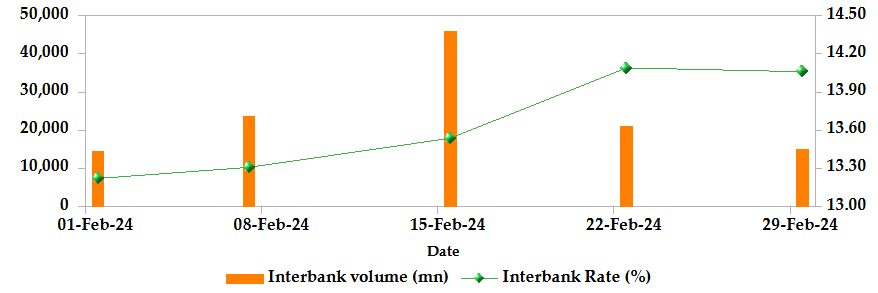

During the month, liquidity tightened as a result of tax remittances which more than offset government payments. The inter-bank rate increased from 13.38% to 14.06%. The volume of inter-bank transactions increased from Kshs 11.87 billion to Kshs 15.04 billion. Commercial banks’ excess reserves increased from Kshs 22.70 billion to Kshs 27.40 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

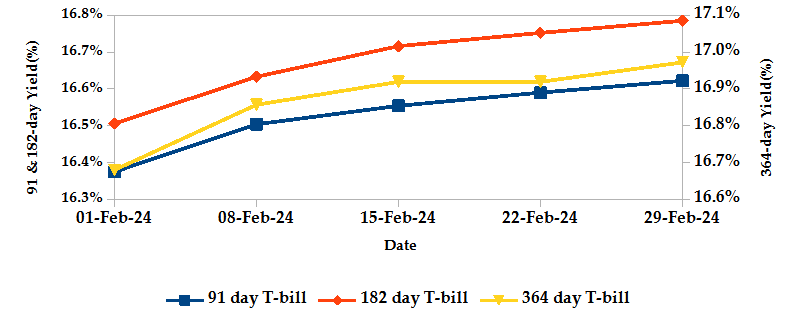

T-Bills

T-bills recorded an overall subscription rate of 161.08% during the month of February, compared to 146.50% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 518.94%, 75.33% and 103.68% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 1.51%, 1.69% and 1.75% to 16.62%, 16.79% and 16.97% respectively.

T-BILLS

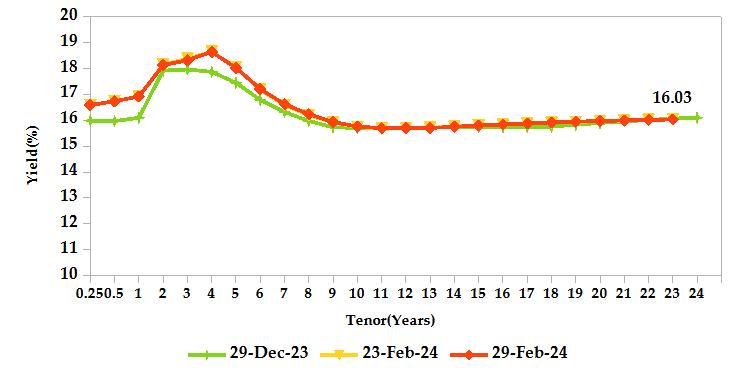

T-Bonds

During the month, T-Bonds registered a total turnover of Kshs 270.98 billion from 3,204 bond deals. This represents a monthly increase of 332.38% and 50.28% respectively. The yields on government securities in the secondary market increased during the month of February.

In the primary bond market, CBK re-opened FXD1/2024/03 and FXD1/2023/05 and issued a new FXD1/2024/10, seeking to raise Kshs 40.0 billion from the three treasury bonds. The period of sale for the FXD1/2024/03 runs from 27/02/2024 to 06/03/2024 while FXD1/2023/05 and FXD1/2024/10 runs from 27/02/2024 to 20/03/2024 and their coupon rates are 8.39%, 16.84% and 16.00% respectively.

In the international market, yields on Kenya’s Eurobonds decreased by an average of 69 basis points.

YIELD CURVE

EQUITIES

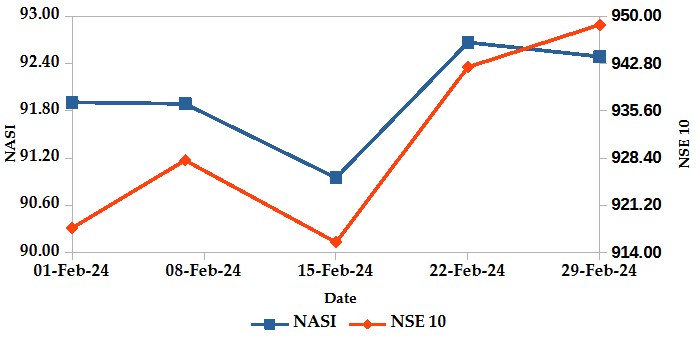

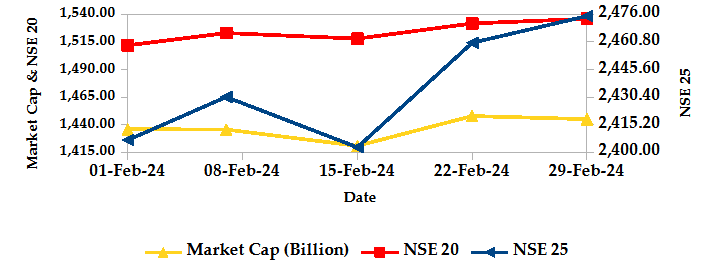

During the month, market capitalization gained 0.34% to settle at Kshs 1.45 trillion. Total shares traded increased by 82.32% to 276.01 million shares and equity turnover also increased 71.48% to close at Kshs 4.60 billion. On a monthly basis, NASI, NSE 20, NSE 25 and NSE 10 settled 0.34%, 1.79%, 2.73% and 3.45% higher. The performance was a result of gains recorded by large-cap stocks such as ABSA, Co-operative and Equity of 9.83%, 7.44% and 6.45% respectively. This was however weighed down by the losses recorded by other large-cap stocks such as Safaricom and Stanbic of 2.57% and 1.59% respectively.

NASI and NSE 10

Market Capitalization, NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

The derivatives market, over the month, recorded a turnover of Kshs 10.41 million with 107 contracts, which was an increase from Kshs 5.91 million with 102 contracts recorded in the previous month.

I-REIT market, over the month, recorded a turnover of Kshs 1.06 million with 97 deals which was an increase from Kshs 0.63 million with 92 deals recorded in the previous month.

The EFT market, over the month, recorded a turnover of Kshs 3.61 million with 4 contracts which was an increase from Kshs 1.49 million with 3 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

Global Markets

Weekly Change

Monthly Change

S&P 500

5.10%

7.45%

STOXX Europe 600

1.84%

3.36%

Shanghai Composite (SSEC)

8.13%

1.79%

MSCI Emerging Market Index

4.63%

-0.36%

MSCI World

4.11%

5.30%

Regional Markets

Weekly Change

Monthly Change

FTSE ASEA Pan African Index

-4.52%

-3.75%

JSE All Share

-2.48%

-4.31%

NSE All Share (NGSE)

-1.16%

31.57%

DSEI (Tanzania)

2.73%

0.39%

ALSIUG (Uganda)

7.16%

5.45%

Global markets generally registered gains during the month. In the US, the S&P 500 gained 5.10% and the Dow Jones index gained 2.22%, fueled by a rally in tech stocks as concerns eased around the Federal Reserve delaying interest rate cuts. In Europe, the STOXX Europe 600 edged 1.84% higher, while the UK’s FTSE 100 indices closed slightly lower by 0.01%, buoyed by signs of easing inflation. New data showed that Eurozone inflation dipped to a three-month low of 2.6% in February, aligning with ECB President Lagarde’s expectations of continued disinflation. In Asia Pacific, the Shanghai Composite (SSEC) index gained 8.13%, fueled by easing concerns about the Federal Reserve delaying interest rate cuts. Additionally, anticipation grew ahead of China’s annual plenary session, with hopes of fresh fiscal stimulus and increased support for the property and tech sectors.

On a regional front, markets recorded a mixed performance. The FTSE ASEA Pan African index, representing the overall African markets lost 4.52% from January. South Africa’s JSE All Share Index and Nigeria’s All Share Index lost 2.48% and 1.16% respectively, while Uganda’s All Share Index and Tanzania’s DSEI increased by 7.16% and 2.73% respectively.

On the global commodities markets, oil future indices edged higher, buoyed by expectations of continued supply cuts from OPEC+ and persistent tensions in the Middle East. Crude Oil WTI futures and ICE Brent Crude Oil settled 3.18% and 2.34% higher to close at $78.26 and $83.62 respectively.

Get future reports

Please provide your details below to get future reports: