The usable foreign exchange reserves stood at USD 7,131 million (3.80 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling appreciated against the Dollar, the Sterling Pound and the Euro to exchange at KES 160.09, KES 202.00 and KES 172.43 respectively. The observed appreciation against the Dollar is attributed to a lower demand for the Dollar and tight monetary policy.

Currency

YTD Change

W-o-W Change

Dollar

1.97%

-0.30%

Sterling Pound

1.08%

-0.64%

Euro

-0.70%

-0.71%

Liquidity

Liquidity in the money markets increased, with the average inter-bank rate decreasing from 13.26% to 13.14%, as government payments more than offset tax remittances. Open market operations remained active.

Liquidity

Week (previous)

Week (ending)

Interbank rate

13.26%

13.14%

Interbank volume (billion)

14.57

31.83

Commercial banks’ excess reserves (billion)

22.70

16.20

Fixed Income

T-Bills

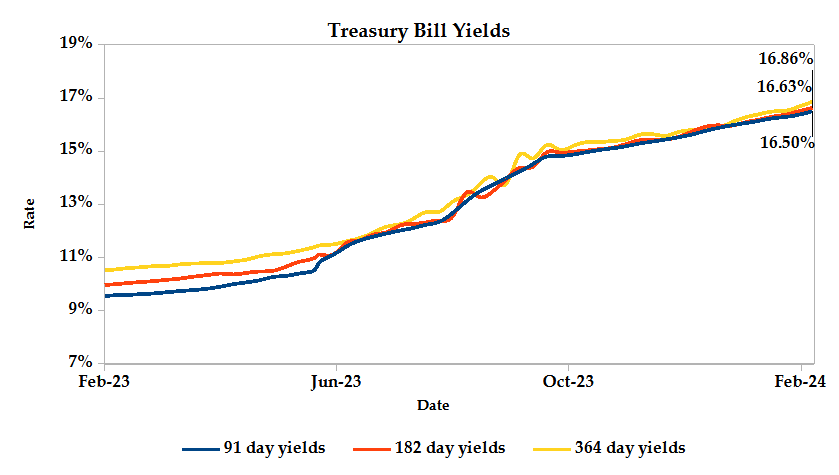

T-Bills remained over-subscribed during the week, with the overall subscription rate increasing to 213.00%, up from 107.50% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 867.62% while the 182-day T-Bill and 364-day T-Bill had subscription rates of 94.47% and 69.68% respectively. The acceptance rate decreased by 4.62% to close the week at 95.38%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 0.60%, from KES 23.27 billion in the previous week to KES 23.41 billion. Total bond deals decreased by 23.06% from 594 in the previous week to 457.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average of 0.67% compared to the previous week, 0.67% month-to-date and 0.13% year-to-date. On the contrary, the yields on the 10-year Eurobonds for Angola and Zambia increased. Below is a summary analysis of performance for individual bonds.

Bond

YTD Change

M-o-M Change

W-o-W Change

2014 10-Year Issue

-3.87%

-4.31%

-4.31%

2018 10-Year Issue

0.65%

0.10%

0.10%

2018 30-Year Issue

0.50%

0.17%

0.17%

2019 7-Year Issue

0.48%

-0.51%

-0.51%

2019 12-Year Issue

0.78%

0.28%

0.28%

2021 13-Year Issue

0.66%

0.23%

0.23%

Equities

NASI, NSE 25 and NSE 10 settled 1.29%, 0.42% and 0.89% lower while NSE 20 settled at 0.26% higher compared to the previous week, bringing the year-to-date performance to -0.86%, 1.18%, 0.79% and 0.51% respectively. Market capitalization lost 1.29% from the previous week to close at KES 1.42 trillion, recording a year-to-date decrease of 0.86%. The performance was driven by losses recorded by large-cap stocks such as Safaricom, KCB and Equity of 3.33%, 2.21% and 1.83% respectively. This was however mitigated by the gains recorded by Stanbic, ABSA and Co-op Bank of 4.55%, 1.69% and 1.67% respectively.

The Banking sector had shares worth KES 540.6M transacted which accounted for 53.87% of the week’s traded value, Manufacturing and Allied sector had shares worth KES 84.2M transacted which represented 8.39% and Safaricom, with shares worth KES 313.7M transacted represented 31.26% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

Top Gainers

YTD Change

W-o-W

Transcentury

-5.77%

8.89%

HF Group

9.86%

7.37%

Scangroup

15.60%

7.23%

Kakuzi

0.00%

5.77%

Jubilee

2.70%

5.41%

Losers

YTD Change

W-o-W

Sasini

0.00%

-8.88%

Home Africa

-17.95%

-8.57%

Umeme

-6.75%

-6.45%

Britam

-8.56%

-6.00%

Fahari I-REIT

-9.84%

-5.96%

Alternative Investments

Losers

Week (previous)

Week (ending)

% Change

Derivatives Turnover (million)

2.52

0.52

-79.26%

Derivatives Contracts

23.00

12.00

-47.83%

I-REIT Turnover (million)

0.12

1.05

768.35%

I-REIT deals

22.00

94.00

327.27%

Global and Regional Markets

Global Markets

YTD Change

W-o-W

S&P 500

5.98%

1.37%

Dow Jones Industrial Average (DJI)

2.54%

0.04%

FTSE 100 (FTSE)

-1.93%

-0.56%

STOXX Europe 600

1.32%

0.19%

Shanghai Composite (SSEC)

-3.25%

4.97%

MSCI Emerging Markets Index

-2.84%

0.74%

MSCI World Index

3.54%

1.04%

Continental Markets

YTD Change

W-o-W

FTSE ASEA Pan African Index

-2.99%

-1.33%

JSE All Share

-3.58%

-1.45%

NSE All Share (NGSE)

34.04%

-2.45%

DSEI (Tanzania)

0.03%

1.44%

ALSIUG (Uganda)

0.57%

1.29%

The US stock market closed the week in the green zone, as investors digested revised inflation data and the Federal Reserve’s monetary policy plans. The Bureau of Labor Statistics (BLS) updated Consumer Price Index (CPI) figures showed a slightly lower-than-expected increase in December, alongside recent Fed comments suggesting a slower pace of interest rate hikes.

The European stock market was volatile during the week, as investors grappled with a deluge of corporate earnings reports, regional inflation data and the potential impact of the upcoming Fed decision.

The Asian stock market closed the week on a positive trend, fueled by a shift in leadership at the market regulator and timely support measures from Beijing ahead of a holiday break.

Week’s Highlights

The Monetary Policy Committee (MPC) of the Central Bank of Kenya increased its benchmark rate by 50 basis points to 13.0% at its meeting on February 6, 2024, following a significant 200 basis point hike in December. This brings borrowing costs to their highest level since October 2012. The decision is a response to the challenge of rising inflation, which has persisted above the government’s 5.0% target range. All components of inflation, including fuel, food and non-food non-fuel, increased in January 2024. The MPC also highlighted ongoing pressure on the exchange rate as a contributing factor. The interest rate hike aims to anchor inflation expectations and guide inflation back towards the target range while addressing exchange rate pressures.

Kenya announced a tender offer to repurchase its $2 billion, 6.88% Eurobond, maturing in June 2024. The offer, open from February 7th to 14th, allows investors to tender their bonds for $1,000 per $1,000 of the principal amount of the accepted notes. Citigroup and Standard Bank act as dealer managers, while Citibank London serves as a tender agent. This initiative aims at managing Kenya’s external debt by smoothing the maturity profile and potentially reducing interest costs. The offer is conditional on the successful issuance of new U.S. dollar-denominated notes, with the maximum tender amount to be determined post-pricing of these new notes. Additionally, participation requires valid tender instructions by the expiration deadline, with a minimum denomination requirement.

The Nairobi Securities Exchange (NSE) is set to revolutionize fixed-income trading in Kenya with the launch of a hybrid market. This innovative platform, approved by the Capital Markets Authority, combines the transparency of on-screen trading with the flexibility of over-the-counter (OTC) deals, offering investors and issuers a wider range of options and potentially intensifying competition within the fixed-income landscape.

Kenya has entered into a memorandum of understanding with Japan, unlocking access to the Japanese Yen market through a $500 million Samurai Bond. This strategic move, announced in February 2024, diversifies Kenya’s debt portfolio and fuels green initiatives through two phases of $250 million each. The funds are earmarked for electric mobility (E-mobility) projects, aligning with Kenya’s environmental goals and accelerating the adoption of sustainable transportation solutions. This initiative not only reduces Kenya’s exposure to US dollar-denominated debt but also positions Kenya as a leader in sustainable development and paves way for a cleaner, more modern transportation sector.

The Stanbic Bank Kenya PMI edged up to 49.8 in January 2024 from 48.8 in December 2023, marking the slowest contraction in five months. While both output and new orders still declined, the pace eased, with some companies reporting improved order books and foreign sales. Additionally, employment saw its first increase since August 2023, albeit primarily temporary workers. However, purchasing activity and inventories continued to fall, highlighting persistent supply chain disruptions. Notably, input cost inflation eased significantly, leading to slower output price growth, while business sentiment regarding future output weakened, reaching an eight-month low.

The Capital Markets Authority (CMA) has granted NCBA Bank license to operate as a Real Estate Investment Trust (REIT) Trustee, unlocking new avenues for Kenyans seeking exposure to the real estate sector. As a licensed trustee, NCBA will hold and manage real estate assets on behalf of REIT investors, joining established players like Kenya Commercial Bank, Co-operative Bank and Housing Finance Bank. This expansion of the REIT ecosystem in Kenya is expected to attract more investors and developers, potentially boosting real estate development and overall economic activity. Additionally, the CMA also granted VCG Asset Management Limited license to operate as a fund manager, bringing the total number of licensed fund managers in Kenya to 41. This development expands investment options and strengthens the financial services sector, offering investors greater choice and diversification opportunities.

China’s consumer prices unexpectedly deflated further in January, dropping by 0.8% year-on-year. This marks the steepest decline in over 14 years and the fourth consecutive month of drops. Food prices led the charge, plunging at a record pace of 5.9%, with all categories seeing reductions. While non-food inflation remained positive, it edged lower to 0.4%. Despite rising costs in specific sectors like clothing and healthcare, the overall trend points towards weakening demand and potential deflationary risks.

January’s PMI data revealed a mixed bag for global economies. The US, with a composite PMI of 52.0, stands out with service sector growth and easing inflation to a 2-year low. This boosted investors’ confidence to a 20-month high, despite contraction in manufacturing. The UK’s Eurozone Composite PMI reached a 6-month high of 47.9, hinting at potential stabilization despite the ongoing decline. New business and employment are steady, but price pressures remain high. China’s Caixin PMI of 52.5 marks its 13th month of expansion, but the pace slows with dampened new orders and export sales. Dr. Wang Zhe of Caixin highlighted ongoing challenges like tepid demand and subdued expectations.

Get future reports

Please provide your details below to get future reports: