Month’s Highlights

- The Central Bank of Kenya published its 2021-2025 vision and strategy document which set the agenda on the future of the country’s digital payments ecosystem. This includes the adoption of technologies that enable the delivery of new open banking services.

- Vodafone has announced the ending of its talks with Saudi Telecom Company (STC) on the US$2.4 billion sales of its 55% shareholding in Vodafone Egypt. The acquisition of Vodafone Egypt by STC will bring Vodafone’s 22-year history in Egypt to an end. Vodafone has been operating in Egypt since 1998 and is the largest mobile operator in Egypt.

- Companies in the NSE are facing difficulties in the economy with this reflected in deteriorating financial performance that has filtered through to their share price performance. Only 10 companies have recorded a share price gain in 2020. A total of 14 firms have issued profit warnings this year, up from nine in 2019. These have included banks, whose bottom line was hit by rising non-performing loans and the waiver of fees related to mobile transfers.

- Safaricom and its partners have signed an agreement to borrow up to KSh55.7 billion from US International Development Finance Corporation to fund expansion into Ethiopia’s telecommunications market. The financial investment in Ethiopia is expected to top the KSh111 billion mark, with the DFC loan deal seen as part of the project’s fundraising efforts.

- Mwalimu National SACCO has fully acquired Spire Bank from Naushad Merali for an undisclosed amount. Interestingly, a Government probe into the Mwalimu National SACCO-ECB transaction has been kept under wraps to this moment.

- NIC Capital Limited has applied to the Capital Markets Authority(CMA) concerning its request to cease operations. This investment bank is associated with the former NIC Bank, which has since merged its operations with the Commercial Bank of Africa (CBA).

- China will overtake the USA to become the world’s biggest economy in 2028, five years earlier than previously estimated by the UK-based Centre for Economics and Business Research in its annual report. The report attributes China’s growing economic muscle to its skillful management of the pandemic, with its strict early lockdown, improving its performance relative to the USA and Europe.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 2.53% to stand at USD 7.75 billion(4.76 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

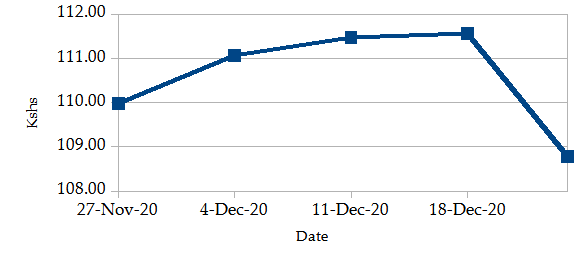

The Kenyan Shilling gained against the USD by 0.74%, exchanging at Kshs 109.17 at the end of the month down from Kshs 109.98 in the previous month. This is attributable to several factors, including a weakening US dollar and CBK interventions.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

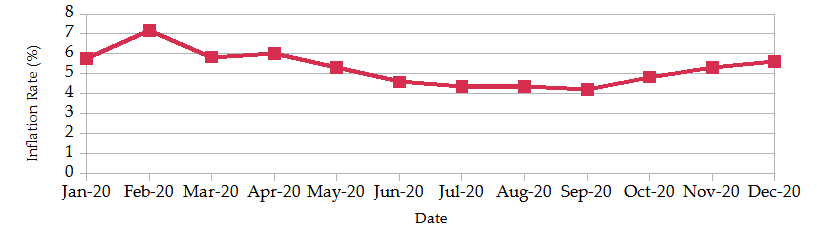

The overall year-on-year inflation increased to 5.62% in the month of December up from a revised figure of 5.33% in November. The increase is attributable to the rise in the prices of essential food items, transport, electricity, water, gas, and other fuels such as kerosene/paraffin, which contributed to a surge in the December cost of living index. Beginning midnight of December 31st, 2020, Kenyans have started paying the new 16% VAT, previously lowered to 14% as part of the Covid-19 relief package.

INFLATION EVOLUTION

Liquidity

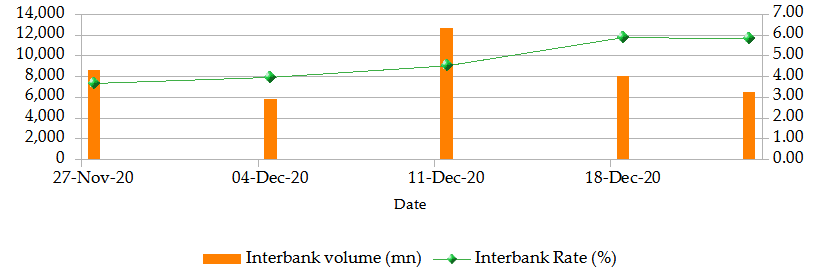

During the month, liquidity decreased as a result of tax remittances more than offsetting government payments. The inter-bank rate increased to 6.08% up from 3.47%. The volume of inter-bank transactions increased to Kshs 16.39 billion from Kshs 13.33 billion. Commercial banks excess reserves increased to Kshs 16.80 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

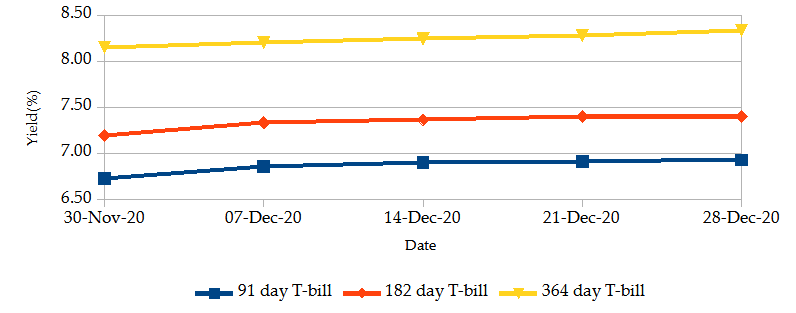

The T-bills recorded an overall subscription rate of 52.60% at the end of the month of December, compared to 93.94% recorded in the previous month. The under-subscription is partly attributable to tightening liquidity in the aftermath of holiday expenditures. The performance of the 91-day, 182-day and 364-day papers stand at 100.6%, 38.4% and 47.6% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 2.62% 2.88% and 2.42% respectively to 6.91%, 7.40% and 8.35%.

T-BILLS

T-Bonds

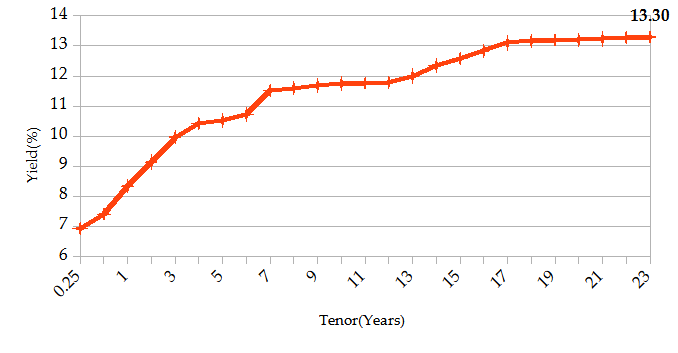

At the end of the month, the T-Bonds registered a turnover of Kshs 56.45 billion from 1,511 bond deals. This represents a monthly increase of 28.60% and 26.37% respectively. The yields on government securities in the secondary market increased during the month of December.

In the international market, yields on Kenya’s Eurobonds declined by an average of 8.9 basis points on a weekly basis.

YIELD CURVE

EQUITIES

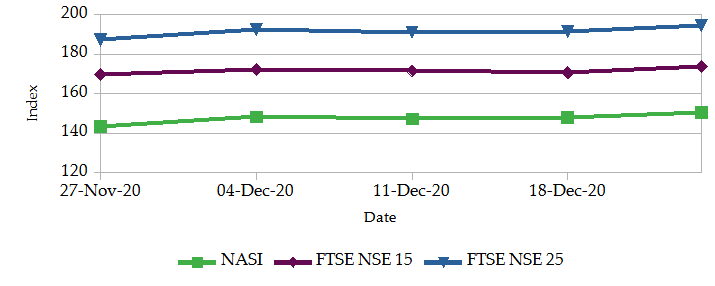

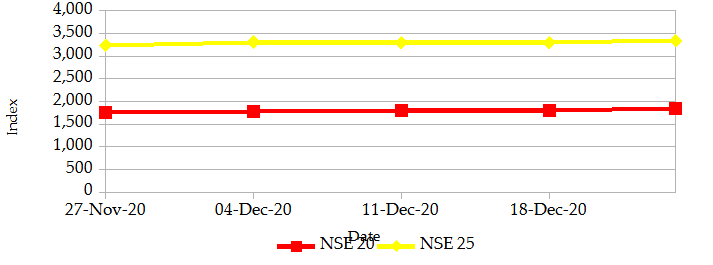

During the month of December, the market capitalization rose by 6.21% to Kshs 2.34 trillion. However, total shares traded and equity turnover declined by 75.10% and 84.68% respectively to 4 million shares and Kshs 86 million. NASI, NSE 20 and NSE 25 gained by 6.2%, 6.3% and 5.3% respectively on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 gained by 1.3%, 1.6% and 2.1% respectively. The gain in NASI is as a result of the appreciation of large-cap stocks such as Safaricom, Co-operative Bank, East Africa Breweries Ltd and ABSA Bank.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25TS

ALTERNATIVE INVESTMENTS

- Mixed-Use Developments recorded average rental yields of 7.1%, 0.3% points higher than the respective single-use retail, commercial office and residential themes in 2020. The relatively better performance by MUDs is attributed to the prime locations, mostly serving the high and growing middle class supported by the concept’s convenience as it incorporates working, shopping and living spaces.

- The derivatives market over the month recorded 91 contracts having a turnover of Kshs 7.6 million which was an increase from 25 contracts having a turnover of Kshs 1.3 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.8 million with 157 deals which was an increase from Kshs 1.2 million with 155 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 6.6 million with 7 deals which was an increase from Kshs 3.3 million with 3 deals recorded over the last month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 1.43% | 3.24% |

| STOXX Europe 600 | 0.77% | 1.47% |

| Shanghai Composite (SSEC) | 2.25% | 1.90% |

| MSCI Emerging Market Index | 2.91% | 4.96% |

| MSCI World Index | 1.16% | 3.41% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 1.34% | 4.19% |

| JSE All Share | 0.47% | 2.56% |

| NSE All Share (NGSE) | 3.79% | 15.44% |

| DSEI (Tanzania) | 0.26% | 0.99% |

| ALSIUG (Uganda) | 1.44% | -0.14% |

- During the month, major global markets gained as the Covid-19 vaccine continues to be distributed. In the USA, the S&P 500 and Dow Jones indices gained by 3.24% and 2.33% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 appreciated by 1.47% and 1.46% respectively.

- On a regional front, most markets were on an upward trend and outperformed the Kenyan stock market apart from the Uganda All Share Index. The FTSE ASEA Pan African index, representing the overall African markets, gained by 4.19% from the month of November. South Africa’s JSE All Share went up by 2.56%, Nigeria’s All-share index rose by 15.44% and Tanzania’s DSEI increased by 0.99%. However, Uganda’s All Share Index declined by 0.14%.

- On the global commodities markets, the oil futures gained with a bigger-than-expected decline in U.S. crude oil inventories and hopes for a U.S. Covid-19 fiscal aid package boosting fuel demand recovery hopes. The Crude Oil WTI futures gained by 6.57% from the previous month of November. The ICE Brent Crude Oil increased in value by 7.51%.

- During the month, U.S. stock markets gained with hopes for a boost to the already-agreed fiscal stimulus package dovetailed with the urge to do some “window-dressing” of year-end balance sheets. This was supported by confidence that the stimulus package would put a floor under household spending for the next few months. The Brexit trade deal should see sentiment towards the FTSE indices recover just as the dividend payout ratio improves, vaccines are rolled out and overseas revenues accelerate.

Get future reports

Please provide your details below to get future reports: