MONTH’S HIGHLIGHTS

- The Central Bank of Kenya (CBK) introduced a Chief Executive Officers (CEOs) Survey in March 2021. There is optimism in the business community due to the rollout of the Covid-19 vaccines and the continued reopening of the economy. The economic environment, the COVID-19 pandemic and the business environment were highlighted by CEOs as significant factors that could constrain growth.

- The Energy and Petroleum Regulatory Authority (EPRA) retained diesel, petrol and kerosene prices despite an increase in landing costs of fuel. The constant fuel prices can be attributed to a strengthening Kenya Shilling against the US dollar, meaning the country uses fewer Shillings to import crude oil.

- The Institute of Public Finance (IPF) Kenya has urged the National Treasury to freeze all new public projects and reschedule public debt repayments. Kenya’s Debt repayment rate is expected to reach 60% of all taxes collected by 2021/22.

- Kenya’s Capital Markets Authority (CMA) says it has seen renewed interest in the corporate bond market despite threats posed by Covid-19. Enforcement actions have further boosted confidence in the bond market.

- The International Monetary Fund (IMF), in its latest global outlook, expects the world economy to grow at 6% in 2021 and 4% in 2022, from a negative 3% growth in 2020. The optimistic projections are due to upgrades for advanced economies, more so the USA, which is expected to grow at 6.4% in 2021 and China at 8.4% since the economy has rebounded to pre-pandemic GDP levels.

- Kenya has been ranked as the most attractive investment destination for Japanese firms looking to invest in Africa, citing the country’s start-up community, geothermal power potential, expanding infrastructure and big motor vehicle assembly industry, according to a survey by the Japan External Trade Organization (JETRO). South Africa came second, followed by Nigeria, Ethiopia, Ghana, Mozambique and Tanzania.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves gained by 4.36% to stand at USD 7.66 billion (4.70 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

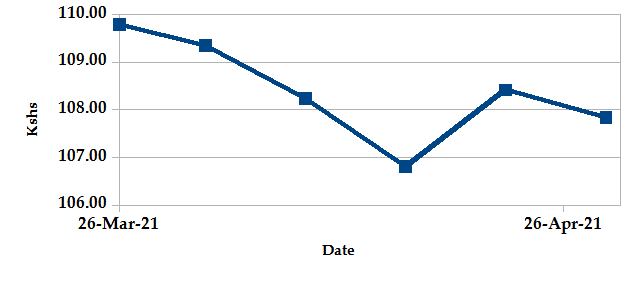

Currency

The Kenyan Shilling gained against the USD by 1.77% exchanging at Kshs 107.84 at the end of the month down from Kshs 109.79 in the previous month. The increase is due to low dollar demand from general importers. The shilling continues to be supported by Forex reserves. We expect continued pressure on the shilling due to rising uncertainties in the global markets due to the COVID-19 pandemic.

USD Vs KSHS

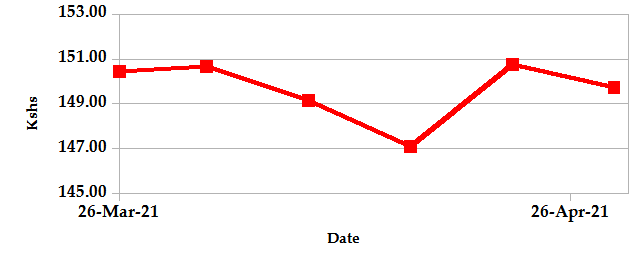

STERLING POUND Vs KSHS

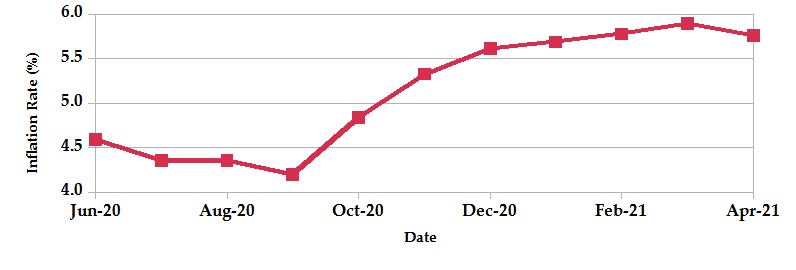

Inflation

The overall year-on-year inflation decreased to 5.76% in the month of April down from 5.90% in March. The decrease is attributable to the slowdown in fuel price increases in petrol, diesel, and kerosene which averaged Ksh 123.66, Ksh 108.58 and Ksh 98.78, the same mean as March.

INFLATION EVOLUTION

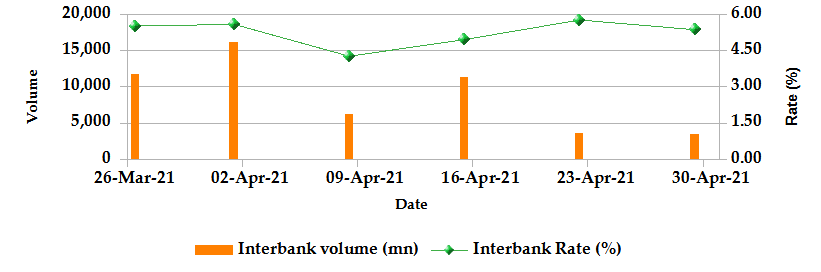

Liquidity

During the month of April, liquidity eased as a result of government payments which offset tax remittances. The inter-bank rate decreased to 4.83% from 5.52% the previous month. The volume of inter-bank transactions decreased to Kshs 9.70 billion from Kshs 11.70 billion. Commercial banks excess reserves decreased to Kshs 13.0 billion from Kshs 15.3 billion the previous month.

INTER-BANK RATE and VOLUME

FIXED INCOME

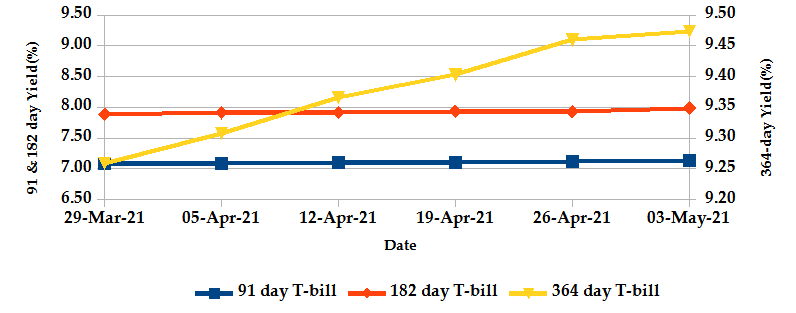

T-Bills

The T-bills recorded an overall subscription rate of 80.35% at the end of the month of April, compared to 117.14% recorded in the previous month. The decrease in subscription is due to tight liquidity in the money market. The performance of the 91-day, 182-day and 364-day papers stand at 74.78%, 26.36% and 136.58% respectively. On a monthly basis, the yields on the 91-day papers increased by 0.73% to 7.14% and yields on 182-day and 364-day papers increased by 1.25% and 2.32% respectively to 7.99% and 9.47%.

T-BILLS

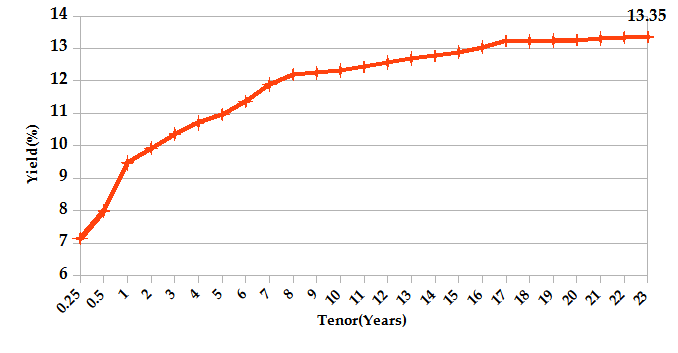

T-Bonds

Over the month of April, the T-Bonds registered a total turnover of Kshs. 75.62 billion from 2,283 bond deals. This represents a monthly increase of 37.91% and 59.32% respectively. The yields on government securities in the secondary market remained relatively stable during the month of April.

In the international market, yields on Kenya’s Eurobonds remained stable, increasing by an average of 4.0 basis points.

YIELD CURVE

EQUITIES

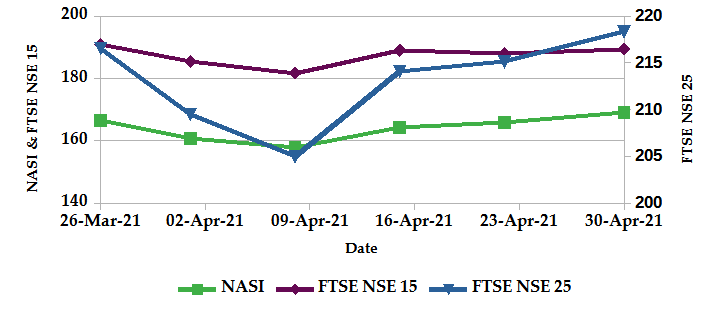

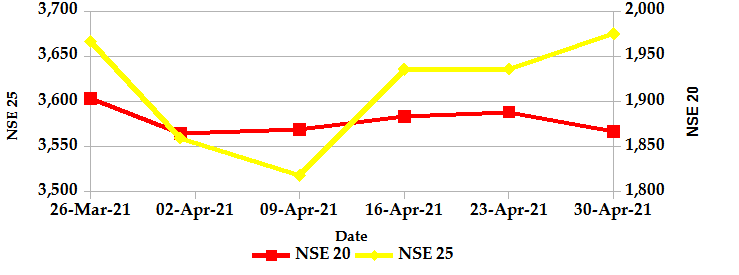

During the month of April, NASI and NSE 25 increased by 1.60% and 0.23% respectively while NSE 20 decreased by 1.92% on a monthly basis. On a weekly basis, the NASI and NSE 25 increased by 2.14% and 1.07% while the NSE 20 declined by 1.15%. The increase in NASI is a result of gains of large-cap stocks such as Safaricom and East Africa Breweries Ltd. At the close of the month, market capitalization increased by 1.60% to Kshs 2.60 trillion. Also, total shares traded and equity turnover increased to 13.4 million and 465.3 million from 10.0 million and 311.3 million respectively the previous month.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 227 contracts having a turnover of Kshs 27.97 million which was an increase from 105 contracts having a turnover of Kshs 22.79 million recorded over the last month.

- The I-REIT market over the month recorded 280 contracts having a turnover of Kshs 9.48 million which was an increase from 176 contracts having a turnover of Kshs 2.54 million recorded over the last month.

- The ETF market recorded no activity over the month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 0.02% | 5.20% |

| STOXX Europe 600 | -0.37% | 2.45% |

| Shanghai Composite (SSEC) | -0.79% | 0.83% |

| MSCI Emerging Market Index | 0.88% | 4.40% |

| MSCI World Index | 0.20% | 4.87% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 0.00% | 1.33% |

| JSE All Share | -0.62% | -0.24% |

| NSE All Share (NGSE) | 1.37% | 1.59% |

| DSEI (Tanzania) | 0.00% | 0.39% |

| ALSIUG (Uganda) | 0.00% | -3.03% |

- During the month, major global markets gained due to the rebounding of companies from the effects of COVID-19 and quarter earnings that project profit growth that will be able to support markets. In the USA, the S&P 500 and Dow Jones indices gained by 5.20% and 2.44% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 gained by 2.45% and 3.40% respectively.

- On a regional front, most markets gained. The FTSE ASEA Pan African index, representing the overall African markets, increased by 1.33% from the month of March. South Africa’s JSE All Share marginally declined by 0.24%, Nigeria’s All-share index rose by 1.59%, and Tanzania’s DSEI increased by 0.39%. However, Uganda’s All Share Index declined by 3.03%.

- On the global commodities markets, the oil prices increased due to optimism over economic recovery. US GDP data further stoked this optimism resulting in an increase in oil demand. The Crude Oil WTI futures increased by 4.12% from the previous month of March. Also, the ICE Brent Crude Oil increased in value by 3.24%. Gold futures gained by 2.1% as gold prices increased due to declines in U.S. Treasury yields at the middle of the month which drove up demand for dollar-denominated gold.

Get future reports

Please provide your details below to get future reports: