MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) of the Central Bank met on 26th June 2023 and raised the lending rate from 9.50% to 10.50%, in response to the need for further tightening to anchor inflation expectations and the potential impact of elevated global risks on the domestic economy.

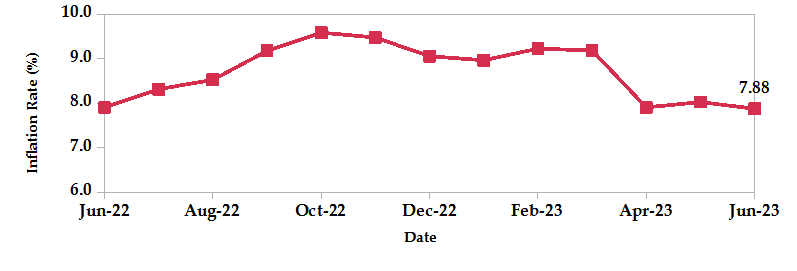

- Inflation slightly declined to 7.88% in June 2023 from 8.03% in May 2023, mainly driven by a 1.8% decrease in LPG prices. However, the overall sentiment was adversely affected by the surge in food and electricity prices. The food and non-alcoholic beverages index went up 1.3% reflecting higher sugar and vegetables prices. The housing, water, electricity, gas and other fuels index increased by 0.6%, attributed to a 4.2% rise in electricity prices. Additionally, the transport index saw a marginal uptick of 0.2% due to elevated fare prices.

- The Energy and Petroleum Regulatory Authority (EPRA) published an addendum to the monthly statement released on 14th June 2023 in response to the Finance Act 2023, implementation of the revised value-added tax (VAT) on petroleum products from 8% to 16% effective from 1st July 2023. As a result, the maximum pump prices of super petrol, diesel and kerosene increased by KES 13.49, KES 13.39 and KES 11.96 to KES 195.53, KES 179.67 and KES 173.44 per litre respectively effective from 1st July to 14th July 2023.

- The 2023/2024 approved Budget, effective from 1st July 2023, includes key tax policies to boost revenue generation. These include an increase in value-added tax (VAT) on petroleum products to 16% while exempting LPG products. New income tax rates of 32.5% for those with incomes between KES 500,000 and KES 800,000, and 35% for income exceeding KES 800,000. Mandatory contributions to the National Housing Development Fund for both employees and employers. Withholding tax applicability to digital content monetization and sales-related services. A rise in turnover tax rates, excluding businesses with income exceeding KES 25M per annum. Implementation of an electronic tax invoice management system (eTIMS) requirement for all businesses to ensure proper invoice generation. Other changes include adjustments to excise duty, remittance of withholding tax and withholding VAT, tax amnesty, VAT exemptions for exported services, reduced rental income tax rate, import declaration fees, railway development levy and the introduction of an export and investment promotion levy. Interest limitation rules will only be applicable to foreign loans.

- The government approved the conversion of the country’s debt ceiling from KES 10 trillion to a debt anchor based on a percentage of gross domestic product (GDP). With the support of the International Monetary Fund (IMF), this decision removed the final obstacle to Kenya’s alignment with global best practices. The Public Debt and Privatisation Committee authorized a debt anchor threshold of 55% of GDP in present value terms. Furthermore, the committee allowed a buffer of up to 5% to accommodate the existing debt threshold to GDP, which currently stands at 60%.

- The Caixin China General Manufacturing PMI declined to 50.5 in June 2023 from 50.9 in the previous month but exceeded market expectations. It marked the second consecutive month of growth, output expansion slowed compared to the previous month’s 11-month high. New orders increased at a slower pace, while employment continued its downward trend for the fourth consecutive month. Export sales remained steady, with a rise in buying activity. Input costs saw the most significant drop since January 2016, primarily due to lower raw material expenses. Selling prices declined as market competition intensified and efforts to stimulate sales were implemented. Overall, sentiment weakened to an 8-month low due to concerns regarding sluggish market conditions.

- The Bank of England surprised the market by raising its policy interest rate by 50 basis points to 5.0% in June, marking the thirteenth consecutive rate hike. This decision, aimed at combating persistent inflation, exceeded expectations of a smaller rate increase. Borrowing costs now stand at their highest level since the 2008 financial crisis. The Bank of England’s series of rate hikes, initiated over a year and a half ago, represents the fastest policy tightening in over three decades.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves increased by 15.39% to settle at USD 7.48 billion (4.12 months of import cover). This meets CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover. The increase was attributed to support from the World Bank loan facility, resolving the shortfall experienced since November 2022. However, it still falls short of the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

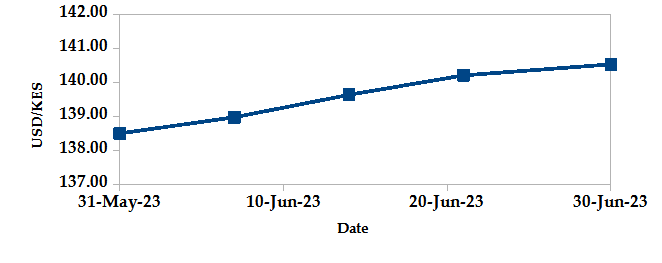

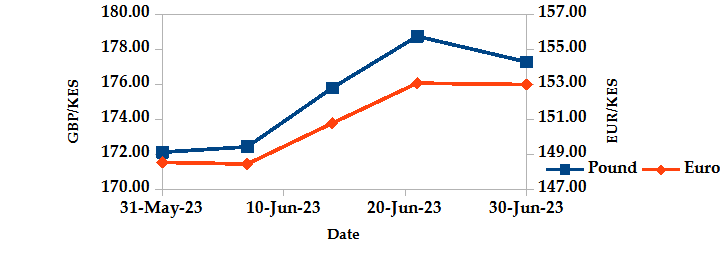

The Kenyan Shilling depreciated against the USD, the Sterling Pound and the Euro by 1.47%, 2.99% and 2.99%, exchanging at Kshs 140.52, Kshs 177.28 and 152.98 at the end of the month, up from Kshs 138.49, Kshs 172.12 and Kshs 148.54 in the previous month. The depreciation against the Dollar is a result of rising demand from importers and investors mitigating their risk by holding foreign currency deposits.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation slightly increased to 8.03% in May from 7.91% in April. This is mainly attributed to higher food and fuel prices.

INFLATION EVOLUTION

Liquidity

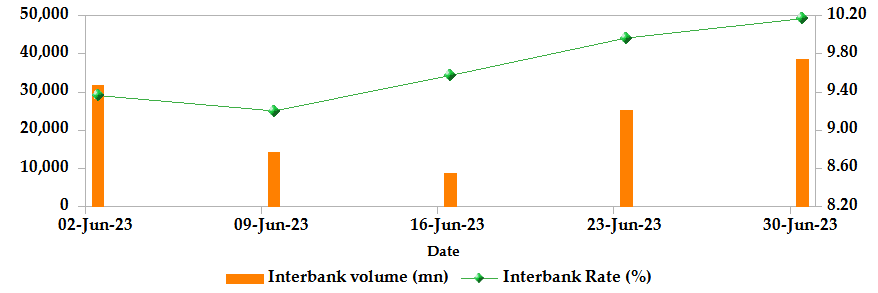

During the month, liquidity tightened as a result of tax remittances which more than offset government payments. The interbank rate increased to 10.17% from 9.35%. The volume of inter-bank transactions increased to Kshs 38.54 billion from Kshs 25.07 billion. Commercial banks’ excess reserves increased from Kshs 26.10 billion to Kshs 59.30 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

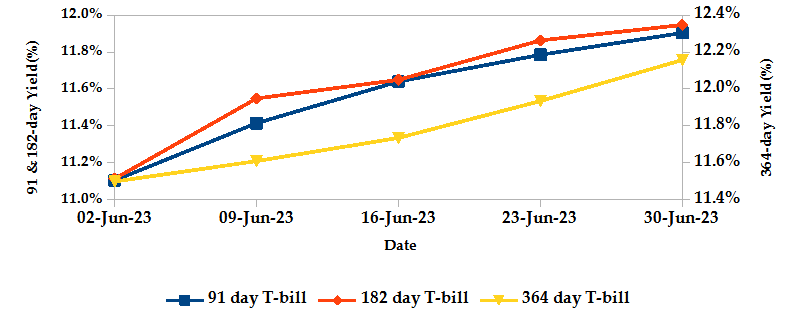

T-Bills

T-bills recorded an overall subscription rate of 86.76% during the month of June, compared to 135.40% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 422.30%, 18.59% and 20.71% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 9.90%, 7.50% and 6.11% to 11.90%, 11.95% and 12.16% respectively as investors aggressively bid to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

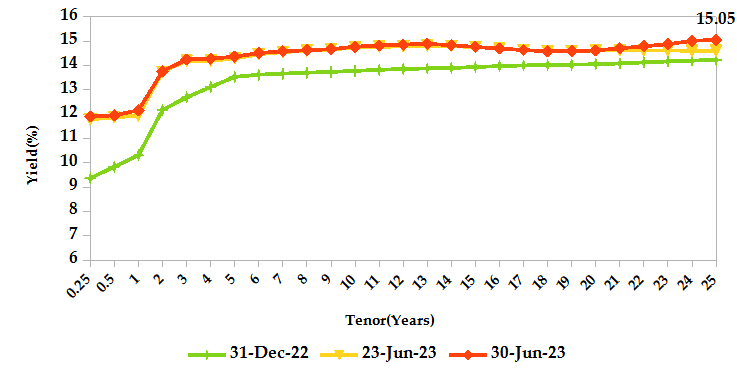

T-Bonds

During the month, T-Bonds registered a total turnover of Kshs 49.85 billion from 2,801 bond deals. This represents a monthly decrease of 22.11% and an increase of 64.19% respectively. The yields on government securities in the secondary market increased during the month of June.

In the primary market, CBK reopened the 3-year fixed coupon treasury bond; FXD1/2023/003, through a tap sale seeking to raise 15.0 billion at a 14.23% coupon rate.

In the international market, yields on Kenya’s Eurobonds decreased by an average of 122 basis points.

YIELD CURVE

EQUITIES

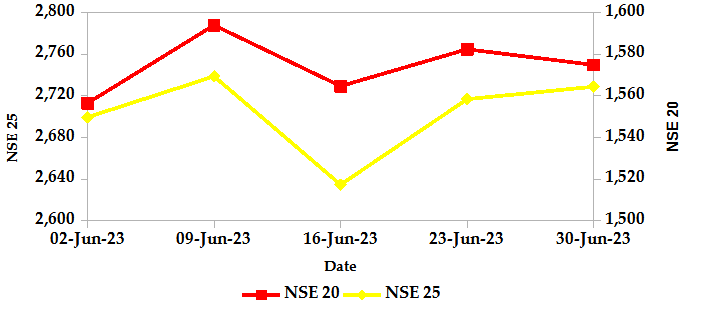

During the month, market capitalization gained 3.20% to settle at Kshs 1.67 trillion. Total shares traded decreased by 15.45% to 259.22 million shares while equity turnover dropped 9.98% to close at Kshs 4.82 billion. On a monthly basis, NASI, NSE 20 and NSE 25 settled 3.19%, 1.82% and 2.40% higher. The performance was a result of gains recorded by large-cap stocks such as Stanbic, Safaricom and ABSA of 8.01%, 5.42% and 3.96% respectively, which were weighed down by a loss posted by KCB of 7.86%.

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market, over the month, recorded 78 contracts with a turnover of Kshs 10.14 million which was an increase from 54 contracts with a turnover of Kshs 4.08 million recorded in the previous month.

- I-REIT market, over the month, recorded a turnover of Kshs 1.20 million with 227 deals which was an increase from Kshs 0.93 million with 139 deals recorded in the previous month.

- The ETF market, over the month, recorded no activity which was a decrease from Kshs 1.01 million with 1 deal recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 6.47% | 16.38% |

| STOXX Europe 600 | 2.25% | 6.39% |

| Shanghai Composite (SSEC) | -0.47% | 2.34% |

| MSCI Emerging Market Index | 3.23% | 2.80% |

| MSCI World | 5.93% | 14.06% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -7.45% | -4.87% |

| JSE All Share | 1.01% | 3.43% |

| NSE All Share (NGSE) | 9.32% | 18.17% |

| DSEI (Tanzania) | -1.20% | -4.73% |

| ALSIUG (Uganda) | -0.62% | -16.25% |

- Global markets remained volatile during the month. In the US, both the S&P 500 and the Dow Jones index edged 6.47% and 4.54% higher compared to the previous month, attributed to banks’ robust performance following a positive outcome in the Federal Reserve’s stress test, affirming their strength in navigating a severe recession scenario. In Europe, both the STOXX Europe 600 and the UK’s FTSE 100 indices went up by 2.25% and 1.15% following Swedish retailer H&M’s better-than-anticipated quarterly profit. In Asia Pacific, however, the Shanghai Composite (SSEC) index dropped by 0.47% as a result of weak Chinese economic data and growing concerns about further rate hikes in the U.S.

- On a regional front, markets posted mixed performance. The FTSE ASEA Pan African index, representing the overall African markets lost 7.45% from May. South Africa’s JSE All Share and Nigeria’s All Share index gained 1.01% and 9.32% while Tanzania’s DSEI and Uganda’s All Share index lost 1.20% and 0.62% respectively.

- On the global commodities markets, oil future indices edged higher despite concerns about further interest rate hikes by major central banks. This increase was primarily driven by a significant and unexpected decline in US crude inventories, indicating increased demand in the world’s largest consumer, especially during the travel-intensive summer season. Crude Oil WTI futures and ICE Brent Crude Oil settled 3.75% and 3.08% higher to close at $70.64 and $74.90 respectively.

Get future reports

Please provide your details below to get future reports: