MONTH’S HIGHLIGHTS

- Non-food and fuel inflation (core inflation) increased in August. Core inflation tends to be less elastic compared to headline inflation which is largely influenced by the volatile change in food and fuel prices. An increase in core inflation points to deeper price issues in the economy, and that the rise in the primary products is filtering through to other segments such as transport, healthcare, recreation and education services.

- Forex reserves recorded a significant drop recently while retaining an adequate number of months of import cover. This is despite being in breach of East Africa’s Forex reserve policy of a minimum of 4.5 months of import cover. This was attributable to the decline of the shilling and increased demand for dollars by importers.

- The Kenyan shilling hit an all-time low due to economic uncertainties surrounding the election results. The shilling has been weighed down by high oil prices and high demand from energy and manufacturing sectors. The global crude oil prices have been rising due to geopolitical tensions in Eastern Europe. The weakened shilling signalled higher cost of imported goods and inflation.

- US government and American firms are expected to announce new investments in Kenya across sectors such as energy, health and agri-business this week. The effort is part of the revival of Prosper Africa, an initiative that aims to make the centrepiece of US economic and commercial engagement with Africa.

- The Kenya Revenue Authority (KRA) plans to raise tax on petrol as part of an annual adjustment on inflation. Government plans to end the fuel subsidy that prevented prices from rising. Kenya’s expenditure on the fuel subsidy reached KSh 71 billion in the six months to June 2022. The International Monetary Fund (IMF) set a fresh loan condition requiring Kenya to drop the fuel subsidy programme by October.

- Kenya is in plans to sign an agreement with China to end double taxation of income or gains arising from trade.

- Kenya’s exports of tea, flowers, coffee and fruits to Russia were blockaded in the wake of sanctions imposed on Moscow by Western nations after its invasion of Ukraine. The exclusion of Russian banks from SWIFT will make it riskier and more expensive for Kenyan exporters, halting exports like spices, nuts and vegetables to Russia.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 4.72% to stand at USD 7.38 billion(4.20 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover but falls below the EAC region’s convergence criteria of 4.5 months of import cover.

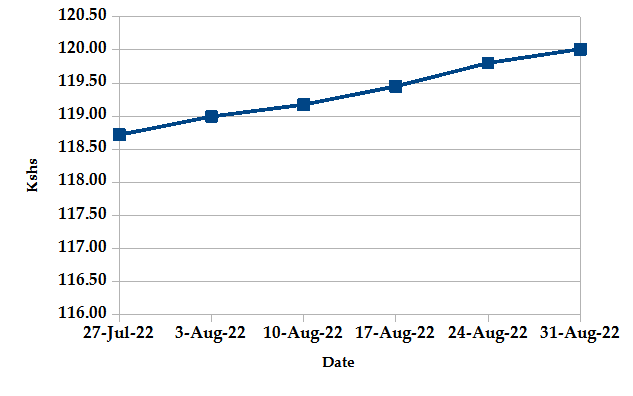

Currency

The Kenyan Shilling depreciated against the USD by 1.02%, exchanging at Kshs 120.01 at the end of the month up from Kshs 118.80 in the previous month. The depreciation is due to increased dollar demand from energy importers due to increased global oil prices and a slower-than-expected recovery in exports.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

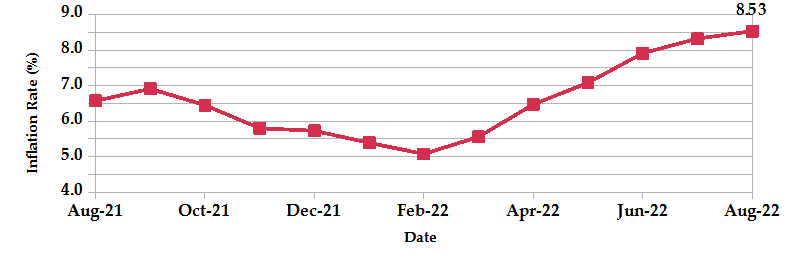

The overall year-on-year inflation increased to 8.53% in the month of August up from a revised figure of 8.32% in July. The increase is attributable to an increase in Food and Non-Alcoholic Drinks’ Index by 15.3% and the Transport Index increased by 7.6%. Housing, Water, Electricity, Gas and Other Fuels’ Index rose by 5.6%.

INFLATION EVOLUTION

Liquidity

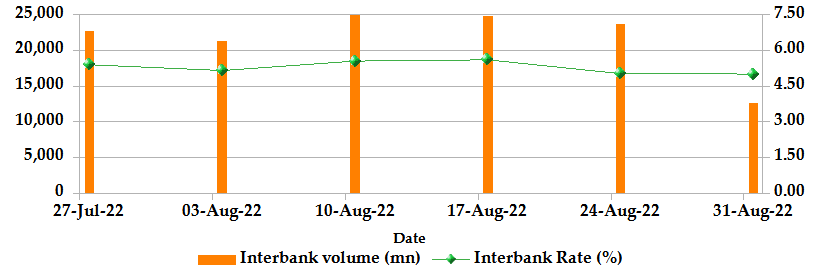

During the month, liquidity eased as a result of government payments which partly offset tax receipts. The inter-bank rate decreased to 5.00% down from 5.35%. The volume of inter-bank transactions decreased from Kshs 18.80 billion to Kshs 12.57 billion. Commercial banks excess reserves increased to Kshs 42.40 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

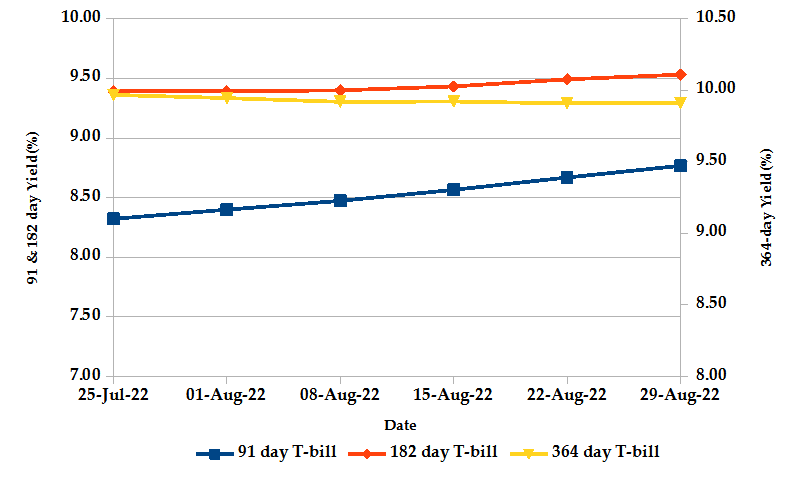

T-Bills

The T-bills recorded an overall subscription rate of 70.9% at the end of the month of August, compared to 108.6% recorded in the previous month. The undersubscription is partly attributable to investors’ uncertainty regarding the 2022 elections. The performance of the 91-day, 182-day and 364-day papers stand at 262.8%, 42.4% and 22.7% respectively. On a monthly basis, the yields on the 91-day and 182-day papers increased by 5.35% and 1.48% respectively to 8.77% and 9.53%. On the other hand, the yield on the 364-day paper marginally declined by 0.58% to 9.91%.

T-BILLS

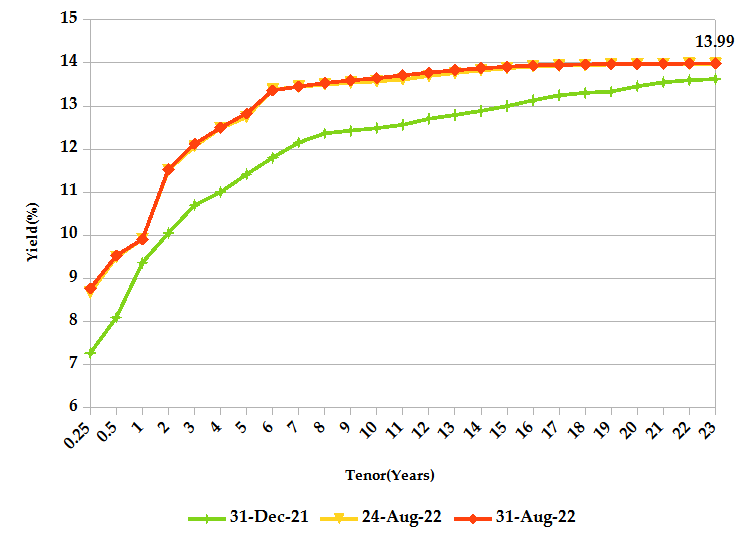

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 4.25 billion from 127 bond deals. This represents a weekly decrease of 13.7% and increase of 14.4% respectively. The yields on government securities in the secondary market remained relatively stable during the month of August.

In the international market, yields on Kenya’s Eurobonds rose by an average of 11.6 basis points.

YIELD CURVE

EQUITIES

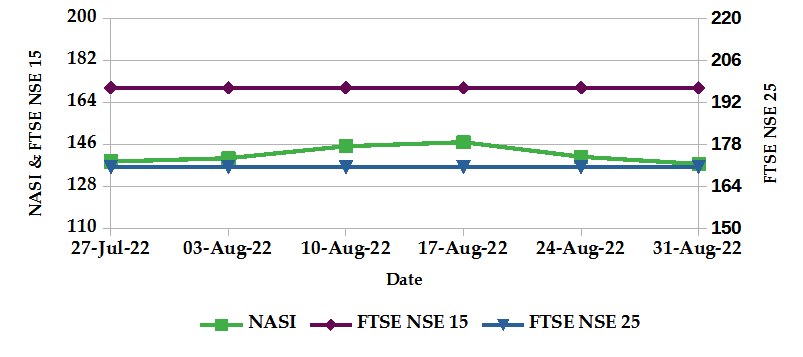

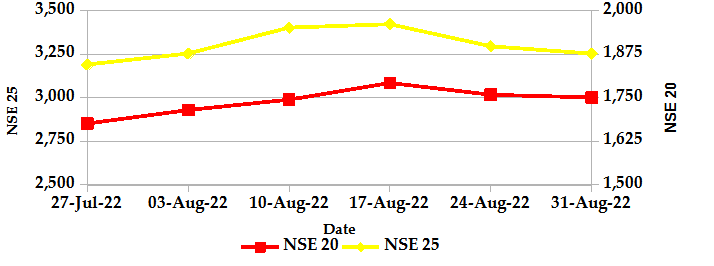

During the month of August, the market capitalization declined by 2.55% to Kshs 2.14 trillion. Total shares traded and equity turnover plunged by 35.8% and 43.6% respectively to 30 million shares and Kshs 0.76 billion. NASI and NSE 25 declined by 2.5% and 0.6% in that order, while NSE 20 gained by 2.9% on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 declined by 2.2%, 0.4% and 1.3% respectively. The decline in NASI is a result of the depreciation of large-cap stocks such as Safaricom, EABL and, KCB Group.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 163 contracts having a turnover of Kshs 7.0 million which was an increase from 148 contracts having a turnover of Kshs 5.4 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 8.5 million with 153 deals which was an increase from Kshs 1.3 million with 176 deals recorded over the last month.

- The ETF market over the month recorded no activity over the month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -4.49% | -4.24% |

| STOXX Europe 600 | -3.92% | -5.29% |

| Shanghai Composite (SSEC) | -0.41% | -1.57% |

| MSCI Emerging Market Index | 0.91% | 0.03% |

| MSCI World Index | -3.97% | -4.33% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -0.89% | -2.63% |

| JSE All Share | -3.72% | -2.78% |

| NSE All Share (NGSE) | 2.39% | -1.06% |

| DSEI (Tanzania) | -0.88% | 0.15% |

| ALSIUG (Uganda) | -2.54% | -1.26% |

- During the month, major global markets declined as investors fear that continued monetary policy tightening by central banks in the USA and Europe would trigger a recession. In the USA, the S&P 500 and Dow Jones indices declined by 4.24% and 4.07% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and UK’s FTSE 100 declined by 5.29% and 1.88% respectively.

- On a regional front, most markets declined apart from Tanzania’s DSEI. The FTSE ASEA Pan African index, representing the overall African markets, declined by 2.63% from the month of July. South Africa’s JSE All Share declined by 2.78%, Nigeria’s All Share Index declined by 1.06% and Uganda’s All Share Index declined by 1.26%. However, the Tanzania’s DSEI marginally increased by 0.15%.

- On the global commodities markets, the oil futures indices declined as investor concerns over interest rate hikes to combat high inflation lowered fuel demand. The Crude Oil WTI futures and ICE Brent Crude Oil plunged by 9.20% and 12.29% respectively from the previous month of July, Gold Futures declined by 3.12% due to strengthening of the dollar.

Get future reports

Please provide your details below to get future reports: