MONTH’S HIGHLIGHTS

- The Treasury will borrow up to KSh41.8 billion from the dollar reserves the Central Bank of Kenya (CBK) received from the International Monetary Fund (IMF) in August. It is eyeing the loan from CBK due to new expenditure requirements in the second half of the fiscal year.

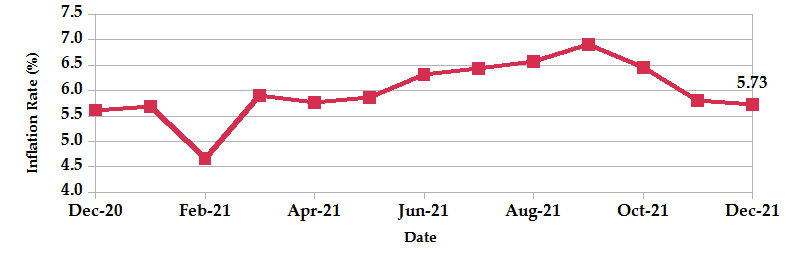

- Kenya recorded an inflation rate of 5.7% for the month of December, following lower food and fuel prices. This is a drop in November’s 5.8%, largely tamed by a government effort to subsidize fuel prices for the month. There are concerns about the weakening shilling and rising oil prices, which could pump up inflation should the government cut fuel subsidies that have retained fuel prices despite increases in transport costs.

- New Year expectations from various captains of industry have been mixed though key players are unanimous that 2021 has been a bumpy ride in the face of challenges posed by the Covid-19 pandemic. There is a cheerful optimism about 2022 slightly dampened by 2022 general election jitters.

- The rapidly growing debt portfolio and growing public outcry over continued borrowing could threaten the pace of infrastructure development and dent investor confidence. The entire pension industry boasts over Sh1.319 trillion in assets under management which comprises up to 13.3% of the GDP as of June 2021, according to the CBK.

- US stocks were mixed on the last trading day of 2021, but the major indexes closed out one of their best years on record. As the new year begins, investors are still concerned about the impact of the omicron variant on the global recovery.

- The International Monetary Fund (IMF) projects the savings rate will continue to gradually improve over the next six years to hit 13.2% in 2026. IMF sees government savings improving from the current negative 2.9% to a positive 6% by 2026. The increase will be supported by the gradual recovery of the economy.

- Mobile banking usage increased to 34.4% in 2021 from 25.3% in 2019, as more people used technology to transact during the Covid-19 period according to the latest FinAccess Household Survey Report 2021.

- Treasury spent KSh36.48 billion on retirees in Q3 2021, reflecting a 78.5% jump from KSh20.44 billion a year earlier. The rise highlights Kenya’s growing pension burden due to an ever-increasing number of retirees from the Public Service.

- Crude oil futures rose on easing COVID-19 concerns and as the ongoing optimism from the Santa Claus rally amid thin trading volumes. This really is because markets tend to rise over a stretch of time right before and after the calendar flips to the new year. This could be attributable to optimism over a coming new year, holiday spending, traders on vacation or institutions squaring up their books.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves increased by 0.92% to stand at USD 8.82 billion(5.39 months of import cover). This meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

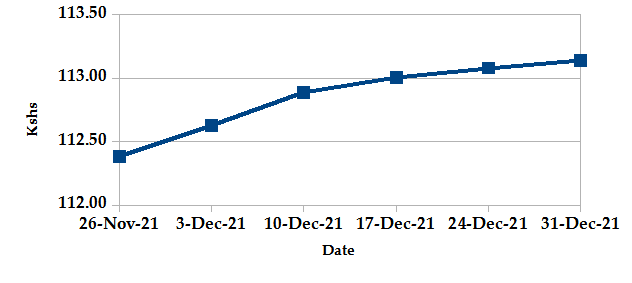

The Kenyan Shilling depreciated against the USD by 0.58%, exchanging at Kshs 113.14 at the end of the month up from Kshs 112.49 in the previous month. The depreciation is due to increased dollar demand from oil and energy importers who had to increase the amounts they pay for oil imports hence depleting the dollar supply in the market.

USD Vs KSHS

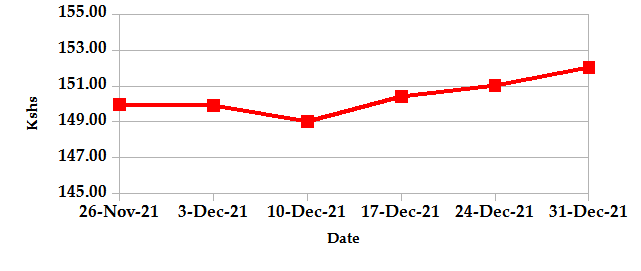

STERLING POUND Vs KSHS

Inflation

The overall year-on-year inflation decreased to 5.73% in the month of December down from a revised figure of 5.80% in November. The decrease is attributable to lower food and fuel prices. there are concerns about the weakening shilling and rising oil prices, which could pump up inflation should the government cut fuel subsidies that have retained fuel prices despite increases in transport costs.

INFLATION EVOLUTION

Liquidity

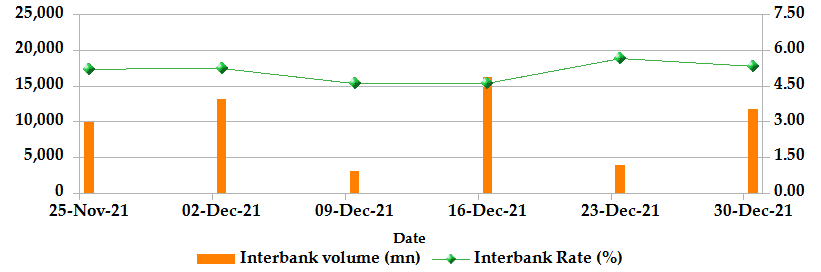

During the month, liquidity decreased as a result of tax receipts which partly offset government payments. The inter-bank rate increased to 4.95% up from 4.90%. The volume of inter-bank transactions increased from Kshs 5.35 billion to Kshs 13 billion. Commercial banks’ excess reserves decreased to Kshs 10.50 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

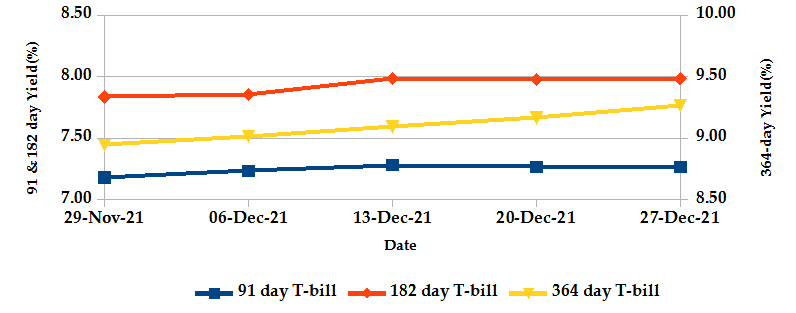

T-Bills

The T-bills recorded an overall subscription rate of 62.0% at the end of month of December, compared to 79.7% recorded in the previous month. The under-subscription is partly attributable to low market liquidity. The performance of the 91-day, 182-day and 364-day papers stands at 101.7%, 46.0% and 62.1% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 2.4%, 5.7% and 7.3% respectively to 7.27%, 8.10% and 9.37%.

T-BILLS

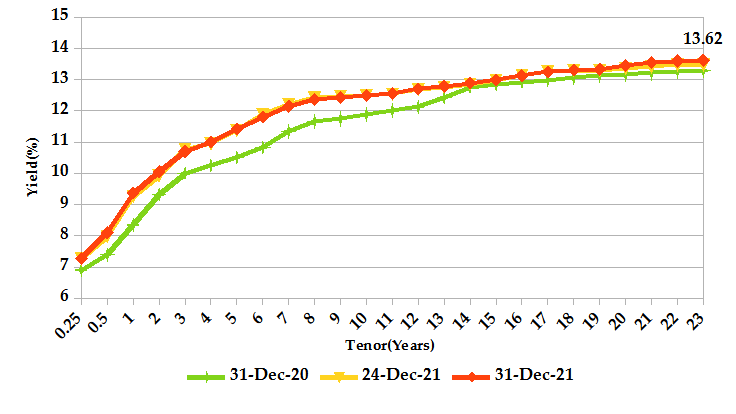

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 5.70 billion from 197 bond deals. This represents a monthly decrease of 58.0% and 69.0% respectively. The yields on government securities in the secondary market remained relatively stable during the month of December.

In the international market, yields on Kenya’s Eurobonds declined marginally by an average of 11.1 basis points.

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 58 contracts having a turnover of Kshs 31.6 million which was an increase from 178 contracts having a turnover of only Kshs 19.0 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.5 million with 206 deals which was a decrease from Kshs 1.6 million with 175 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 9.8 million with 1 deal which was a decrease from Kshs 11.1 million with 4 deals recorded over the last month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 0.85% | 4.36% |

| STOXX Europe 600 | 1.10% | 5.37% |

| Shanghai Composite (SSEC) | 0.60% | 2.13% |

| MSCI Emerging Market Index | 0.94% | 1.62% |

| MSCI World Index | 0.78% | 4.19% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 1.77% | 2.25% |

| JSE All Share | 3.12% | 4.67% |

| NSE All Share (NGSE) | 1.07% | -1.23% |

| DSEI (Tanzania) | -0.35% | 2.72% |

| ALSIUG (Uganda) | 0.97% | -0.18% |

- During the month, major global markets have proven resilient in the face of pandemic-related challenges, and many expect the global economy will still expand at a well-above-trend pace. In the USA, the S&P 500 and Dow Jones indices gained by 4.36% and 5.38% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 appreciated by 5.37% and 4.61% respectively. As far as Covid is concerned, for now, market participants remain willing to add to their risk exposures, and perhaps push equity indices to new highs, as several nations around the globe held off from imposing fresh lock-downs, despite record infections due to rising infection rates from the Omicron variant.

- On a regional front, markets had mixed performance. The FTSE ASEA Pan African index, representing the overall African markets, gained by 2.25% from the month of November. South Africa’s JSE All Share went up by 4.67%, Nigeria’s All Share Index declined by 1.23% and Tanzania’s DSEI increased by 2.72%. However, Uganda’s All Share Index declined by 0.18%. There is significant uncertainty in Africa due to the risk from new Covid-19 variants, amid very low vaccination rates and governments’ limited fiscal space.

- On the global commodities markets, the oil futures indices rose on easing Covid-19 concerns and as the ongoing optimism from the Santa Claus rally amid thin trading volumes. This could be attributable to optimism over a coming new year, holiday spending, traders on vacation or institutions squaring up their books. The Crude Oil WTI futures increased by 13.64% from the previous month of November and the ICE Brent Crude Oil increased in value by 10.22%.

YIELD CURVE

EQUITIES

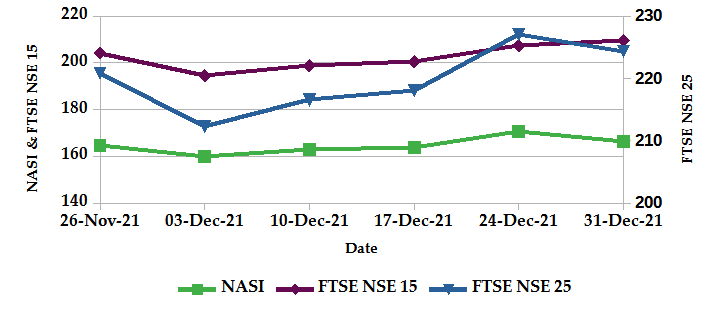

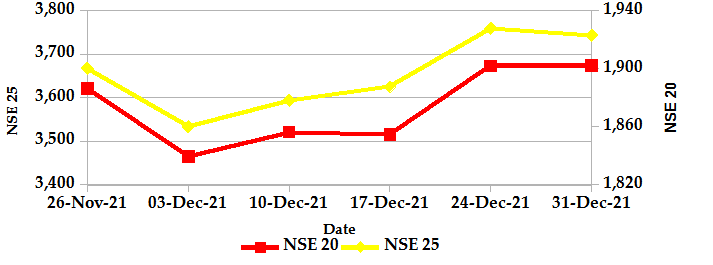

During the month of December, the market capitalization rose by 1.57% to Kshs 2.59 trillion. However, total shares traded and equity turnover plunged by 87.0% and 88.5% respectively to 22.1 million shares and Kshs 685.7 million. NASI, NSE 20 and NSE 25 gained by 1.6%, 1.7% and 3.0% on a monthly basis. On a weekly basis, the NASI and NSE 25 declined by 2.4% and 0.4% respectively while NSE 20 gained by 0.03%. The gain in NASI is a result of an appreciation of large-cap stocks such as EABL, Equity Group, ABSA and Co-operative Bank.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

Get future reports

Please provide your details below to get future reports: