Month’s Highlights

- The Monetary Policy Committee (MPC) met on June 25, 2020, and for the second time retained the base lending rate at 7%. Citing the impact of the continuing global COVID-19 (coronavirus) pandemic, and measures taken by authorities around the world to contain its spread and impact. The Committee noted that there has been strong growth in the first quarter of 2020 despite the restrictions implemented due to the pandemic. The growth was majorly supported by Kenya’s export which improved by 4.1% between January and May 2020. Policy measures adopted in March and April were having the intended effect on the economy, and are still being transmitted. The MPC concluded that the current accommodative monetary policy stance remains appropriate, and therefore decided to retain the Central Bank Rate (CBR) at 7.00%.

- Jamii Bora Shareholders accepted an offer by Co-operative bank to acquire a 90% stake of Jamii Bora at the value of Ksh 1 billion. Jamii Bora bank’s had recorded losses of Ksh 51.3 million in quarter 1 of 2018 and Ksh 96.8 million in quarter 1 of 2017. Initially, Co-op Bank had a discussion to buy a 100% stake in the bank. The number of banks in Kenya will reduce to 38 but Kenya will still remain over-banked compared to countries such as South Africa.

- Equity Group announced to call off plans to buy Atlas Mara after the two parties came into a mutual agreement. Equity had entered into a binding term sheet in 2019 with Atlas Mara to acquire Banque Populaire du Rwanda, African Banking Corporation Zambia Ltd, Africa Banking Corporation Tanzania, and Africa Banking Corporation Mozambique Ltd. The transaction was to be funded by a share swap that would result in Atlas Mara owning 252.2 million shares of Equity Group equivalent to a 6.7% stake.

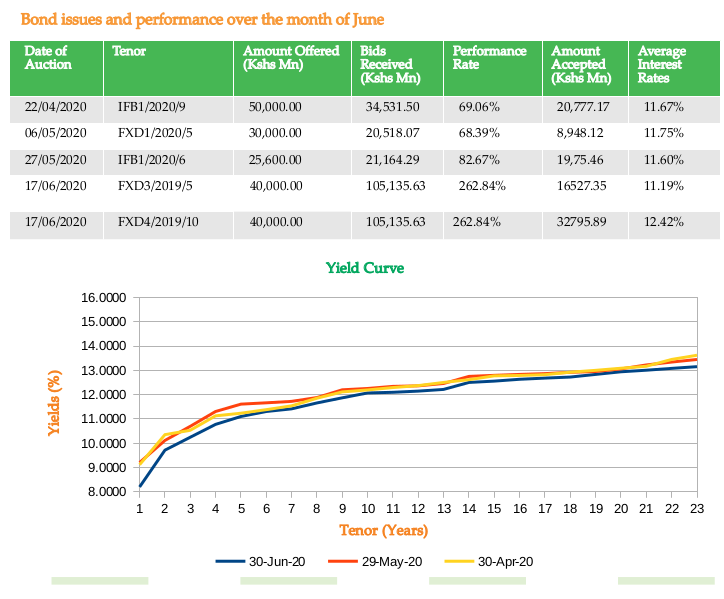

- The Treasury achieved its domestic borrowing target of Ksh 409 billion after taking up Sh 15.7 billion in bonds and bills during June. In the four weekly T-bill auctions in June, investors bid a total of Sh 224 billion from which the central bank accepts Sh 69.1 billion less than a third of bids received. On the month’s Sh 40 billion sales, bids worth Sh 105 billion were received with the government accepting Sh 18.4 billion.

- KQ is projected to lose up to $500M by December in revenue, so far the airline has incurred an estimated $100 million due to the pandemic. KQ is seeking to be allowed to resume flying to mitigate the losses and preserve the airline as a going concern especially after reporting a $130 million full-year loss early June. A Bill to privatize was tabled in parliament on 25th June 2020 that will set the stage for minority buyout and converting shares owned by banks into Treasury bonds.

- South African based African Alliance group ceased operations in its stockbroking unit in Kenya. The company says it will now focus on asset management and treasury business. The group cites declining business at the Nairobi Securities Exchange and the need to capitalize on other market areas as the catalyst for the move. African Alliance will refund cash to clients and investors in the company.

- Kenya’s economy grew by 4.9% in the first quarter of 2020 compared to 5.5% in the first quarter of 2019. Agricultural production boosted output as well as the resilient service sector. Covid-19 effects on the economy will majorly impact the output in the second quarter.

ECONOMIC INDICATORS

Foreign Exchange Reserves

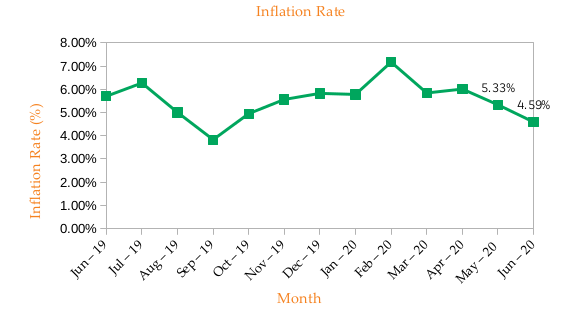

The overall year on year inflation rate decreased to 4.59% in the month of June from 5.33% recorded in May. The decline flows the decrease in the overall CPI rate from 108.60 in May to 108.27 in June. Food and non-alcoholic consumer price index declined by 1.27% due to a decrease in prices while food inflation increased by 8.15%, prices of tomatoes decreased by among other foodstuffs while onions, kales and spinach prices increased by 3.51, 4.67, and 2.61 percent. Housing, water, electricity, gas and other fuel price index also declined by 0.81% mainly due to a decrease in kerosene cost while transport price index increased by 2.08%on account of an increase in petrol prices.

During the month, the CBK’s usable foreign reserves improved by 10.78% to settle at USD 9.23 billion(5.55 months of import cover). This meets the CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

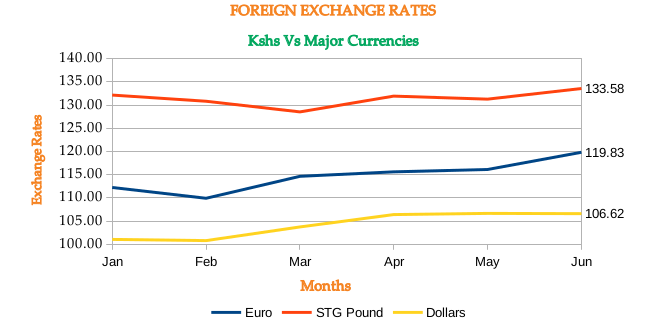

The Kenyan Shilling remained relatively stable against major global currencies. It appreciated by 0.41% against the USD to trade at Kshs 106.51, from Kshs 106.94 registered at the end of May. The gains recorded are due to high levels of forex reserves, an increase in tea and flower exports as destination markets began to open up, and remittances inflows registered in May which stood at Ksh 27.5 billion up from Ksh 22.2 billion in April.

Inflation

The overall year on year inflation rate decreased to 4.59% in the month of June from 5.33% recorded in May. The decline flows the decrease in the overall CPI rate from 108.60 in May to 108.27 in June. Food and non-alcoholic consumer price index declined by 1.27% due to a decrease in prices while food inflation increased by 8.15%, prices of tomatoes decreased by among other foodstuffs while onions, kales and spinach prices increased by 3.51, 4.67, and 2.61 percent. Housing, water, electricity, gas and other fuels price index also declined by 0.81% mainly due to a decrease in kerosene cost while transport price index increased by 2.08%on account of an increase in petrol prices.

Liquidity

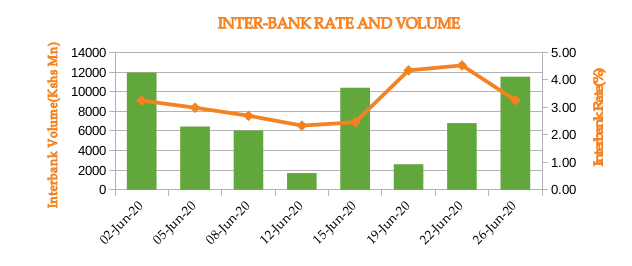

During the month, liquidity improved with the inter-bank rate closing at 3.26% in the month of June down from 3.28% in May. This is mainly as a result of government payments and open market operations that remained active during the month. The commercial bank’s excess reserves stand at Kshs 41.1 bn up from 35.20 bn in May. The volume of inter-bank transactions decreased from Kshs 18.25 bn to Kshs 11.53 bn.

FIXED INCOME

T-Bills

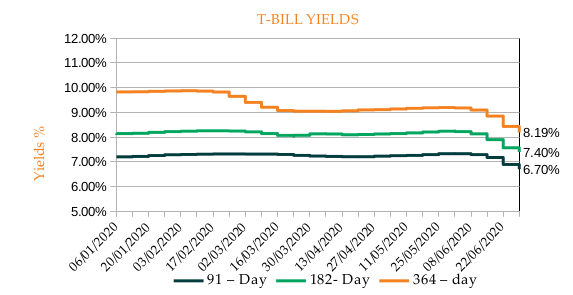

The T-bills recorded an overall subscription rate of 245.63% during the month of May, compared to 103.7% recorded in the previous month. The over-subscription is attributable to high liquidity in the money market. The subscription rates for the 91-day, 182-day, and 364-day paper rose to 412.03%, 140.25%, and 284.44%, respectively, from 81.28%, 58.41% and 154.99% recorded in May. On a monthly basis, the yields on the 91-day, 182-day, and 364-day papers decreased by 8.63% 10.34% and 10.92% points respectively, to settle at 6.7%, 7.4%, and 8.19%. On a weekly basis, the yields also decreased.

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 4.621 bn from 135 bond deals. This represents a monthly increase of 35% and 103.83% respectively. The yields on 4-year, 5-year, 6-year, and 7-year government securities in the secondary market on average declined in the month of June from May. On the other hand, towards the end of the curve, June had reduced yields compared to May. In the international market, yields on Kenya’s Eurobonds slightly declined similar to the 10-year Eurobonds for Angola and Ghana. CBK reopened the 5-year and 10-year bonds which were highly oversubscribed at 262.84%.

EQUITIES

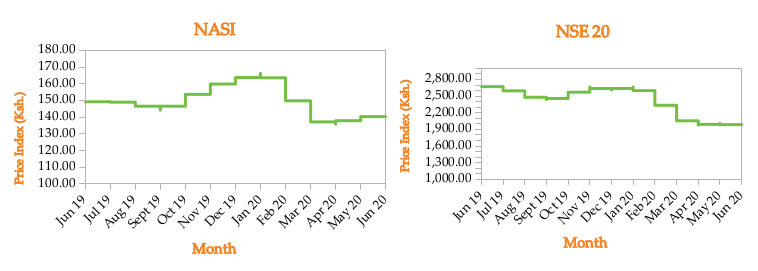

In June, the market capitalization increased by 1.21% to Kshs 2.12 trillion up from Kshs 2.10 trillion in May. Total shares traded and equity turnover rose by 72.42% and 17.01% respectively to 146 million shares and Kshs 2.77 billion. NASI, NSE 20, and NSE 25 surged by 1.21%, 0.21%, and 1.34% on a monthly basis. The rise in turnover despite the share prices decline reflects the sustained selling activity of foreign investors who are now seeking safety in developed markets. The net sales until June were Sh 22.8 billion mainly driven by the five large-cap stock that accounts for Sh 2.1 trillion market capitalization on the course.

ALTERNATIVE INVESTMENTS

During the month of June, the derivatives market recorded a turnover of Kshs 1.45 million. The I-REIT market registered a turnover of Kshs 9.06 million. The ETF market closed the month with a turnover of Kshs 26.277 million. On a weekly basis, the derivatives market recorded increased activity as the turnover rose from Ksh 107, 750 million to Ksh 803, 905 million from last week’s turnover. The I-REIT market also experienced an increase in turnover from Ksh 2.83 million to Ksh 6.85 million while the ETF market recorded an increase from Ksh 4.05 million to Ksh 26 million.

GLOBAL AND REGIONAL MARKETS

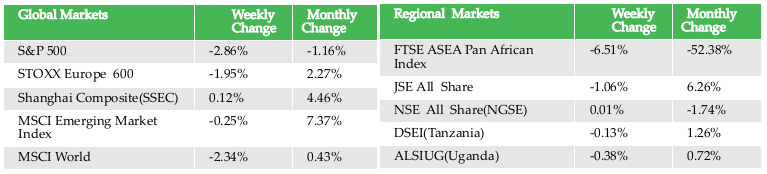

- During the month, major global indices were on the rise except S&P 500 which fell by 1.16% and DJI which declined by 1.45%. The World MSCI Index soared by 0.43% while the MSCI Emerging Markets Index rose marginally by 7.37%. China’s SSEC edged higher by 4.46%. In Europe, the European index, STOXX Europe 600 edged up by 2.27% while UK’S FTSE 1000 climbed up by a margin of 2.45%.

- The US Federal Reserve restricted dividends banks can pay shareholders and required them to suspend repurchases after an analysis showed that some banks could approach minimum capital levels. Banks will only be allowed to pay dividends in line with a formula based on their most recent income.

- On the regional front, the Pan African index FTSE ASEA registered a monthly decline of 52.38% from the previous month of May. South Africa’s JALSH gained by 6.26%, Nigeria’s NGSEINDEX went down by 1.74%, Tanzania’s DSEI improved by 1.26% with Uganda’s ALSIUG rising marginally by 0.72%.

- On the global commodities market, oil futures recovered sharply from losses recorded in the month of May. Crude Oil WTI and ICE Brent Crude oil appreciated by 8.45% and 16.11%, respectively. On a weekly basis, the oil futures decreased by 3.17% and 2.77% respectively. The gold futures prices increased on a weekly and monthly basis by 1.56% and 2.5% respectively.

Get future reports

Please provide your details below to get future reports: