Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,743 million (3.61 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar to exchange at KES 153.34, but appreciated against the Sterling Pound and the Euro to exchange at KES 192.76 and KES 165.28 respectively. The observed depreciation against the Dollar is attributed to a high demand from energy and commodity importers.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | 24.24% | 0.07% |

| Sterling Pound | 29.60% | -0.53% |

| Euro | 25.53% | -1.30% |

Liquidity

Liquidity in the money markets increased, with the average inter-bank rate decreasing from 10.57% to 10.40%, as government payments more than offset tax remittances. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 10.57% | 10.40% |

| Interbank volume (billion) | 9.67 | 10.23 |

| Commercial banks’ excess reserves (billion) | 23.10 | 25.00 |

Fixed Income

T-Bills

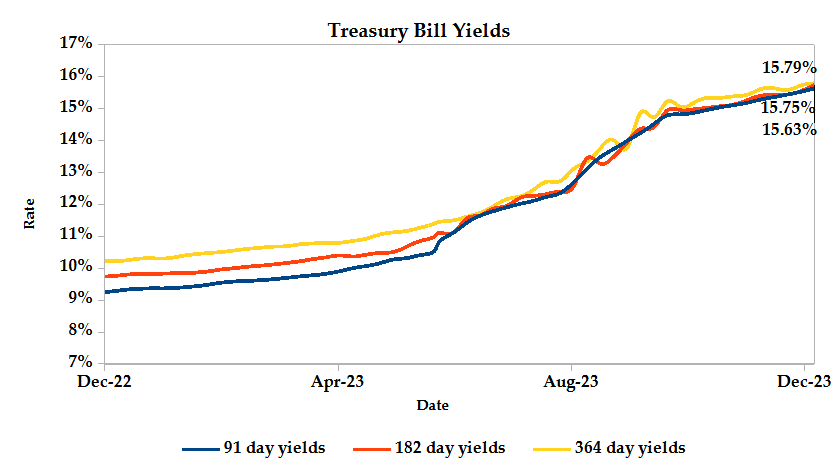

T-Bills remained over-subscribed during the week, with the overall subscription rate increasing to 156.90%, up from 100.26% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 786.08% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 54.12% and 8.00% respectively. The acceptance rate decreased by 0.65% to close the week at 94.27%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 28.24% from KES 10.10 billion in the previous week to KES 12.95 billion. Total bond deals increased by 1.36% from 588 in the previous week to 596.

In the primary bond market, CBK released auction results for the re-opened 6.5-year infrastructure bond IFB1/2023/6.5, which sought to raise KES 25 billion. The issue received bids worth KES 47.24 billion, representing a subscription rate of 188.96%.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average of 0.20% compared to the previous week, a 0.20% month-to-date loss and a 0.57% year-to-date gain. The yields on the 10-year Eurobonds for Angola and Zambia increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 1.46% | -0.02% | -0.02% |

| 2018 10-Year Issue | 0.51% | -0.32% | -0.32% |

| 2018 30-Year Issue | 0.15% | -0.17% | -0.17% |

| 2019 7-Year Issue | 0.59% | -0.30% | -0.30% |

| 2019 12-Year Issue | 0.22% | -0.19% | -0.19% |

| 2021 13-Year Issue | 0.51% | -0.22% | -0.22% |

Equities

NASI, NSE 20, NSE 25 and NSE 10 settled 1.81%, 1.25%, 1.06% and 0.57% higher compared to the previous week, bringing the year-to-date performance to -26.23%, -9.68%, -22.81% and -6.58% respectively. Market capitalization also gained 1.81% from the previous week to close at KES 1.47 trillion, recording a year-to-date decline of -26.03%. The performance was driven by gains recorded by large-cap stocks such as Stanbic, ABSA and Safaricom of 6.13%, 5.02% and 3.56%. These were however weighed down by losses recorded by large-cap stocks such as NCBA and Co-operative of 2.56% and 2.63% respectively.

The Banking sector had shares worth KES 183.9M transacted which accounted for 13.58% of the week’s traded value, Manufacturing and Allied sector had shares worth KES 41.2M transacted which represented 3.04% and Safaricom, with shares worth KES 73.8M transacted represented 79.64% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Bamburi | 31.48% | 17.97% |

| Eaagads | 32.86% | 9.84% |

| BK Group | 20.00% | 9.09% |

| FAHARI I-REIT | -6.49% | 8.56% |

| EA Cables | 12.94% | 6.67% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Eveready | 55.56% | -14.50% |

| Home Africa | -20.59% | -10.00% |

| Standard Group | -24.98% | -9.89% |

| Olympia | -5.41% | -9.68% |

| HF Group | 13.97% | -8.88% |

Alternative Investments

| Losers | Week (previous) | Week (ending) | % Change |

|---|---|---|---|

| Derivatives Turnover (million) | 0.33 | 0.83 | 156.50% |

| Derivatives Contracts | 10.00 | 10.00 | 0.00% |

| I-REIT Turnover (million) | 0.06 | 0.10 | 60.70% |

| I-REIT deals | 19.00 | 11.00 | -42.11% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 20.40% | 0.21% |

| Dow Jones Industrial Average (DJI) | 9.40% | 0.01% |

| FTSE 100 (FTSE) | 0.01% | 0.33% |

| STOXX Europe 600 | 8.77% | 1.30% |

| Shanghai Composite (SSEC) | -4.72% | -2.05% |

| MSCI Emerging Markets Index | 1.29% | -0.73% |

| MSCI World Index | 17.16% | 0.21% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 3.61% | 0.31% |

| JSE All Share | -1.01% | -3.06% |

| NSE All Share (NGSE) | 38.66% | 0.17% |

| DSEI (Tanzania) | -7.85% | 0.18% |

| ALSIUG (Uganda) | -26.68% | -0.64% |

The US stock market closed out the week in the green zone, fueled by a better-than-expected U.S. jobs report that showed low unemployment and strong job creation. This boosted investor confidence in achieving a soft economic landing.

The European stock market closed the week on an upward trajectory, fueled by investor bets on a potential pause in the European Central Bank’s (ECB) interest rate hikes and an encouraging U.S. jobs report that ignited risk appetite among investors.

Asian stock markets ended the week in the red, as investors grappled with both persistent concerns over a Chinese economic slowdown and the potential shift away from negative interest rates in Japan, as hinted by Bank of Japan Governor Kazuo Ueda.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 3.79% and 3.85% lower at $71.26 and $75.84 respectively. Gold futures prices settled 3.51% lower at $1,998.30.

Week’s Highlights

Get future reports

Please provide your details below to get future reports:

[fluentform id=”3″]