MONTH’S HIGHLIGHTS

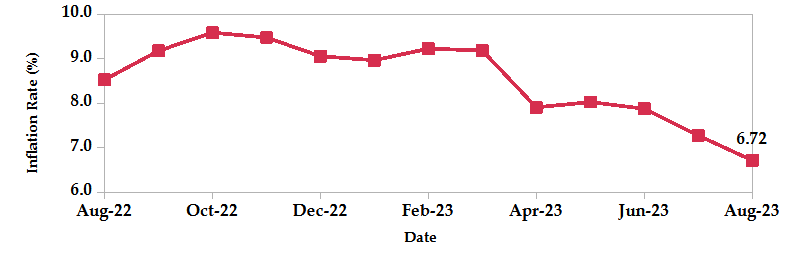

- Inflation declined for the third consecutive month to 6.72% in August from 7.28% in July, owing to easing food prices, as evidenced by a 0.5% drop in the food and non-alcoholic beverages inflation to 7.5%. The housing, water, electricity, gas and other fuels index remained relatively the same mainly due to the decrease in gas prices which offset the increase in electricity prices. Despite the steady petrol and diesel prices, the transport index rose 0.3% attributed to the rise in fare prices.

- The Monetary Policy Committee (MPC) of the Central Bank of Kenya met on 9th August 2023 and retained the lending rate at 10.50%, noting that the impact of the June 2023 tightening of monetary policy to anchor inflationary expectations was still working its way through the economy, as evidenced by the decline in overall inflation to within CBK’s target range of 2.5%-7.5% in July. The MPC expects a further decline in inflation as food prices continue to fall.

- Safaricom received approval from the Central Bank of Kenya to increase the M-PESA account limit to Kshs 500,000. The convenience this shift will bring to customers, particularly small businesses, is anticipated to increase as the volume of cashless transactions. In addition to the higher account limit, Safaricom also increased the daily transaction limit to Kshs 500,000. The current per-transaction limit of Kshs 150,000 will remain in place, but customers will be able to make as many transactions as they need to up to the daily limit of Kshs 500,000.

- The MPC approved key measures aimed at improving the monetary policy implementation framework and enhancing the transmission of monetary policy. These measures are in line with the reforms outlined in the White Paper on Modernisation of the Monetary Policy Framework and Operations. One of the key measures approved by the MPC is the introduction of an interbank interest rate corridor around the Central Bank Rate (CBR) set at CBR ± 2.5%. This framework allows CBK to conduct its open market operations on a flexible rate fixed quantity basis. The MPC also approved changes to the terms and conditions for the facility, including reducing the interest rate on the facility from 600 bps above the CBR to 400 bps above the CBR, and improving access to the CBK Discount (Overnight) Window facility.

- According to the minutes from the most recent European Central Bank (ECB) meeting, policymakers are contemplating a potential interest rate hike in September. However, the final decision hinges on forthcoming data and will be determined on a meeting-to-meeting basis. The ECB is striving to strike a balance between addressing inflationary concerns and effectively navigating the slowdown in economic growth.

- The Federal Reserve Chair highlighted the need for raising interest rates further to combat inflation and bring it back to the 2% target. The decision would be based on a careful evaluation of inflation indicators, economic performance and the labour market. However, the Fed could keep interest rates steady at its September meeting, pending a comprehensive review of incoming data and evolving market conditions.

- The Euro Area’s annual inflation rate held steady at 5.3% in August, surpassing the market’s anticipated 5.1%. While energy prices declined at a reduced rate, inflation decelerated for food, alcohol, tobacco, and non-energy industrial goods and services. On a monthly basis, consumer prices saw a 0.6% increase in August. Concurrently, the core inflation rate, which excludes volatile food and energy prices, followed the expected cooling trend, dropping from July’s 5.5% to 5.3%.

- China’s official NBS Manufacturing PMI in August exceeded expectations, rising to 49.7 from 49.3 in July. This marks the smallest decline in factory activity since March, attributed to Beijing’s stimulus efforts to boost the economy. Key highlights include increased output, the first growth in new orders in five months, improved buying activity, shortened delivery times and softer declines in export sales. However, employment continued to decline for the sixth consecutive month. Input costs rose for the second consecutive month, and output charges increased for the first time in six months. The business sentiment in general saw an improvement, reaching a six-month high.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves declined by 4.03% to settle at USD 7.08 billion (3.83 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

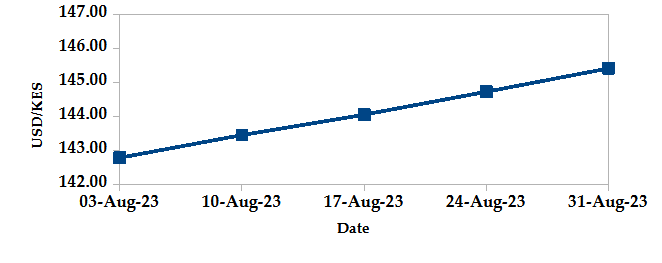

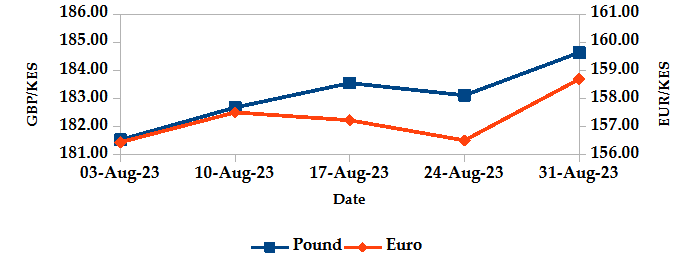

The Kenyan Shilling depreciated against the USD, the Sterling Pound and the Euro by 2.14%, 0.91% and 1.33%, exchanging at Kshs 145.41, Kshs 184.64 and Kshs 158.69 at the end of the month, up from Kshs 142.36, Kshs 182.97 and Kshs 156.61 in the previous month. The depreciation against the Dollar is a result of rising demand from importers and investors mitigating their risk by holding foreign currency deposits.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation declined to 6.72% in August from 7.28% in July. This is mainly attributed to lower food prices.

INFLATION EVOLUTION

Liquidity

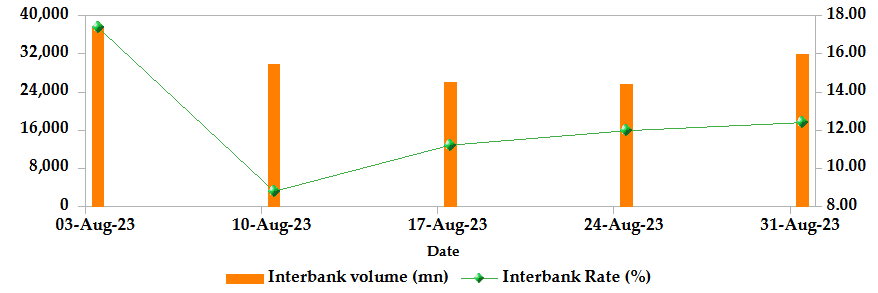

During the month, liquidity increased as a result of government payments which more than offset tax remittances. The interbank rate decreased from 16.55% to 12.40%. The volume of inter-bank transactions increased from Kshs 18.08 billion to Kshs 31.91 billion. Commercial banks excess reserves decreased from Kshs 18.10 billion to Kshs 14.90 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

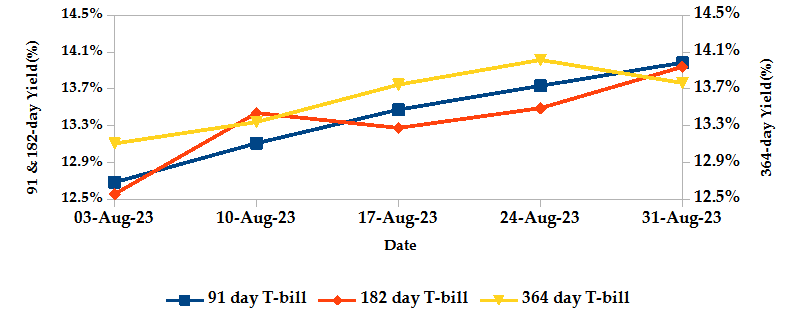

T-Bills

T-bills recorded an overall subscription rate of 125.07% during the month of August, compared to 119.98% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 632.59%, 33.99% and 13.13% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 13.22%, 12.48% and 8.15% to 13.99%, 13.94% and 13.77% respectively as investors aggressively bid to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

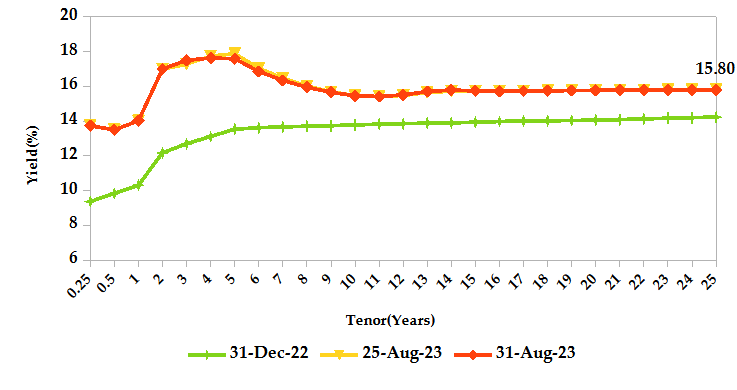

T-Bonds

During the month, T-Bonds registered a total turnover of Kshs 55.87 billion from 2,363 bond deals. This represents a monthly decrease of 4.35% and 6.08% respectively. The yields on government securities in the secondary market increased during the month of August.

In the primary market, CBK issued a new FXD1/2023/2 bond and reopened FXD1/2023/5 bond with an effective tenor of 4.9 years, seeking to raise Kshs 40.0 billion from the two papers. Additionally, the Central Bank reopened the same bonds through a tap sale seeking to raise Kshs 21.0 billion with coupon rates of 16.97% and 16.84% respectively.

In the international market, yields on Kenya’s Eurobonds increased by an average of 85 basis points.

YIELD CURVE

EQUITIES

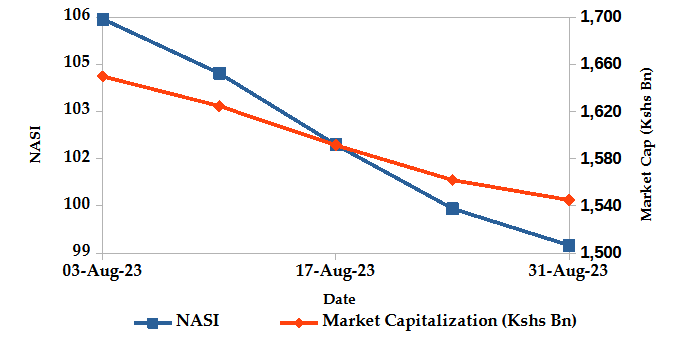

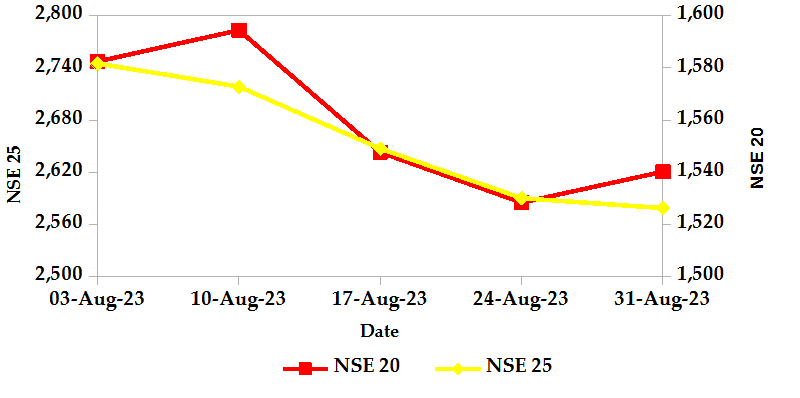

During the month, market capitalization lost 5.95% to settle at Kshs 1.54 trillion. Total shares traded decreased by 1.26% to 407.40 million shares and equity turnover dropped 18.26% to close at Kshs 5.36 billion. On a monthly basis, NASI, NSE 20 and NSE 25 settled 5.93%, 2.35% and 5.52% lower. The performance was a result of losses recorded by large-cap stocks such as KCB, Safaricom and ABSA of 17.19%, 8.88% and 5.26%.

NASI and Market Capitalization

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market, over the month, recorded 141 contracts with a turnover of Kshs 5.00 million which was an increase from 67 contracts with a turnover of Kshs 4.19 million recorded in the previous month.

- I-REIT market, over the month, recorded a turnover of Kshs 216.14 million with 680 deals which was an increase from Kshs 2.14 million with 198 deals recorded in the previous month.

- The ETF market, over the month, recorded a turnover of Kshs 3.54 million with 1 deal which was an increase from no activity recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -1.77% | 17.87% |

| STOXX Europe 600 | -2.79% | 5.53% |

| Shanghai Composite (SSEC) | -5.20% | 0.11% |

| MSCI Emerging Market Index | -6.36% | 1.85% |

| MSCI World | -2.55% | 14.81% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -0.53% | -3.71% |

| JSE All Share | -5.92% | 1.34% |

| NSE All Share (NGSE) | 3.44% | 28.98% |

| DSEI (Tanzania) | -0.39% | -6.03% |

| ALSIUG (Uganda) | -5.26% | -21.36% |

- Global markets registered losses during the month. In the US, the S&P 500 lost 1.77% and the Dow Jones index lost 2.36%. In Europe, both the STOXX Europe 600 and UK’s FTSE 100 indices edged 2.79% and 3.38% lower, respectively and in Asia Pacific, the Shanghai Composite (SSEC) index lost 5.20% The negative sentiment can be attributed to a number of factors, including growing concerns about an economic slowdown, as evidenced by the recent decline in manufacturing activity and slowdown in global trade; persistently elevated inflation levels, which has led to the rise in interest rates by central banks around the world in an effort to curb inflation.

- On a regional front, markets recorded mixed performance. The FTSE ASEA Pan African index, representing the overall African markets lost 0.53% from July. South Africa’s JSE All Share Index, Tanzania’s DSEI and Uganda’s All Share indices dropped by 5.92%, 0.39% and 5.26% respectively, while Nigeria’s All Share Index rose by 3.44%.

- On the global commodities markets, oil future indices edged higher, primarily driven by the anticipation of tighter supplies, resulting from deeper production cuts by Saudi and Russia, which largely offset outweighed concerns over slowing economic growth. Crude Oil WTI futures and ICE Brent Crude Oil settled 2.24% and 1.67% higher to close at $83.63 and $86.86 respectively.

Get future reports

Please provide your details below to get future reports: