MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) held a meeting on September 28th 2021. The Central Bank Rate (CBR) remained unchanged at 7.00% for the eleventh time in a row. Inflation pressures are expected to be elevated in the near term, mainly driven by increases in fuel and food prices. There is continued global economic recovery due to the rollout of vaccines and the easing of COVID-19 containment measures. Leading economic indicators also point to a strong GDP recovery. The number of non-performing loans declined while growth in private sector credit increased to 7.0% in August from 6.1% in July.

- The Central Bank of Kenya has projected the economy to grow by 6.1% this year and 5.6% in 2022, backed by recovery in manufacturing, trade and hospitality sectors, and despite expected decline in agriculture production. Economic indicators around manufacturing, trade, accommodation and power consumption are pointing to improved economic performance. Rising global crude oil prices and supply constraints have raised the cost of raw materials for local factories and dry weather conditions will keep the cost of living measure high.

- According to a report by the African Development Bank(AFDB), Egypt, Nigeria, Kenya and South Africa were mentioned as the top African countries for investment in Africa.

- The high court has halted plans by KRA to increase excise duty by 4.97% on at least 31 goods in line with average annual inflation as of October, arguing that it will pile pressure on the cost of living. This comes after the high court stopped KRA from collecting a minimum tax of 1% of business sales revenue, even when it reports losses.

- Foreign investors have pulled out Kshs 843 million from the NSE after selling Safaricom and EABL shares, thus weighing down the share prices of the two stocks and the market capitalization of the bourse. Investors are now looking forward to the actions of the US Federal Reserve on tapering down of its asset (bonds) purchase program, which will raise rates on US securities and draw funds back into that market.

- More than half of stock prices at the Nairobi Securities Exchange (NSE) are yet to rebound to pre-Covid-19 levels amid the full recovery of the bourse and economic revival from the pandemic-induced slump 31 out of the 58 actively trading counters are trading below their closing price as at March 12, 2020, when the first Covid-19 case was reported, pulling down the NASI index to a 20-year low. Value investors have concentrated on stocks with good earnings potential, mainly Safaricom and banks.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves increased by 5.02% to stand at USD 9.44 billion(5.77 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

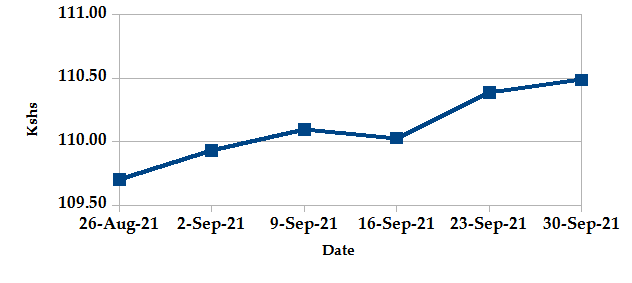

Currency

The Kenyan Shilling depreciated against the USD by 0.56%, exchanging at Kshs 110.49 at the end of the month up from Kshs 109.87 in the previous month. The depreciation is due to increased import activities coupled with increased dollar demand across various sectors including energy while there is low inflows from export activities.

USD Vs KSHS

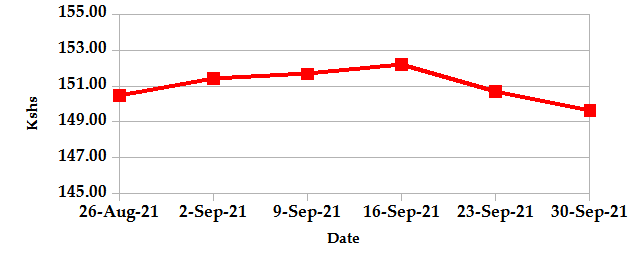

STERLING POUND Vs KSHS

Inflation

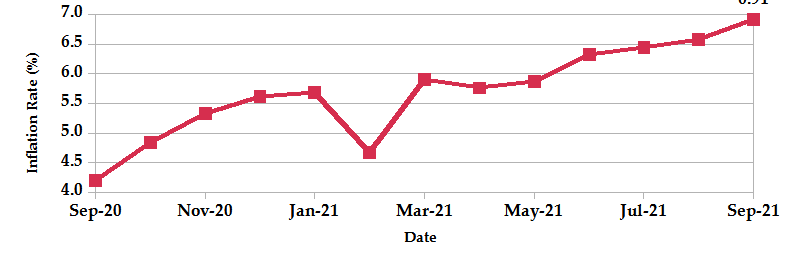

The overall year-on-year inflation increased to 6.91% in the month of September up from a revised figure of 6.57% in August. The increase is attributable to an increase in Food and Non-Alcoholic Drinks Index by 10.63%, Transport by 9.21% and Housing, Water, Electricity, Gas and Other Fuels Index by 6.08%.

INFLATION EVOLUTION

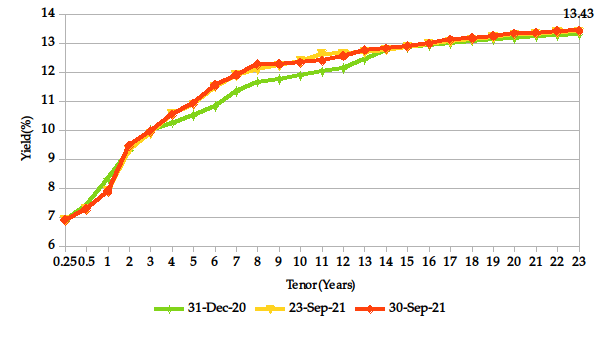

YIELD CURVE

EQUITIES

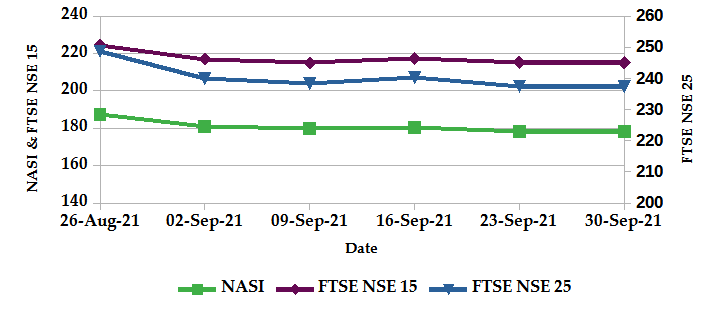

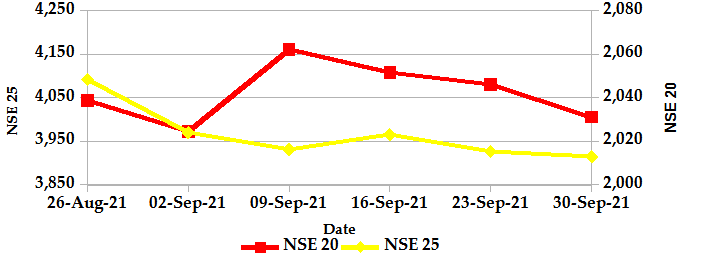

During the month of September, the market capitalization declined by 2.21% to Kshs 2.78 trillion. In addition, total shares traded and equity turnover plunged by 20.0% and 44.1% respectively to 14.9 million shares and Kshs 443.8 million. NASI and NSE 25 declined by 2.2% and 2.6% in that order, while NSE 20 gained by 0.51% on a monthly basis. On a weekly basis, the NASI gained by 0.28% while NSE20 and NSE 25 declined by 0.42% and 0.10% respectively. The gain in NASI is a result of an appreciation of large-cap stocks such as Safaricom, Co-operative Bank and BAT which gained by 3.3%, 1.5% and 1.1% respectively.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

Liquidity

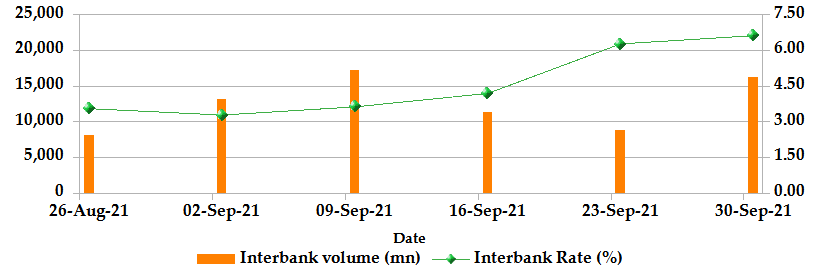

During the month, liquidity tightened due to the build-up of bank balances ahead of the quarter-end reporting as well as anticipatory quarterly tax remittances. The inter-bank rate increased to 6.61% up from 3.36%. The volume of inter-bank transactions increased from Kshs 12.46 billion to Kshs 16.15 billion. Commercial banks’ excess reserves decreased to Kshs 10.60 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

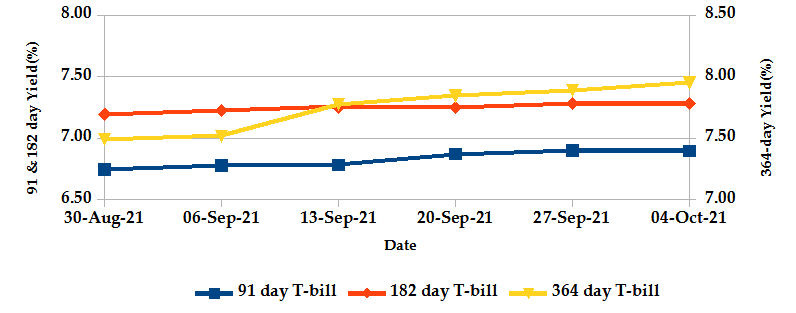

The T-bills recorded an overall subscription rate of 57.95% at the end of the month of September, compared to 71.26% recorded in the previous month. The under-subscription is partly attributable to investor shift to the bond market. The performance of the 91-day, 182-day and 364-day papers stand at 97.9%, 60.8% and 39.2% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 2.28%, 1.21% and 6.10% respectively to 6.90%, 7.28% and 7.95%.

T-BILLS

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 114.7 billion from 2,586 bond deals. This represents a monthly increase of 28.9% and 38.2% respectively. The yields on government securities in the secondary market remained relatively stable during the month of September.

In the international market, yields on Kenya’s Eurobonds increased by an average of 11.7 basis points.

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 252 contracts having a turnover of Kshs 21.9 million which was a decrease from 254 contracts having a turnover of Kshs 40.6 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 27.0 million with 210 deals which was an increase from Kshs 11.4 million with 224 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 63.5 million with 2 deals which was an increase from the previous month which recorded no activity.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -3.32% | -4.76% |

| STOXX Europe 600 | -1.83% | -3.40% |

| Shanghai Composite (SSEC) | -1.24% | 0.68% |

| MSCI Emerging Market Index | -0.95% | -4.25% |

| MSCI World Index | -3.12% | -4.29% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 0.58% | 2.19% |

| JSE All Share | 0.38% | -5.20% |

| NSE All Share (NGSE) | 3.23% | 2.55% |

| DSEI (Tanzania) | -1.22% | -2.40% |

| ALSIUG (Uganda) | -0.58% | -4.00% |

- During the month, major global markets declined as concerns that higher inflation, supply shortages and China’s property sector woes would put global economic recovery at risk. Investors in the USA are focusing on Treasury yields as a key factor in determining how stocks will fare the rest of the year. In the USA, the S&P 500 and Dow Jones indices declined by 4.76% and 4.29% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 declined by 3.41% and 0.47% respectively.

- On a regional front, market performance was mixed. The FTSE ASEA Pan African index, representing the overall African markets, gained by 2.19% from the month of August. South Africa’s JSE All Share declined by 5.20% while Nigeria’s All Share Index rose by 2.55%. In addition, Tanzania’s DSEI and Uganda’s All Share Index declined by 2.40% and 4.00%.

- On the global commodities markets, oil was steady ahead of a meeting by OPEC and its allies which may determine whether a recent rally in prices amid supply shocks and a recovery from the Covid-19 pandemic will be sustained. The Crude Oil WTI futures gained by 9.53% from the previous month of August. In addition, the ICE Brent Crude Oil increased in value by 7.58%.

Get future reports

Please provide your details below to get future reports: