Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,346 million (4.19 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover. However, it does not meet EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar and the Euro but gained against the Sterling Pound to exchange at Ksh 120.31, Ksh 120.10 and Ksh 138.75 respectively. The observed overall depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 6.34% | 0.16% |

| Euro | -6.24% | 0.07% |

| Sterling Pound | -8.92% | -0.22% |

Liquidity

Liquidity in the money markets increased, partly reflecting government payments which offset tax remittances . Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 4.9% | 4.16% |

| Interbank volume (billion) | 16.9 | 13.1 |

| Commercial banks’ excess reserves (billion) | 40.1 | 42.8 |

Fixed Income

T-Bills

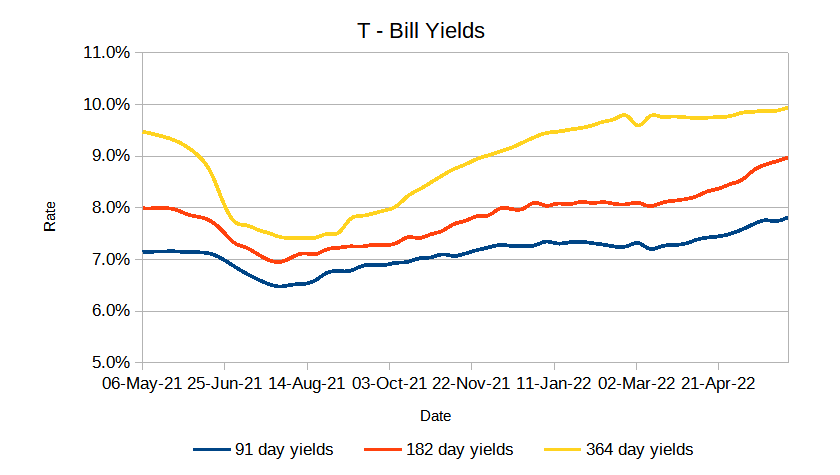

T-Bills were over-subscribed during the week with an increase in the overall subscription rate from 128.75% recorded in the previous week to 152.99%. The 91-day T-Bill got the highest subscription rate at 675.4% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 62.3% and 34.8% respectively. The acceptance rate increased by 7.7% to close the week at 76.12%.

T-Bonds

The bonds market had a lower demand for the week’s bond offers. Bonds turnover decreased by 53.58% from 4.6B in the previous week to 2.1B. Total bond deals decreased by 5.19% from 154 in the previous week to 146.

Eurobonds

In the international market, the yields on the 10-year Eurobonds for Angola and Ghana decreased. Yields on Kenya’s Eurobonds generally decreased by 1.03% compared to the previous week, -1.9% and 6.172% month to date and year to date respectively. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 8.77% | -1.58% | 0.10% |

| 2018 10-Year Issue | 6.67% | -2.17% | 0.13% |

| 2018 30-Year Issue | 3.71% | -1.61% | 0.17% |

| 2019 7-Year Issue | 7.73% | -2.74% | 0.14% |

| 2019 12-Year Issue | 5.77% | -1.43% | 0.12% |

| 2021 12-Year Issue | 4.38% | -1.87% | 0.23% |

Equities

NASI, NSE 20 and NSE 25 increased by 2.63%, 1.37% and 2.09% compared to last week bringing the year to date performance to -15.24%, -6.62% and -11.15% respectively. The market capitalization increased by 2.64% from the previous week to close at 2.207 trillion recording a year to date decline of -15.19%. The performance was driven by gains recorded by large-cap stocks. Top gains were recorded in Safaricom plc, KCB group, Standard Chartered and Co-operative Bank which increased by 6.60% , 4.65%, 3.11% and 2.43% respectively.

The Banking sector had shares worth Ksh 736M transacted which accounted for 45.54% of the week’s traded value, Manufacturing & Allied sector had shares worth Ksh 100M transacted which represented 6.21% and Safaricom, with shares worth Kshs 677M transacted represented 41.89% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Uchumi | 17.39% | 12.50% |

| NCBA | 30.45% | 9.27% |

| Standard Group | 5.54% | 7.52% |

| Kenya Power | -7.47% | 7.38% |

| Olympia | 46.32% | 7.30% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| UNGA | 11.03% | -10.79% |

| Car & General | -26.47% | -9.89% |

| EA portland | 17.54% | -9.05% |

| Kakuzi | -4.42% | -7.77% |

| BK Group | 7.18% | -7.72% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.01 | 0.43 | -57.46% |

| Derivatives Contracts | 6 | 6 | 0.00% |

| I-REIT Turnover | 0 | 0.0022 | 100% |

| I-REIT Deals | 0 | 3 | 100% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -15.20% | 3.65% |

| Dow Jones Industrial Average (DJI) | -12.12% | 2.66% |

| FTSE 100 (FTSE) | -2.05% | 0.96% |

| STOXX Europe 600 | -14.21% | 1.06% |

| Shanghai Composite (SSEC) | -10.91% | 2.37% |

| MSCI Emerging Markets | -21.34% | -0.18% |

| MSCI World Index | -19.63% | -2.90% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -22.93% | -0.05% |

| JSE All Share | -7.31% | 2.09% |

| NSE All Share (NGSE) | 15.50% | -0.70% |

| DSEI (Tanzania) | 1.16% | 0.77% |

| ALSIUG (Uganda) | -8.60% | 1.81% |

US stocks closed the week higher as gains in the Oil and Gas, Technology and Basic Materials sectors led shares higher. Major indexes recorded their first gains in weeks as investors went on a buying spree, shrugging off concerns about the economic outlook. The gains followed a sharp sell-off that begun in mid-August, triggered by concerns about the impact of tighter monetary policies and signs of an economic slowdown in Europe and China.

European stocks closed the week higher as investors digested the European Central Bank’s Jumbo rate hike ahead of a key EU meeting to discuss plans to tackle the region’s energy crisis. The energy ministers are set to meet to discuss the 27-nation bloc’s response to the energy crisis including potentially agreeing on the imposition of a price cap on gas imported from Russia with the soaring prices threatening to push some of the European countries heavily dependent on supplies from Russia.

Asia Pacific stocks closed the week higher tracking an extended recovery as the Dollar and the Treasury yields came off recent highs. Beijing is to increase its spending in the third quarter as Chinese economic growth slowed to a crawl this year due to continued COVID-19 related lockdowns. Despite the week’s gains, most Asian markets are nursing steep losses as rising interest rates in the United States pressured most global markets.

On the global commodities markets, Crude Oil WTI closed the week lower by 0.9% and the ICE Brent Crude decreased by 0.89%. Gold futures prices increased by 0.35% to settle at $1,728.6.

Week’s Highlights

- Markets gained Ksh 42.1 billion in the highest daily gain at the Nairobi Securities Exchange (NSE) as markets welcomed the Supreme Court ruling upholding the presidential results of the just concluded general election. Market capitalisation jumped to Ksh 2.192 trillion from Ksh 2.15 trillion.

- Tea prices rose at the weekly tea auction to hit $2.26 per kilogram with 10.7 million kilograms offered for sale however a decrease from the 12.3 million kilograms offered in the previous sale. This was not the case for coffee as prices dropped to a three-month low reflecting lower demand due to biting inflation in key markets.

- Tanzania froze the issuance of maize export permits for Kenyan traders, a move that is likely to drive the price of the commodity up just 3 months after it increased the cost of export permits by 93% from the previous Ksh 27,000 per truck to Ksh 52,000. This has left processors pushing for stocks that are available locally and a few imports coming from Zambia making it the only key source market for the produce to bridge the local deficit.

- Kenya’s Forex Reserves fell to a 5-year low on the weakening shilling to Ksh 884 billion from Ksh 912 billion the previous week with diaspora remittances, the leading contributor to Forex Reserves dropped for six consecutive months to July. Foreign exchange reserves have sustained a downward trend in the past weeks as the central bank uses part of its stockpile to stabilize the shilling against falling to a level that may disrupt the financial markets.

- Europe’s gas prices rocketed as much as 30% after Russia shut down its main gas supply stocking fear about shortages and gas rationing this winter. Europe has accused Russia of weaponising energy supplies in retaliation for western sanctions imposed on Moscow over its invasion of Ukraine. Russian gas being supplied via Ukraine also reduced leaving the European union to find alternative supplies for gas.

- Egypt’s inflation rose to 14.6% in August with Food and Beverage which make up the larger component jumped to 23.1% . This is even after Egypt’s Monetary committee maintained the deposit rate at 11.25% and the lending rate at 12.25%. Sri Lanka’s inflation hit 64.3% in August with transport and food prices increasing to 148.6% and 93.7% respectively. Sri Lanka is facing its worst economic crisis after running out of foreign exchange reserves to finance even its most essential imports such as food, fuel and medicine.

Get future reports

Please provide your details below to get future reports: