Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves stood at USD 7,045 million (3.95 months of import cover). This falls below CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at KES 122.28, KES 127.33 and KES 148.03 respectively. The observed depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 8.08% | 0.20% |

| Euro | -0.59% | 0.81% |

| Sterling Pound | -2.83% | 2.21% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate rising from 4.37% to 4.90%, as tax remittances more than offset government payments. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 4.37% | 4.90% |

| Interbank volume (billion) | 28.99 | 26.50 |

| Commercial banks’ excess reserves (billion) | 5.70 | 14.80 |

Fixed Income

T-Bills

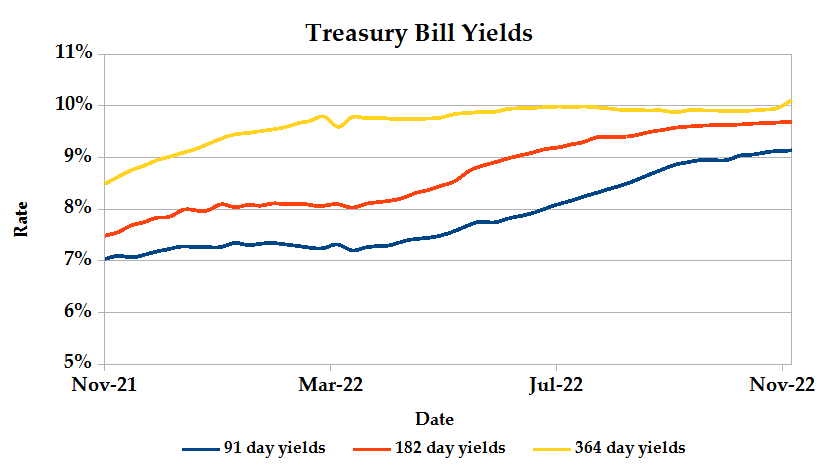

T-Bills remained over-subscribed during the week, with the overall subscription rate slowing to 113.37% from 170.84% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 316.83% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 68.47% and 76.88% respectively. The acceptance rate picked up 7.17% to close the week at 78.64%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover decreased by 8.45% from KES 14.50B in the previous week to KES 13.27B. Total bond deals decreased by 15.27% from 753 in the previous week to 638.

In the primary bond market, CBK reopened two bonds; FXD1/2008/20 and FXD1/2022/25 with effective tenors of 5.6 and 24.9 years and coupon rates of 13.75% and 14.19% respectively, seeking to raise KES 40.0 billion for budgetary support. Additionally, a new 6-year amortized infrastructure bond has been issued; IFB1/2022/6 seeking KES 87.8 billion, with the sale closing on 30th November. The switch bond’s coupon rate is set to be market determined and offers existing holders of T-bill issues 2494/91, 2454/182, 2380/364 and T-bond issue FXD1/2021/2 a chance to roll over their investment into a tax-free issue as well as amped up returns.

Results of the tap sale on issue IFB1/2022/14 were released, recording an anticipated oversubscription with total bids received amounting KES 19.14 billion against a target KES 5.0 billion.

Eurobonds

In the international market, yields on Kenya’s Eurobonds rose by an average 0.43% compared to the previous week, declined 2.92% month to date and increased 4.79% year to date. The yields on the 10-year Eurobond for Ghana increased while that of Angola declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 8.43% | -2.87% | 1.38% |

| 2018 10-Year Issue | 4.63% | -3.28% | 0.25% |

| 2018 30-Year Issue | 2.92% | -2.19% | 0.11% |

| 2019 7-Year Issue | 5.41% | -3.35% | 0.54% |

| 2019 12-Year Issue | 4.07% | -3.24% | 0.18% |

| 2021 12-Year Issue | 3.25% | -2.60% | 0.12% |

Equities

NASI, NSE 20 and NSE 25 lost 1.35%, 0.77% and 0.73% respectively compared to the previous week bringing the year to date performance to -23.83%, -13.70% and -17.29% respectively. Market capitalization declined by 1.35% from the previous week to close at KES 1.98 trillion recording a year to date drop of 23.81%. The performance was driven by losses recorded by large-cap stocks such as KCB, Safaricom and Equity of 3.09%, 2.38% and 1.82% respectively. The losses were however boosted by gains recorded by Co-operative and Standard Chartered of 3.75% and 3.06% respectively.

The Banking sector had shares worth KES 725M transacted which accounted for 50.41% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 332M transacted which represented 23.07% and Safaricom, with shares worth KES 314M transacted represented 21.83% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Olympia | 63.16% | 11.51% |

| Unga | 15.01% | 9.66% |

| Sasini | 19.52% | 7.97% |

| NCBA | 29.08% | 7.35% |

| Jubilee | -36.86% | 6.52% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| NBV | -41.55% | -13.77% |

| Standard Group | -26.94% | -9.59% |

| Express | -26.83% | -8.54% |

| TP Serena | -16.39% | -7.94% |

| Williamson Tea | 6.92% | -7.33% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.38 | 1.48 | 6.83% |

| Derivatives Contracts | 30 | 20 | -33.33% |

| I-REIT Turnover | 0.12 | 0.27 | 121.38% |

| I-REIT Deals | 28 | 46 | 64.29% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -16.06% | 1.53% |

| Dow Jones Industrial Average (DJI) | -6.12% | 1.78% |

| FTSE 100 (FTSE) | -0.25% | 1.37% |

| STOXX Europe 600 | -10.05% | 1.71% |

| Shanghai Composite (SSEC) | -14.61% | 0.14% |

| MSCI Emerging Markets | -23.71% | -0.21% |

| MSCI World Index | -16.59% | 1.68% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -26.27% | 0.95% |

| JSE All Share | -0.41% | 0.79% |

| NSE All Share (NGSE) | 10.52% | 6.88% |

| DSEI (Tanzania) | -1.49% | -0.05% |

| ALSIUG (Uganda) | -14.20% | -1.13% |

US indices edged higher compared to the previous week, boosted by the confirmation of several Fed officials that the pace of rate hikes could soon ease as well as retailers’ hope of a strong sales season. Consumer staples, utilities and healthcare sectors led the gains while tech and consumer discretionary lagged.

European stocks recorded week on week gains, with the STOXX 600 retail index on its sixth straight weekly gains on hopes of slowing rate hikes. Gains were offset by real estate stocks, which slid 0.9% after a survey by Aviva indicated that the demand for rental homes in Britain rose in October 2022 as first time home buyers put off purchases, citing high cost of living which makes mortgage unaffordable.

Asia Pacific stocks ended the week slightly positive with South east markets such as Philippine and Malaysia recording the best performance backed by easing political tensions. However, the bourses underperformed relative to their regional peers, reflecting investors fears of renewed lockdown measures in China and Covid-related worker unrest that affected production.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 4.65% and 4.84% lower at $76.48 and $83.63 respectively. Gold futures prices settled 0.15% higher at $1,754.00.

Week’s Highlights

- The Monetary Policy Committee (MPC) met during the week and decided to raise the Central Bank Rate (CBR) from 8.25% to 8.75%. This is on the back of sustained increase in domestic and global inflation, weakened global outlook as a result of tightened monetary polices across major economies as well as elevated global risks and geopolitical tensions, whose effects have rippled into the country.

- Kenya’s foreign exchange reserves fell below their minimum statutory limit, with the last slip being in October 2015. Speaking at the MPC press release, CBK Governor assured that the reserves are expecting a boost from project loans, with IMF expected to release KES 52.83 billion in December under the current 38-month budgetary support programme. Treasury’s borrowing plan also stipulates an additional KES 57.31 billion expected from bilateral and multilateral lenders.

- High Court has barred implementation of the Retirement Benefits (Mortgage Loans) (Amendment) Regulations, 2020 which would allow pension scheme members access up to 40% of their benefits for home purchase. The ruling was on the grounds that the amendment process was flawed because Parliament did not seek public participation. This stifles the progress the amendment would have made on boosting home ownership and filling the housing gap.

- The Capital Markets (Amendment) Bill, 2022 has been raised in Parliament seeking to introduce taxation of crypto exchanges and digital wallets, to impose similar excise duty transaction taxes (20%) as those charged on bank transactions. The move brings the sector closer to regulation, with the amendment set to define digital assets as securities, placing them under CMA oversight. The United Nations reported that the country’s exposure to cryptocurrencies is the highest in Africa, necessitating a need for monitoring and regulation.

- CMA and NSE have given Hisa Technologies and Faida Investment Bank the green light to introduce fractional investing of Kenyan stocks and government bonds, an extension of the existing offer on fractional investing in US stock portions and ETFs. The move is set to supported by a model that allows investors purchase less than a whole share of a stock, with the dividends earned as a proportion of the shares held. This is in line with the government’s plan to improve investor participation and broaden access to capital markets.

- S&P Global reported a contraction in business activity across the US private sector for the fifth consecutive month in November. The Composite PMI Output Index fell to 46.3 from 48.2 in October, with the slump attributed to the rising cost of living, aggressive Fed rate hikes that have raised borrowing costs and economic uncertainty that has weighed on demand in both domestic and export markets. Manufacturers and service providers however expressed greater confidence in output expectations, supply chain stability and higher client demand supported by new product launches.

Get future reports

Please provide your details below to get future reports: