Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,814 million (3.60 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar and the Sterling Pound but appreciated against the Euro to exchange at KES 160.35, KES 203.62 and KES 174.47 respectively. The observed depreciation against the Dollar is attributed to a high demand from energy and commodity importers.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | 2.14% | 0.31% |

| Sterling Pound | 1.88% | 0.19% |

| Euro | 0.47% | -0.29% |

Liquidity

Liquidity in the money markets tightened, with the average inter-bank rate increasing from 13.44% to 13.76%, as tax remittances more than offset government payments. Remittance inflows totalled $372.60 million in December 2023, a 4.96% increase from $355.0 million in November 2023 and a 7.86% rise from $345.45 million in December 2022. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 13.44% | 13.75% |

| Interbank volume (billion) | 11.83 | 13.88 |

| Commercial banks’ excess reserves (billion) | 14.60 | 19.60 |

Fixed Income

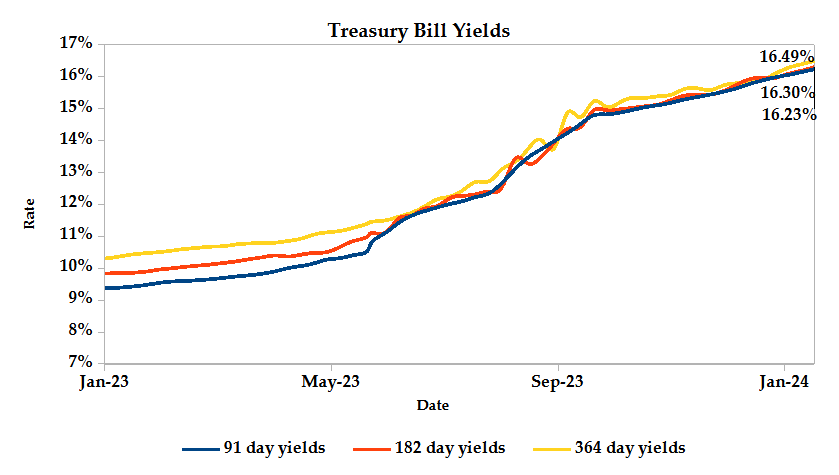

T-Bills

T-Bills remained over-subscribed during the week, with the overall subscription rate decreasing to 146.99%, down from 241.54% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 638.95% while the 182-day T-Bill and 364-day T-Bill had subscription rates of 61.93% and 35.26% respectively. The acceptance rate increased by 22.04% to close the week at 96.77%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 71.98%, from KES 10.09 billion in the previous week to KES 17.36 billion. Total bond deals increased by 40.36% from 389 in the previous week to 546.

In the primary bond market, CBK released auction results for the 3-year bond FXD1/2024/003 and 5-year FXD1/2023/005 which sought to raise KES 15.0 billion through a tap sale. The issues received bids worth KES 11.86 billion, representing a subscription rate of 79.07%. Of these, KES 11.76 billion worth of bids were accepted at a weighted average rate of 18.39% and 18.77% respectively.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average 0.08% compared to the previous week, but increased 0.18% month-to-date and 0.18% year-to-date. The yields on the 10-year Eurobonds for Zambia increased while that of Angola declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 0.14% | 0.14% | -0.36% |

| 2018 10-Year Issue | 0.15% | 0.15% | -0.07% |

| 2018 30-Year Issue | 0.14% | 0.14% | 0.00% |

| 2019 7-Year Issue | 0.39% | 0.39% | -0.04% |

| 2019 12-Year Issue | 0.14% | 0.14% | -0.03% |

| 2021 13-Year Issue | 0.11% | 0.11% | -0.02% |

Equities

NASI, NSE 20, NSE 25 and NSE 10 settled 0.61%, 0.18%, 0.52% and 0.45% higher compared to the previous week, bringing the year-to-date performance to 1.52%, 0.52%, 1.76% and 1.66% respectively. Market capitalization also gained 0.62% from the previous week to close at KES 1.46 trillion, recording a year-to-date increase of 1.52%. The performance was driven by gains recorded by large-cap stocks such as Equity, Standard Chartered and ABSA of 1.96%, 1.86% and 1.77%. This was however weighed down by losses recorded by other large-cap stocks such as EABL, Stanbic and KCB of 1.67%, 1.57% and 1.36% respectively.

The Banking sector had shares worth KES 251M transacted which accounted for 40.73% of the week’s traded value, Manufacturing and Allied sector had shares worth KES 40.3M transacted which represented 6.53% and Safaricom, with shares worth KES 297.3M transacted represented 48.19% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Sanlam | 26.67 | 26.67% |

| NBV | 4.88% | 19.44% |

| EA Cables | -2.04% | 9.09% |

| HF Group | 6.96% | 8.21% |

| Umeme | 1.93% | 7.82% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Transcentury | 13.46% | -11.76% |

| CIC | -7.42% | -6.19% |

| Sameer | -10.57% | -4.69% |

| Kenya-Re | 0.54% | -4.62% |

| Sasini | 5.00% | -4.55% |

Alternative Investments

| Losers | Week (previous) | Week (ending) | % Change |

|---|---|---|---|

| Derivatives Turnover (million) | 0.46 | 1.37 | 195.90% |

| Derivatives Contracts | 16.00 | 14.00 | -12.50% |

| I-REIT Turnover (million) | 0.20 | 0.02 | -90.28% |

| I-REIT deals | 27.00 | 9.00 | -66.67% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 2.04% | 1.17% |

| Dow Jones Industrial Average (DJI) | 0.39% | 0.72% |

| FTSE 100 (FTSE) | -3.36% | -2.14% |

| STOXX Europe 600 | -1.94% | -1.58% |

| Shanghai Composite (SSEC) | -4.39% | -1.72% |

| MSCI Emerging Markets Index | -5.25% | -2.55% |

| MSCI World Index | 0.19% | 0.22% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 4.33% | 3.16% |

| JSE All Share | -4.31% | -2.21% |

| NSE All Share (NGSE) | 24.41% | 13.84% |

| DSEI (Tanzania) | -1.20% | -0.82% |

| ALSIUG (Uganda) | -0.11% | -1.46% |

The US stock market closed the week in the green zone, boosted by optimism surrounding AI applications and a surge in chipmaker demand, with heavyweight technology stocks leading the charge.

The European stock closed the week on a downward trajectory, as investors grappled with concerns over central bank interest rate cuts, with the focus being on the upcoming European Central Bank’s policy meeting.

The Asian stock market closed the week in the red zone, weighed down by slowing Chinese economic growth and fading hopes for early U.S. rate cuts.

Week’s Highlights

Get future reports

Please provide your details below to get future reports:

[fluentform id=”3″]